A Stormy Week With Selloff in Bonds, Stocks, Bitcoin and China – Action Forex

Last week, the financial world navigated a storm of uncertainty and volatility. From skyrocketing treasury yields to the extended declines in equities, from the downward spiral of Chinese stock market to the tumultuous Yuan exchange rate, and not forgetting the unexpected nosedive in Bitcoin. At the same time the dynamics of these developments are closely intertwined.

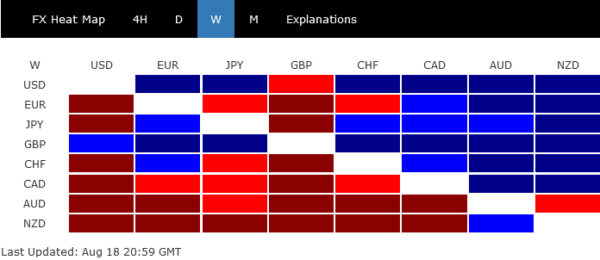

Dollar demonstrated its resilience, buoyed by the widespread risk-averse sentiment in the market. Yet, while it showcased strength, it was British Sterling that took the limelight, clinching the title as the week’s star performer. Meanwhile, Japanese Yen hinted at the dawn of a potential sustainable rebound, claiming the third spot on the podium.

However, not all currencies shared in the triumphs. Australian Dollar bore the brunt of the week’s tumult, finding itself at the mercy of subpar domestic data and external pressures from China’s own financial whirlwind. Trailing closely behind in this downtrend were New Zealand and Canadian Dollars, emblematic of the broader risk-averse climate. Amidst the currency chaos, both Euro and Swiss Franc seemed to tread water, their performances largely overshadowed by the formidable Pound.

Surging yields, falling stocks, and Dollar index

Last week, the financial markets witnessed significant shifts, with US treasury yields surging and stocks undergoing a sharp selloff. 30-year US Treasury bond yield rocketed to its loftiest since 2011, while 10-year yield was nudging levels at 2022 high, which was last observed in 2007.

Driving this dynamic was the mounting belief that interest rates in prominent economies are poised to remain elevated for a prolonged period. US macroeconomic indicators throughout the summer seemingly validate a resilient economy, with concerns about Fed’s unresolved battle against inflation. This perspective gained traction, especially after FOMC’s July meeting minutes revealed a majority of participants sensing pronounced “upside risks to inflation.”

10-year yield touched 4.328 before retracting a bit, concluding at 4.251. While short-term consolidations seem likely with TNX contesting 4.333 high, outlook will stay bullish, as long as 3.957 support remains intact. Decisive break of 4.333 would mark resumption of the long-term uptrend from 2020’s 0.398 low, with sights set on the 5% handle and above.

