Euro Ignores Hawkish ECB Comments, Markets Continue Consolidations – Action Forex

The forex markets are holding steady in a consolidative pattern today. Notably, Euro has remained largely unaffected by continued hawkish messages emanating from top ECB officials, who have merely echoed President Christine Lagarde’s suggestion that an interest rate hike is likely in July, while situation in September remains uncertain.

Euro is the third weakest in trading today so far, trailing behind Aussie and Kiwi. Both of these are consolidating alongside other risk markets. Sterling and Swiss Franc are showing mixed performance as markets await rate decisions from the BoE and SNB later in the week. Dollar and Yen, meanwhile, are demonstrating signs of a modest recovery, while Canadian Dollar edges slightly ahead.

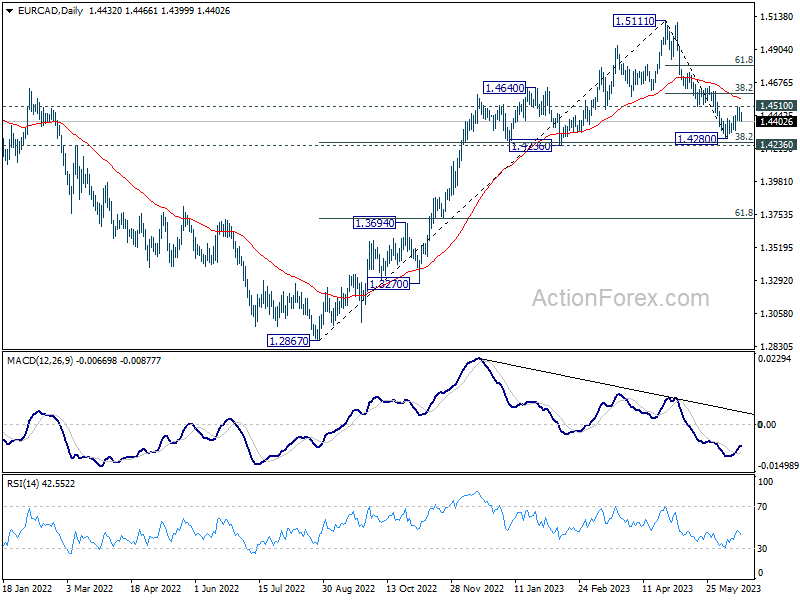

From a technical standpoint, the conditions appear ripe for a EUR/CAD rebound, with bullish convergence condition evident in 4H MACD. The 1.4280 mark is perilously close to 1.4236 cluster support (38.2% retracement of 1.2867 to 1.5111 at 1.4254). However, the current recovery momentum from 1.4280 is less than inspiring.

Should we witness a firm break above 1.4510 resistance, this would confirm short-term bottoming, leading to a stronger rise to 38.2% retracement of 1.5111 to 1.4280 at 1.4597 and above. Conversely, break below 1.4336 would suggest higher likelihood of an extended fall from 1.5111, pushing through 1.4236 cluster support.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.51%. DAX is down -0.77%. CAC is down -0.71%. Germany 10-year yield is up 0.0397 at 2.514. Earlier in Asia, Nikkei dropped -1.00%. Hong Kong HSI dropped -0.64%. China Shanghai SSE dropped -0.34%. Singapore Strait Times dropped -0.58%. Japan 10-year JGB yield fell -0.0090 to 0.395, below 0.4 handle.

ECB Lane: September is so far away, let’s see

ECB Chief Economist Philip Lane emphasized the central bank’s data-driven approach in managing inflation. Speaking today he suggested that another interest rate hike is likely in July, provided there are no significant changes in the economic outlook.

“At this point, we are surely data-driven,” Lane stated, reflecting ECB’s commitment to making policy decisions based on economic indicators and trends. “July is not so far away, we can say unless there’s a material change another hike (is likely).”

Regarding further in September, however, Lane was more reserved. “But to me, September is so far away; let’s see in September,” he added.

