Canadian Dollar Remains Weak Post-CPI, as Gold Breaches 2000 Barrier – Action Forex

Canadian Dollar exhibited softness in early US session, a reaction to lower-than-expected consumer inflation readings. This development, indicative of ongoing disinflation, could bolster BoC’s confidence to maintain its current policy stance in the upcoming December meeting. Notably, Canadian Dollar has been unique among major currencies in its inability to break above prior week’s high against Dollar. This performance is also influenced by recent weaknesses in oil prices, as WTI crude remains capped well below 80 mark despite some recovery this week.

Elsewhere in the currency markets, Dollar is trailing as the weakest performer. The upcoming FOMC minutes are not expected to provide substantial support to the greenback redirecting focus to developments in risk markets. Euro, meanwhile, is showing signs of struggle, especially evident in EUR/USD, which is losing upside momentum after encountering resistance at 1.0958 Fibonacci level. In contrast, Sterling is benefiting from hawkish comments by BoE Governor, making it a stronger European major currency.

New Zealand Dollar has emerged as today’s strongest performer, narrowly outpacing the Japanese Yen. However, Yen still holds potential for further strengthening, particularly against Dollar. Australian Dollar, on the other hand, appears to be losing momentum.

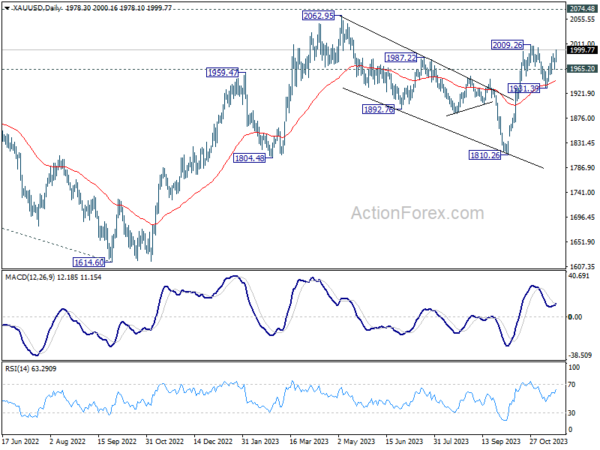

On the technical front, Gold’s rise from 1931.39 resumed today and breached 2000 briefly. Further rally is expected as long as 1965.20 support holds. Retest of 2009.26 should seen next. Firm break there will resume whole rise from 1810.26 for key long term resistance zone at 2062.95/2074.48.

In Europe, at the time of writing, FTSE is down -0.55%. DAX is up 0.07%. CAC is down -0.35%. Germany 10-year yield is down -0.030 at 3.585. Earlier in Asia, Nikkei dropped -0.10%. Hong Kong HSI dropped -0.25%. China Shanghai SSE dropped -0.01%. Singapore Strait Times dropped -0.49%. Japan 10-year JGB yield dropped -0.0445 to 0.699.

Canada CPI eased to 3.1% yoy in Oct, driven mainly by gasoline prices

Canada’s CPI in October showcased a slowdown, dropping from 3.8% yoy to 3.1% yoy, falling slightly below market expectation of 3.2% yoy. This deceleration in inflation is primarily attributed to a significant reduction in gasoline prices, which decreased by -7.8% yoy. When gasoline is excluded from the equation, the CPI exhibited only a marginal decline, easing from 3.7% yoy to 3.6% yoy.

The breakdown of CPI data reveals contrasting trends between goods and services. Prices for goods saw notable deceleration, moving from 3.6% yoy to 1.6% yoy, with lower gasoline prices playing a major role in this decrease. Conversely, prices for services experienced acceleration, rising from 3.9% yoy to 4.6% yoy. This increase in service prices was driven largely by costlier travel tours, rent, property taxes, and other special charges.

In terms of the core inflation measures, CPI median aligned with expectations, slowing from 3.9% yoy to 3.6% yoy. CPI trimmed, which eliminates the most extreme price movements, showed a reduction from 3.7% yoy to 3.5% yoy, coming in slightly below anticipated 3.6% yoy. Meanwhile, CPI common, which tracks common price changes across categories, also slowed down from 4.4% yoy to 4.2% yoy, falling below expected 4.3% yoy.

BoE’s Bailey highlights market misjudgment on inflation persistence

During today’s Treasury Committee hearing, BoE Governor Andrew Bailey expressed concern that the markets might be overly focused on recent data releases, including the recent decrease in inflation for October. He highlighted that the market is perhaps “putting too much weight” on these short-term data points, potentially overlooking the broader challenge of persistent inflation.