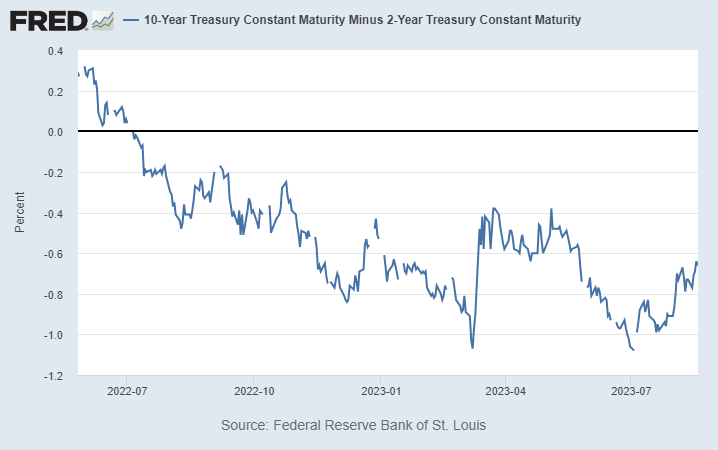

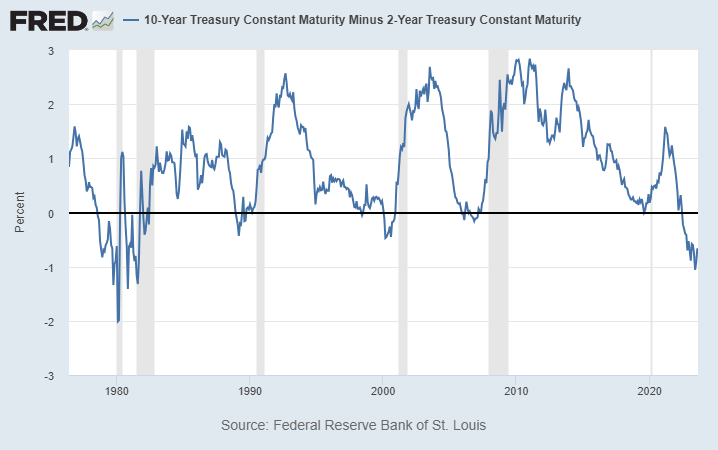

Another noteworthy development was the further normalization of the 2- to 10-year yield curve. Historically, US recessions have typically trailed a complete normalization by a few months. While not immediately alarming, if the yield difference between 2- and 10-year bonds shrinks beneath 0.4%, a crash in risk sentiment could be more imminent.

On the equities front, S&P 500’s marked break of 55 D EMA, (now at 4414.93), suggests it’s already correcting the whole up trend from 3491.58 (2022 low) at least. Further decline is now expected as long as 4443.98 support turned resistance holds, to 38.2% retracement of 3491.58 to 4607.07 at 4180.95.

It’s also possible that the fall from 4067.07 is indeed the third leg of the pattern from 4818.62 (2022 high). Sustained break of 55 W EMA (now at 4188.21, and close to above mentioned 4180.94 retracement level), will bolster this bearish case and confirm medium term reversal for 3491.58 support again .

Dollar index’s rebound from 99.57 continued last week. While the close above 55 W EMA was a positive, momentum remains unconvincing. This rebound is still viewed as a corrective move for now. Nonetheless, further rally is in favor as long as 101.78 support holds, towards 38.2% retracement of 114.77 to 99.57 at 105.37.

As for the rally to be reversing the down trend from 114.77, rather than correcting it, decisive break of 10-year yield above 4.333 high seems not enough. The strength in benchmark yields in UK and Germany indicated that it’s a common development in major economies. Substantial risk aversion would need to be the trigger, like S&P 500 breaking through above mentioned 4180.95 decisively.

China’s Economic Concerns Deepen: Echoes Felt in Global Equity Markets

Investor confidence in China’s economic trajectory has taken a significant hit in the past few weeks. An onslaught of unfavorable news, encompassing bleak economic figures and corporate financial strains, is eroding assurance among stakeholders. Notably, the shadow banking behemoth Zhongzhi halted payments to a vast number of its customers. Country Garden , a prominent property firm, is teetering on the brink of a public bond default. Adding to the list, the troubled property conglomerate Evergrande has opted for bankruptcy protection.

The reverberations of these setbacks are evident on the trading floors, with equity benchmarks in both Hong Kong and mainland China plunging to their lowest since last November. This downturn in sentiment is expected to ripple through global markets due to China’s extensive economic entanglements worldwide, at least until measures to “de-risk” by other countries and regions are wholly actualized.

Hong Kong HSI tumbled through 18044.85 support last week to resume the whole decline from 22700.85. Deeper fall is now expected to 61.8% projection of 22700.85 to 18044.85 from 20361.02 at 17483.61 next. Strong rebound from there would keep the fall from 22700.85 as a corrective move.

However, decisive break there of 17483.61 could prompt downside acceleration to 100% projection at 15705.02. More importantly, give prior rejection by 55 W EMA (now at 19924.97), this development will raise the chance that HSI is trying to resume the whole down trend from 33484.07 (2018 high), and risk deeper fall through 14597.31 low. Should this grim scenario materialize, it would be a glaring red flag for China’s economic landscape, and the repercussions could be felt far beyond its borders.

