Subdued Trading and Anticipation for RBA Minutes – Action Forex

Activity in the global financial markets are rather muted today, with major European stock indexes reading water within a narrow range. US futures are also showing little change, reflecting the quietness of US market holiday. In the currency sphere, movements are similarly subdued, with Euro and Swiss Franc ranking as the day’s weaker currencies followed by Dollar. Kiwi, Aussie, and Yen are having relative strength. Sterling and Swiss Franc find themselves positioned in the middle, presenting mixed performance.

The upcoming Asian trading session, however, promises an uptick in market volatility, with release of RBA minutes highly anticipated. At its February board meeting, RBA maintained official cash rate at 4.35%, aligning with market expectations. Notably, the central bank chose not to abandon its tightening bias. Governor Michele Bullock’s stance, that another rate hike remains a possibility but is not definitively on the cards, has sparked keen interest. The forthcoming minutes are expected to shed light on whether an additional hike was seriously considered and the degree of contention surrounding this decision.

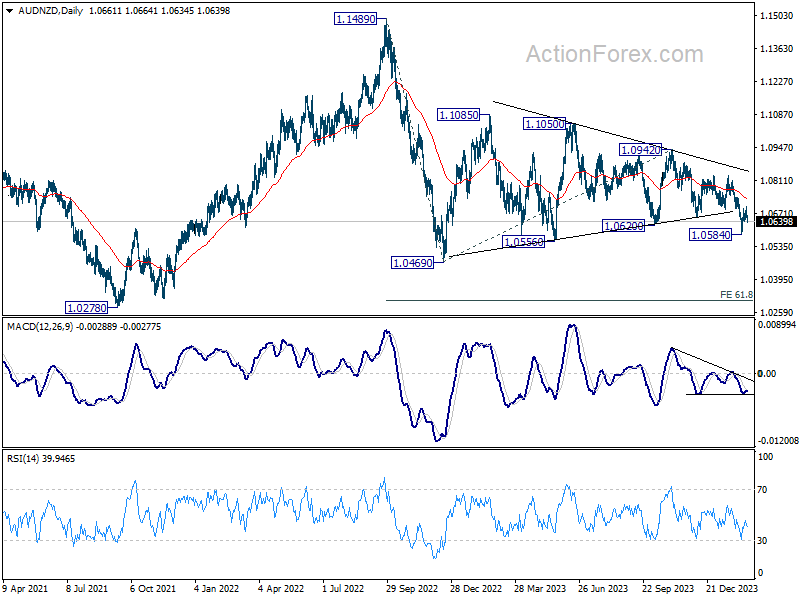

Technically, AUD/NZD recovered after dipping to 1.0584 earlier in the month. But there is no change in the bearish outlook with 55 D EMA (now at 1.0735) intact. Deeper decline is expected and break of 1.0584 will target 1.0469 (2022 low). Firm break there will resume whole down trend from 1.14879 (2022 high).

In Europe, at the time of writing, FTSE is up 0.15%. DAX is down -0.28%. CAC is down -0.19%. UK 10-year yield is down -0.0074 at 4.107. Germany 10-year yield is up 0.009 at 2.417. Earlier in Asia, Nikkei fell -0.04%. Hong Kong HSI fell -1.13%. China Shanghai SSE rose 1.56%. Singapore Strait Times rose 0.12%. Japan 10-year JGB yield fell -0.0004 to 0.730.

Bundesbank: Weak German economy but no significant, broad-based and long-lasting decline

In its latest monthly report, Bundesbank acknowledged that the “weak phase” in the German economy since Russian war of aggression against Ukraine would continue.

Despite this, it stops short of predicting a recession, defining it as a “significant, broad-based and long-lasting decline in economic output.”

The report further elaborates, indicating “no signs of an impending noticeable deterioration” in the labor market stemming from the current economic slowdown.

On the inflation front, Bundesbank anticipates continued decline in inflation rates in the coming months, with price pressures on food and other goods expected to ease further. Nonetheless, the report signals slower pace of decline in service sector inflation, attributing this trend partly to “continued strong wage growth.”

NZ BNZ services rises to 52.1, springs back to growth

New Zealand’s BusinessNZ Performance of Services Index rose from 48.8 to 52.1 in January, marking its highest peak since May 2023. This rebound places the sector back into expansion, albeit slightly below long-term average of 53.4.

Components of the PSI showed notable improvements: activity/sales surged to 53.0 from 47.2, employment edged up to 48.1 from 47.2, new orders/business increased to 51.8 from 50.8, and stocks/inventories rose to 53.5 from 51.7. However, a decrease in supplier deliveries to 48.7 from 50.3 hints at logistical challenges.