BoE Governor stressed the significance of not becoming complacent with current data trends, emphasizing the potential “persistence” of inflation. “I think the market is underestimating that,” he said, pointing towards the complexity of the inflationary environment.

Addressing the debate around inflation targets, Bailey firmly rejected the notion that the target should be adjusted to 3%. He said that it’s a “very bad argument,” underscoring the difficulties in bringing inflation down from 3% to 2%.

Regarding the 2% target, Bailey explained that while there isn’t an “objective magic” to this figure, it is widely recognized as the operational definition of price stability.

RBA’s Bullock: Australian economy faces prolonged inflation challenge

RBA Governor Michele Bullock, speaking at the Australian Securities and Investments Commission Annual Forum, emphasized the persistent challenge of inflation for the Australian economy. Bullock forecasted that inflation would remain a “crucial challenge” for the next “one or two years,” highlighting the complexity and longevity of the problem.

Bullock addressed a common misconception about the current inflationary environment, stating, “There is a bit of a perception around that the inflation at the moment really is all a supply driven thing – petrol prices, rents, these sorts of things, energy.” However, she clarified that there is also a significant “demand component” contributing to inflation, which central banks globally are striving to manage.

Governor Bullock also touched upon global issues, noting, “In a world of fragmentation and conflicts … We’re going to see more potential for supply shocks.” She explained the dilemma central banks face regarding such shocks: while the typical approach is to look through temporary supply shocks, a continuous stream of them can lead to entrenched inflation expectations. Bullock warned, “If inflation expectations adjust, then that’s a problem.”

RBA minutes indicate inflation control at forefront

RBA meeting minutes from November 7 reveal a decisive step in monetary policy adjustment, with a 25bps increase in cash rate to 4.35%. This move reflects the RBA’s heightened focus on managing inflationary pressures and aligning with its long-term targets.

The members’ discussion was centered around two options: raising the cash rate or maintaining it at its current level. The decision to increase the rate was influenced by the consensus that this was the “stronger” course of action.

Achieving inflation targets by the end of 2025 played a significant role in the decision-making process. RBA members acknowledged an increased risk of not meeting these targets, suggesting the necessity of a prompt policy response.

The minutes also reveal a strategic consideration of future scenarios. Delaying the rate adjustment was seen as potentially necessitating a “larger” policy response in the future, especially if inflation pressures intensify.

Preventing a significant rise in inflation expectations was another critical concern. The RBA aimed to avoid any shift in market sentiment that could destabilize inflationary trends. This is particularly relevant given the Board’s emphasis on “low tolerance” for delayed inflation target achievement.

Also, staff’s inflation forecasts, which anticipated one or two rate rises, further underscored the necessity of the rate hike.

New Zealand’s trade deficit narrows, led by reduced exports and imports to China

New Zealand’s trade figures for October have shown significant decrease in both goods exports and imports, leading to a narrowed monthly trade deficit. Exports fell by NZD -552m, or 9.3% yoy decline, totaling NZD 5.4B. Imports also saw a substantial drop of NZD -1.2B, or -14% yoy, to NZD 7.1B. Trade deficit consequently narrowed from NZD -2425m to NZD -1709m, which is larger than expected deficit of NZD -1150m.

A significant aspect of these shifts was the marked decrease in both exports and imports to and from China. China, being New Zealand’s top trading partner, saw the highest monthly fall in exports with a decrease of NZD -308m, amounting to – 19% reduction. This decline was echoed in imports from China, which fell by NZD -353m, a decrease of -18%.

Other key trading partners also showed varied trends. Exports to Australia decreased by NZD -128m (-15%), and to EU by NZD -84m (-24%). In contrast, exports to US slightly increased by NZD 2.9m (0.5%), and to Japan by NZD 25m (9.3%).

In terms of imports, apart from China, EU and US also registered significant drops, with decreases of NZD -138m (-11%) and NZD -146m (-20%), respectively. Imports from Australia and South Korea saw reductions of NZD -35m (-4.4%) and NZD -133m (-23%), respectively.

