US CPI to Dictate Dollar’s Path, GBP/JPY Poised Ahead of UK Employment Figure – Action Forex

The financial markets are intently focused on the upcoming US CPI report, a key indicator that could influence Fed’s next steps. Expectations are leaning towards further slowdown in headline inflation to 3.3%, while core inflation rate is projected to remain steady at 4.1%. However, there’s a growing consensus among economists about the potential for upside risks in this data release, especially concerning slower goods disinflation and stubborn shelter inflation.

Given Fed Chair Jerome Powell’s recent admission of lacking confidence in the effectiveness of the current monetary policy to bring inflation back to target, any deviation above the forecast in today’s CPI data could solidify the rationale for additional rate hikes. Presently, the likelihood of a rate increase in December is pegged at 14.3%, with January’s odds slightly higher at 26.7%, according to fed funds futures.

A stronger-than-anticipated inflation report could trigger a surge in Dollar, not only by raising the probability of a Fed hike but also through inducing a wave of risk aversion in the markets.

As for currency performance this week so far, New Zealand Dollar emerges as the weakest for now, closely followed by the Canadian Dollar and Yen. Sterling stands out as the strongest, but upcoming UK job data and CPI figures will be crucial tests. Australian Dollar and Euro are showing strength too, yet they appear increasingly vulnerable. Dollar, in the meantime, remains in a state of flux, awaiting decisive cues from CPI data.

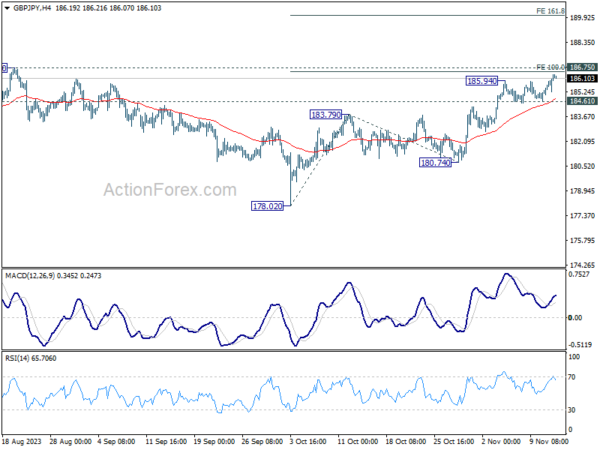

Technically, GBP/JPY’s rally from 178.02 resumed by breaking through 185.94 resistance yesterday. Further rise is now expected as long as 184.61 support holds. Immediate focus is now on 186.75 resistance. Decisive break there will confirm larger up trend resumption. Next near term target will be 161.8% projection of 178.02 to 183.79 from 180.74 at 190.07.

In Asia, at the time of writing, Nikkei is up 0.45%. Hong Kong HSI is down -0.12%. China Shanghai SSE is up 0.07%. Singapore Strait Times is down -0.40%. Japan 10-year JGB yield is down -0.0172 at 0.859. Overnight, DOW rose 0.16%. S&P 500 dropped -0.08%. NASDAQ dropped -0.22%. 10-year yield rose 0.004 to 4.632.

Japan’s Suzuki emphasizes balancing positives and negatives of weak Yen

As Japanese Yen continues to hover near multi-decade lows against Dollar after yesterday’s selloff, Japan’s Finance Minister Shunichi Suzuki reiterated the government’s commitment to addressing the currency’s movements. In his latest remarks, Suzuki avoided any direct mention of intervening in the currency markets, focusing instead on a strategy to balance the impact of the Yen’s weakness.

Suzuki stated, “What’s important is to maximize positive effects from the weak yen while mitigating negatives.” His comments come as the Japanese government faces the challenges of managing economic implications of Yen’s prolonged decline. While a weaker Yen can benefit Japan’s export-driven economy, it also raises concerns about increased import costs, especially in the context of global inflationary pressures.

Suzuki’s emphasis on maximizing the benefits and reducing the drawbacks of the weak Yen highlights the delicate balancing act the Japanese authorities must perform in the current economic environment. His statement suggests a cautious approach from the government, possibly hinting at measured responses rather than abrupt market interventions.

Australia’s consumer sentiment plummets post RBA rate hike

Australia’s Westpac Consumer Sentiment Index saw a significant decline in November, dropping by -2.6% mom to 79.9, reflecting a deepening pessimism among consumers.

Westpac attributed this drop to the recent RBA rate hike, noting a -6% decrease in confidence during the survey period. Despite the overarching pessimism, labor market confidence and housing-related sentiment remained relatively stable.

Westpac further commented, “The Reserve Bank Board next meets on December 5. The November Consumer Sentiment survey highlights the weak and uneven conditions across Australia’s consumer sector. How this plays out for wider domestic demand in the context of strong population growth is something the Board will need to consider as it acts to ensure inflation returns to target.”

Australia NAB business confidence dips to -2, conditions resilient

In Australia, NAB reported a dip in Business Confidence for October, falling from 0 to -2. However, Business Conditions saw a slight improvement, rising from 12 to 13. Notably, trading conditions increased from 18 to 20, and profitability conditions improved from 9 to 12, while employment conditions slightly decreased from 9 to 8.

NAB Chief Economist Alan Oster commented, “Business conditions remain healthy, picking up in October and still well above average. Still, business confidence remained soft in the month, still well below average at -2 index points.” He highlighted the persistent gap of 10-15 index points between current conditions and the more forward-looking confidence indicator, emphasizing that “Businesses clearly remain cautious about the outlook for the economy despite the resilience we are seeing.”