Reflecting on the sector’s performance, BusinessNZ’s chief executive, Kirk Hope, remarked on the “seesaw” trend between expansion and contraction observed in recent months. He highlighted that the sector’s sustained recovery hinges on “continued momentum” in business activity and new orders, coupled with alleviation in “cost of living” pressures.

BNZ Senior Economist Doug Steel provided an optimistic outlook, suggesting that the combined PMI and PSI activity indicator hints that “annual GDP growth will soon turn positive.” Yet Steel cautioned that further progress is essential to mitigate growing spare capacity within the economy.

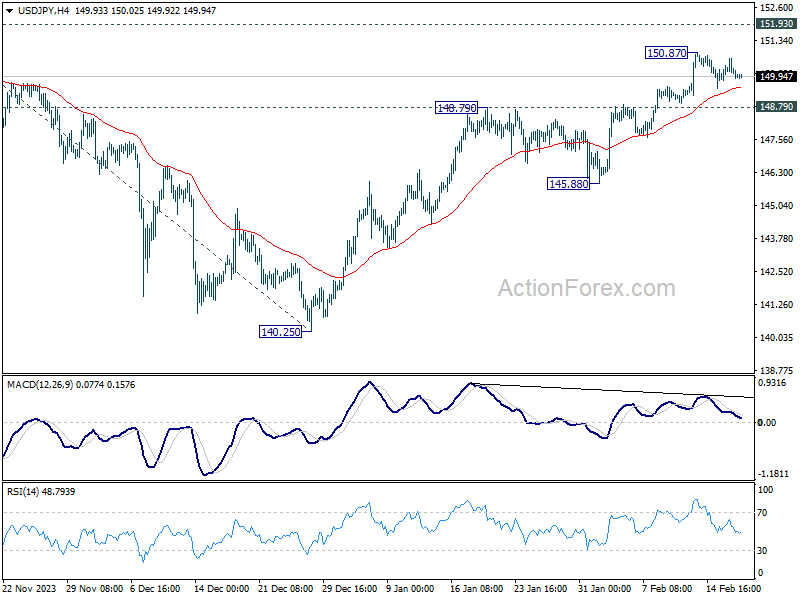

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.81; (P) 150.23; (R1) 150.63; More…

USD/JPY is extending the consolidation from 150.87 and intraday bias remains neutral. Downside of retreat should be contained by 148.79 resistance turned support to bring another rally. Above 150.87 will resume the rise from 140.25 to 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next. However, firm break of 148.79 will turn bias to the downside for 145.88 support.

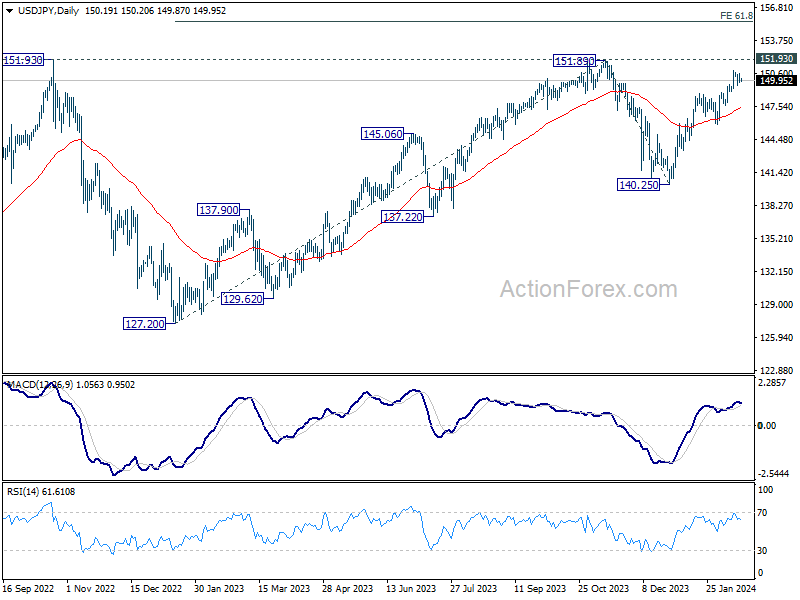

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Jan | 52.1 | 48.8 | ||

| 23:50 | JPY | Machinery Orders M/M Dec | 2.70% | 2.50% | -4.90% | |

| 00:01 | GBP | Rightmove House Price Index M/M Feb | 0.90% | 1.30% | ||

| 11:00 | EUR | German Buba Monthly Report | ||||

| 13:30 | CAD | Industrial Product Price M/M Jan | -0.10% | 0.10% | -1.50% | |

| 13:30 | CAD | Raw Material Price Index Jan | 1.20% | 0.80% | -4.90% |