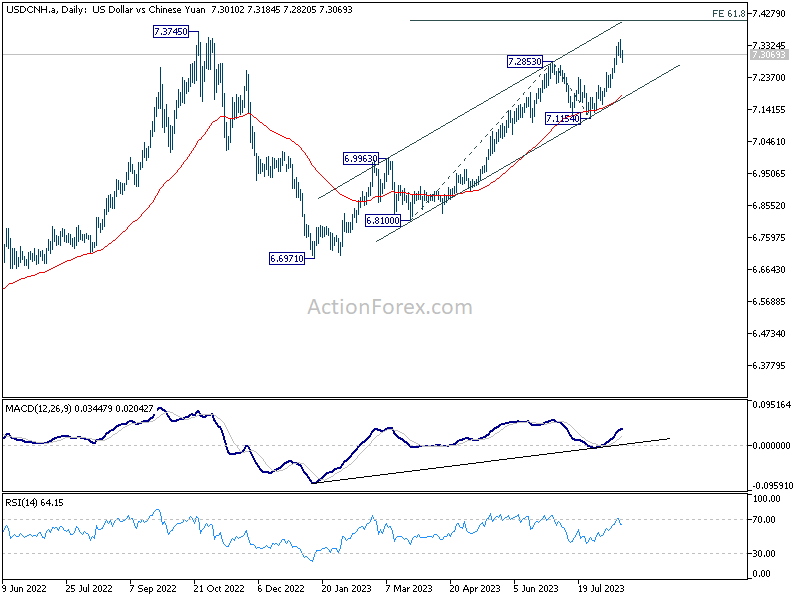

Offshore Yuan plunges amid Dollar strength: What’s next?

Amid the turmoil in China and PBoC’s rate cut, offshore Chinese Yuan has plummeted to its lowest in nine months. Signs of stabilization emerged only after China’s proactive interventions, aimed at stemming further decline, as the currency neared its 2022 low. Yet, market watchers are grappling with two crucial uncertainties.

First, there remains ambiguity around China’s strategic intent — whether Beijing is taking steps to establish a “floor” for Yuan at this juncture or merely attempting to decelerate its descent. The second, and perhaps more pressing, dilemma revolves around the interplay between currencies. While China’s ability to curtail Yuan’s weakness remains a topic of debate, its capacity to restrain a surging Dollar is undeniably limited. Heightened risk aversion in the US could push Dollar further up, exerting additional pressure on Yuan. This, in turn, might amplify disruptions in China’s financial landscape, then spill over across global markets.

In the immediate term, further rise is still in favor in USD/CNH as long as 55 4H EMA (now at 7.2766) holds. Next target is 61.8% projection of 6.8100 to 7.2853 from 7.1154 at 7.401. Firm break of 55 4H EMA will bring deeper pull back first before setting out the next move.

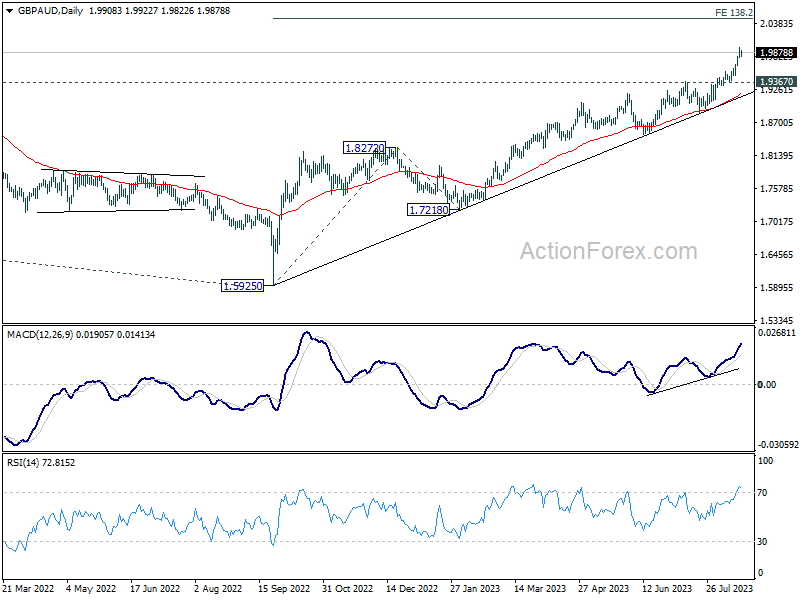

GBP/AUD broke long term trend line as rally accelerates

GBP/AUD emerged as the top performer last week, registering 1.72% gain. This momentum is attributed to a combination of factors. In the UK, unprecedented wage growth points towards persistent inflationary pressures. With this backdrop, BoE would need to continuing rat hikes, by 25 bps in September and possibly once more in November, culminating their current tightening cycle. Conversely, Australia’s disappointing employment figures have cemented RBA stance to maintain rates at 4.10%. The situation is further exacerbated for Aussie due to uncertainties in the Chinese economy.

From a near term point of view, GBP/AUD’s outlook will stay bullish as long as 1.9367 support holds, next target is 138.2% projection of 1.5925 to 1.8272 from 1.7218 at 2.0406.