The report also noted a slowdown in price and cost growth. Labour cost growth eased to 1.8% in quarterly equivalent terms, and purchase cost growth declined to 1.8%. Retail price growth remained stable at 1.9%, while overall price growth eased to 1.0%, marking the slowest rate since July 2020.

Oster added, “The Q3 CPI showed inflation had been persistent through the middle of the year and the survey suggests this remained the case heading into Q4. We still expect to see gradual moderation over time but it will be a protracted process, especially given the resilience of domestic demand thus far.”

Looking ahead

UK employment, Swiss PPI, Eurozone GDP revision and German ZEW economic sentiment are the main focuses in European session. Later in the day, US CPI is the highlight.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6355; (P) 0.6374; (R1) 0.6395; More…

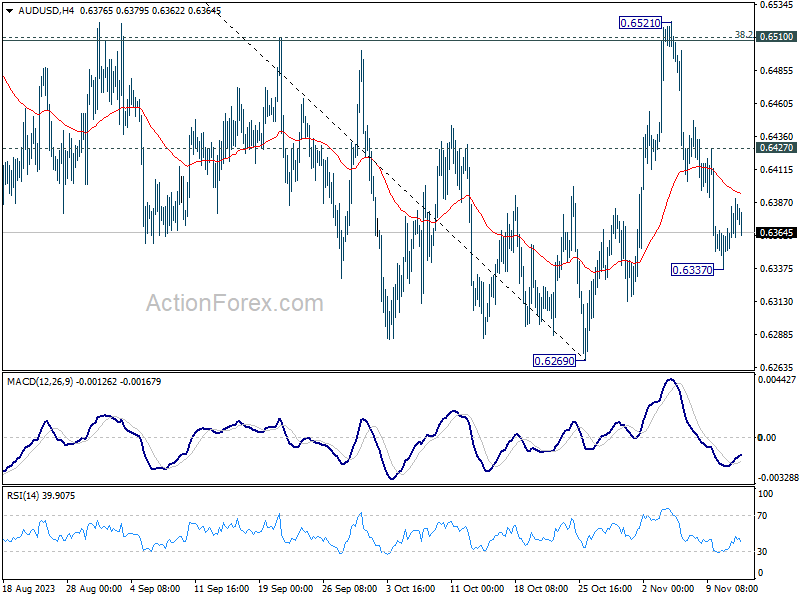

Intraday bias in AUD/USD is turned neutral first with current recovery. Some consolidations could be seen above 0.6337 temporary low. But deeper decline is expected as long as 0.6427 resistance holds. Below 0.6337 will resume the fall from 0.6521 and target 0.6269 support next. Firm break there will resume larger fall from 0.7156, to retest 0.6169 low. Nevertheless, above 0.6427 will bring stronger rebound back to 0.6510 cluster resistance (38.2% retracement of 0.6894 to 0.6269 at 0.6508).

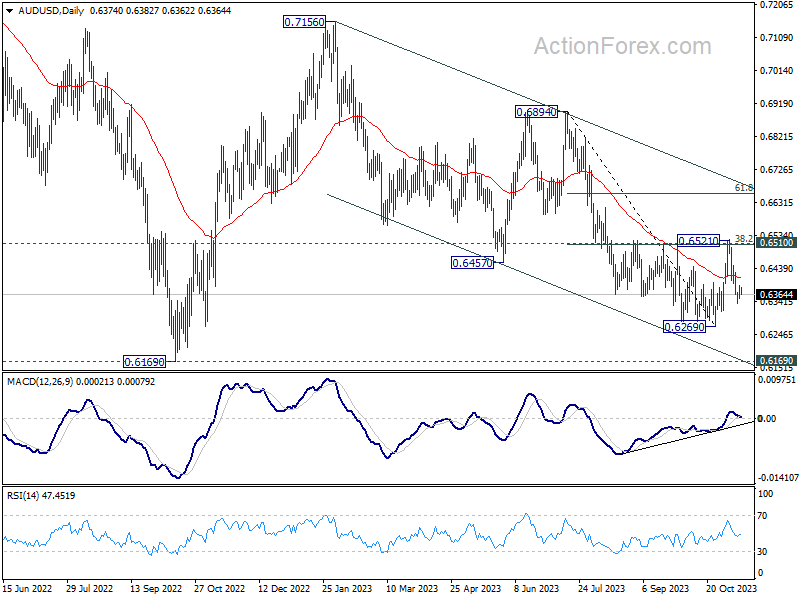

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of a corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Nov | -2.60% | 2.90% | ||

| 00:30 | AUD | NAB Business Conditions Oct | 13 | 11 | 12 | |

| 00:30 | AUD | NAB Business Confidence Oct | -2 | 1 | 0 | |

| 07:00 | GBP | Claimant Count Change Oct | 15.0K | 20.4K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Sep | 4.20% | 4.20% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Sep | 7.40% | 8.10% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Sep | 7.70% | 7.80% | ||

| 07:30 | CHF | Producer and Import Prices M/M Oct | 0.10% | -0.10% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Oct | -1.00% | |||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | -0.10% | -0.10% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 P | 0.20% | 0.20% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Nov | 4.9 | -1.1 | ||

| 10:00 | EUR | Germany ZEW Current Situation Nov | -75.5 | -79.9 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | 6.1 | 2.3 | ||

| 13:30 | USD | CPI M/M Oct | 0.10% | 0.40% | ||

| 13:30 | USD | CPI Y/Y Oct | 3.30% | 3.70% | ||

| 13:30 | USD | CPI Core M/M Oct | 0.30% | 0.30% | ||

| 13:30 | USD | CPI Core Y/Y Oct | 4.10% | 4.10% |