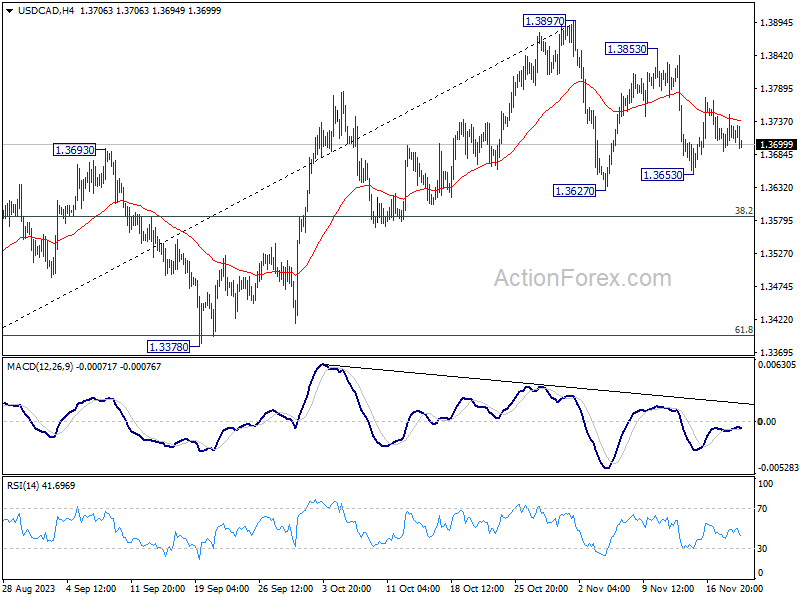

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3694; (P) 1.3722; (R1) 1.3754; More…

Intraday bias in USD/CAD remains neutral at this point as sideway trading continues. While another fall cannot be ruled out, downside should be contained by 38.2% retracement of 1.3091 to 1.3897 at 1.3589 to bring rebound. Break of 1.3897 is expected at a later stage to resume larger rally.

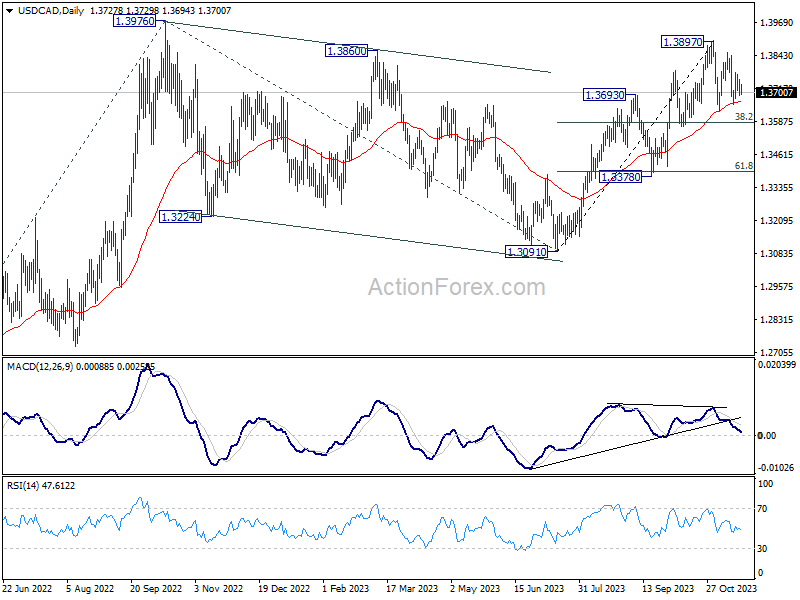

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will remain the favored case as long as 1.3378 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Oct | -1709M | -1150M | -2329M | -2425M |

| 00:30 | AUD | RBA Meeting Minutes | ||||

| 07:00 | CHF | Trade Balance (CHF) Oct | 4.60B | 5.87B | 6.32B | 6.28B |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Oct | 14.0B | 21.0B | 13.5B | |

| 13:30 | CAD | New Housing Price Index M/M Oct | 0.00% | 0.00% | -0.20% | |

| 13:30 | CAD | CPI M/M Oct | 0.10% | 0.20% | -0.10% | |

| 13:30 | CAD | CPI Y/Y Oct | 3.10% | 3.20% | 3.80% | 3.90% |

| 13:30 | CAD | CPI Median Y/Y Oct | 3.60% | 3.60% | 3.80% | |

| 13:30 | CAD | CPI Trimmed Y/Y Oct | 3.50% | 3.60% | 3.70% | |

| 13:30 | CAD | CPI Common Y/Y Oct | 4.20% | 4.30% | 4.40% | |

| 15:00 | USD | Existing Home Sales Oct | 3.91M | 3.96M | ||

| 19:00 | USD | FOMC Minutes |