But more important, last week’s break of the long term trend line as seen in the monthly chart carries some significance. The consolidation pattern from 2.2382 (2015 high) could have completed with three waves to 1.5925 (2022 low). Decisive break of 2.0840 would affirm this case and set the stage for further rise through 2.2382. If that’s true, we’d be looking at 100% projection of 1.4378 to 2.2382 from 1.5925 at 2.3929 as the target. In other words, GBP/AUD is less than half way through the trend at current rate, and the rally may still have considerable ground to cover.

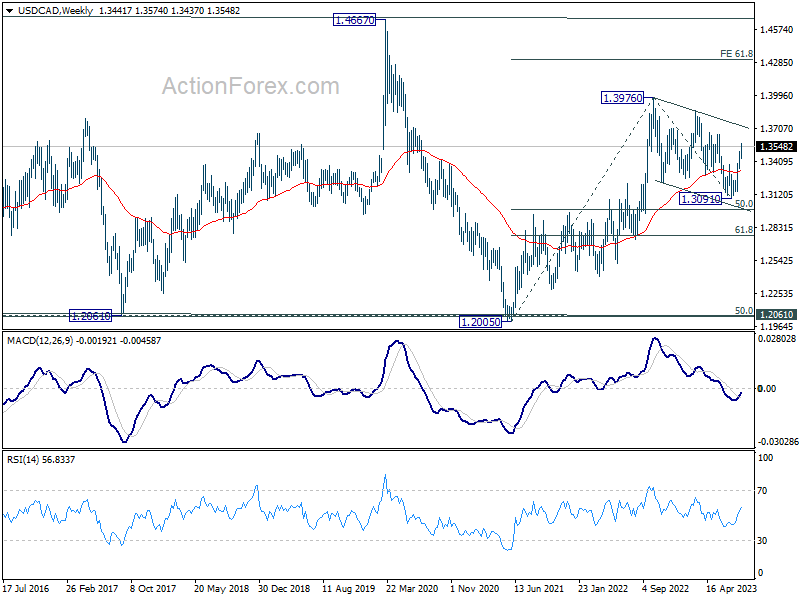

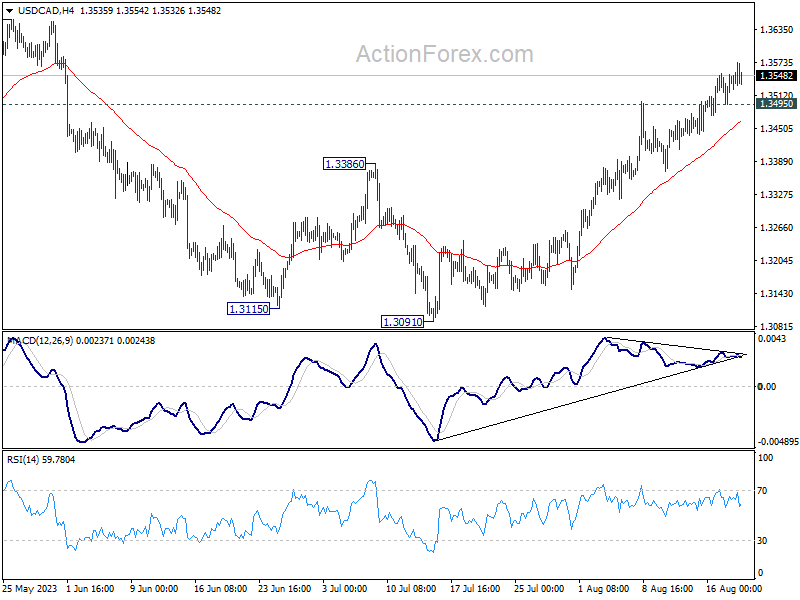

USD/CAD Weekly Outlook

USD/CAD’s rally from 1.3091 continued last week and hit as high as 1.3574. Initial bias stays on the upside this week for retesting 1.3653 resistance. Decisive break there will confirm that correction from 1.3976 has completed, a target a test on this high. On the downside, below 1.3495 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, price actions from 1.3976 are viewed as a corrective fall only. Upon completion, rise from 1.2005 (2021 low) would resume through 1.3976. Next target is 61.8% projection of 1.2005 to 1.3976 from 1.3091 at 1.4309. In case of another fall, downside should be contained by 61.8% retracement of 1.2005 to 1.3976 at 1.2758.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern only, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as 55 M EMA (now at 1.3044) holds.