Despite rising inflation, Lane remains optimistic about the medium-term outlook. “Inflation will come down fairly quickly in the next couple of years to ECB’s 2% target,” he predicted.

ECB Schnabel: We need to err on the side of doing too much

ECB Executive Board member Isabel Schnabel stressed the necessity of maintaining a proactive approach to monetary policy amid persistent inflation risks. In a speech today, she noted that “risks to the inflation outlook are tilted to the upside, reflecting both supply- and demand-side factors.”

Referencing IMF’s recent guidance, Schnabel noted, “The IMF has recently issued a clear recommendation: if inflation persistence is uncertain, risk management considerations speak in favour of a tighter monetary policy stance.”

She further explained the rationale behind this approach. “First, the costs of protecting the economy from upside risks to inflation are comparatively small, as the policy rate can be brought back to neutral levels faster than if policymakers acted under the assumption of low inflation persistence,” Schnabel said.

The second reason revolves around the high costs of reactive policies. Schnabel pointed out, “it is very costly to react only after upside risks to inflation have materialized, as this could destabilise inflation expectations and thus require a sharper contraction in output to restore price stability.”

Overall, Schnabel emphasized the need for data-dependent decisions that lean towards more action rather than less. “We need to remain highly data-dependent and err on the side of doing too much rather than too little,” she asserted.

She insisted, “We thus need to keep raising interest rates until we see convincing evidence that developments in underlying inflation are consistent with a return of headline inflation to our 2% medium-term target in a sustained and timely manner.”

ECB Kazimir: We need to deliver another rate hike in July

ECB Governing Council member Peter Kazimir stressed today the necessity for continued monetary policy tightening to address prevailing inflationary pressures. he specifically highlighted the need for another rate hike in July to move further into a restrictive policy stance.

“We need to deliver another rate hike in July and move further into restrictive territory,” Kazimir stated. He underscored that a continuation of monetary policy tightening is “the only reasonable way ahead.”

Looking ahead to September, Kazimir cautioned that an updated analysis would be required to assess the impact of ECB’s rate hike cycle before proceeding with further tightening measures. However, he emphasized that halting rate hikes prematurely presents a “much more significant” risk than overtightening.

Kazimir drew attention to several factors contributing to inflation risks, asserting, “Upward inflation risks are still substantial, linked to the labour market situation, food prices and, last but not least, profit margins.”

NZ BNZ services jumped back to 53.3, economy still on a broader slowing trajectory

New Zealand’s BusinessNZ Performance of Services Index climbed from 50.1 in April to 53.3 in May, revealing a slight uptick in the services sector. However, it’s worth noting that this figure remains marginally under long-term average of 53.6. A closer look at the numbers shows activity/sales leaping from 45.4 to 52.0, employment increasing from 50.5 to 52.6, and new orders/business ascending from 50.1 to 55.4. Stocks inventories slightly declined from 57.1 to 56.8, while supplier deliveries edged up from 50.6 to 51.1.

BusinessNZ’s Chief Executive Kirk Hope shared his insights, stating, “The lift in expansion for May also saw a pickup in the proportion of positive comments, which rose from 39.8% in April to 50.6% for the current month.” He further added that while there weren’t any defining themes, the overall positive comments were “either industry-specific or very general around increased activity.”

Nonetheless, the economy appears to be on a deceleration trajectory, which, according to BNZ Senior Economist Craig Ebert, is necessary to deflate the inflationary pressures.

“The bounce back in the PSI in May arguably helped calm a lot of nerves – after it sagged to 50.1 in April, and after the services component of Q1 GDP declined 0.6%. Still, this doesn’t deny the economy is on a broadly slowing trajectory, which is what’s required to take the inflationary heat out of it,” Ebert explained.

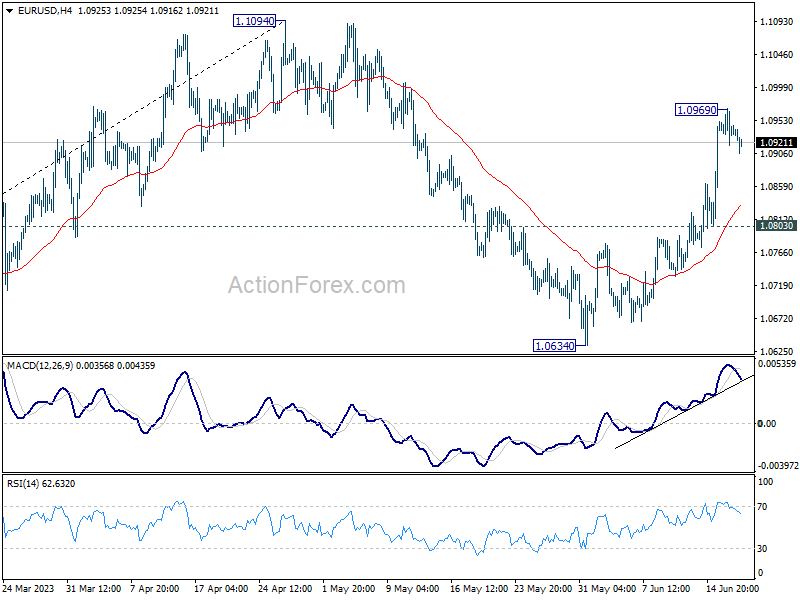

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0916; (P) 1.0944; (R1) 1.0969; More…

A temporary top is in place at 1.0969 with current retreat and intraday bias in EUR/USD is turned neutral first. Some consolidations could be seen. But further rally is expected as long as 1.0803 support holds. On the upside, above 1.0969 will resume the rise from 1.0634 to retest 1.1094 high. Decisive break there will confirm resumption of whole up trend from 0.9534. However, firm break of 1.0803 will extend the corrective pattern from 1.1094 with another falling leg, targeting 1.0634 and below.

{kind=link}

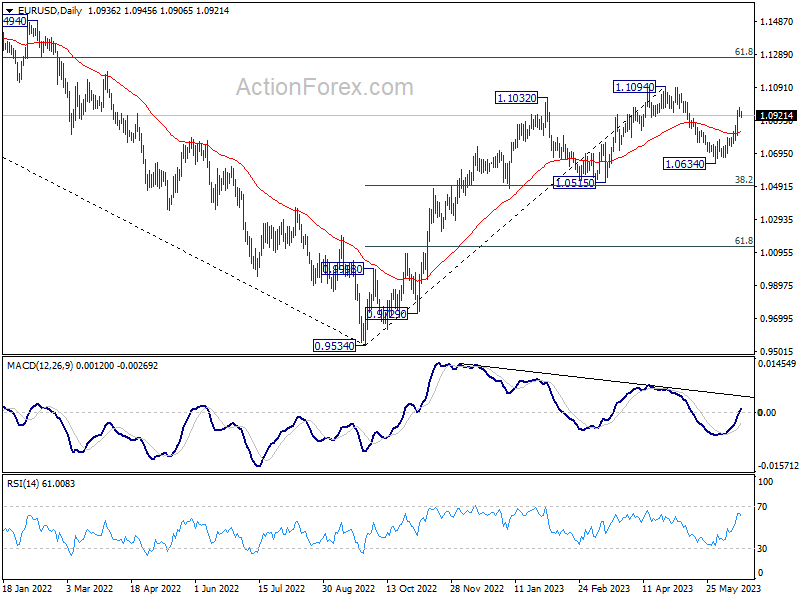

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI May | 53.3 | 49.8 | 50.1 | |

| 12:30 | CAD | Industrial Product Price M/M May | -1.00% | 0.20% | -0.20% | -0.60% |

| 12:30 | CAD | Raw Material Price Index M/M May | -4.90% | 2.40% | 2.90% | 1.80% |

| 14:00 | USD | NAHB Housing Market Index Jun | 50 | 50 |