Yen Falters in Risk-On Environment, Dollar Seeks Comeback With Surging Yields – Action Forex

Global financial markets are currently basking in a robust wave of risk-on sentiment, evidenced by Japan’s Nikkei and Europe’s Stoxx 600 indices reaching new record highs. The optimism is further bolstered by promising US futures, with the technology sector leading the charge, significantly propelled by Nvidia’s impressive results. This surge in tech enthusiasm is largely fueled by the ongoing artificial intelligence boom, which seems poised to captivate market sentiment for the foreseeable future.

In the currency markets, Japanese Yen emerges as the most significant underperformer, embodying the broad risk-on sentiment that typically sees investors moving away from safe-haven assets. Swiss Franc also finds itself on the weaker side, echoing a similar sentiment. However, development in other currencies are less clear.

While Dollar experienced some pressure earlier in the day, it’s is attempting a rebound in early US session, buoyed by rally in Treasury yields. Euro found support from improvement in PMI data, particularly with France showing robust performance that helped counterbalance weak Germany’s. Accounts from the European Central Bank (ECB) meeting revealed policymakers’ apprehensions regarding premature policy easing. However, this has not translated into sustained momentum for the common currency.

As it stands, New Zealand and Australian Dollar lead as the frontrunners in the currency markets, benefiting from the risk-on environment. Euro follows, while the Sterling lags behind alongside Swiss Franc. Yet, the dynamic nature of the markets suggests that these positions could shift by the end of US session.

In Europe, at the time of writing, FTSE is up 0.25%. DAX is up 1.55%. CAC is up 1.09%. UK 10-year yield is down -0.0060 at 4.105. Germany 10-year yield is down -0.002 at 2.446. Earlier in Asia, Nikkei rose 2.19%. Hong Kong HSI rose 1.45%. China Shanghai SSE rose 1.27%. Singapore Strait Times rose 0.18%. Japan 10-year JGB yield fell -0.0045 to 0.721.

US initial jobless claims falls to 201k

US initial jobless claims fell -12k to 201k in the week ending February 17, below expectation of 217k. Four-week moving average of initial claims fell -3.5k to 215k.

Continuing claims fell -27k to 1862k in the week ending February 10. Four-week moving average of continuing claims rose 8.5k to 1878k, highest since December 11, 2021.

Canada’s retail sales rises 0.9% mom in Dec, slightly above expectation

Canada’s retail sales rose 0.9% mom to CAD 67.3B in December, slightly above expectation of 0.8% mom. Sales were up in five of nine subsectors and were led by increases at motor vehicle and parts dealers (+1.9%). In volume terms, retail sales increased 0.8% in December.

Retail sales were up 1.0% in Q4, marking a second consecutive quarterly increase. In volume terms, retail sales increased 1.3% in the quarter.

Advance estimate suggests that sales decreased -0.4% mom in January.

ECB minutes reveal consensus on prematurity of rate cut discussions

Accounts of ECB’s January 24-25 meeting showed that reveal a cautious stance among its members towards the idea of interest rate cuts. Officials reached a “broad consensus” on the notion that discussing rate cuts at this juncture was “premature” with many members emphasizing “risk management considerations” as a foundation for this perspective. The “risk of cutting policy rates too early was still seen as outweighing that of cutting rates too late”, the minuted noted.

Members also emphasized the “high reputational costs” that could arise from having to reverse policy direction should economic conditions improve unexpectedly, wage growth pick up pace, or if new inflationary pressures were to surface. Such a scenario, they argued, could undermine the credibility of ECB’s policy framework and its commitment to price stability.

Furthermore, the discussion acknowledged that while financial markets have already begun to anticipate rate cuts in 2024, leading to a somewhat “loosening of both financial and financing conditions,” this anticipation could be deemed “premature.” There was a concern that acting on market expectations too soon could inadvertently “derail or delay” the efforts to steer inflation back to its target level in a timely manner.

Eurozone CPI finalized at 2.8% in Jan, core at 3.3%

Eurozone PMI was finalized at 2.8% yoy in January, down from December’s 2.9% yoy. Core CPI was finalized at 3.3% yoy, down from prior month’s 3.4% yoy. The highest contribution to came from services (+1.73 percentage points, pp), followed by food, alcohol & tobacco (+1.13 pp), non-energy industrial goods (+0.53 pp) and energy (-0.62 pp).

EU CPI was finalized at 3.1% yoy. The lowest annual rates were registered in Denmark, Italy (both 0.9%), Latvia, Lithuania and Finland (all 1.1%). The highest annual rates were recorded in Romania (7.3%), Estonia (5.0%) and Croatia (4.8%). Compared with December, annual inflation fell in fifteen Member States, remained stable in one and rose in eleven.

Eurozone PMI composite rises to 48.9, a step towards recovery amid German drag

Eurozone PMI Manufacturing dipped further from 46.6 to 46.1 in February, undershooting expectations of a 47.1 reading and signaling continued contraction. Conversely, PMI Services climbed from 48.4 to neutral mark of 50.0, surpassing the forecast of 48.7 and reaching a 7-month high. This uplift in services contributed to PMI Composite’s rise from 47.9 to 48.9, marking an 8-month peak yet still indicating slight overall economic contraction.

Norman Liebke, Economist at Hamburg Commercial Bank, cited a “glimmer of hope” as Eurozone edges closer to recovery, particularly within the services sector. Despite the manufacturing downturn, Liebke reaffirms an annual growth forecast of 0.8% for 2024.

ECB is likely to find the latest PMI figures concerning, especially with output prices increasing for the fourth consecutive month, largely driven by labor-intensive services sector grappling with rising wages. ECB is anticipated to make its first interest rate cut in June according to Liebke’s forecast.

The disparity in economic performance between Germany and France is striking. Germany, Europe’s largest economy, appears to be a significant “drag” on the broader Eurozone growth, with its manufacturing sector facing pronounced challenges. In contrast, France is experiencing a more robust recovery across both services and manufacturing.

Germany’s PMI readings for February further underscore its economic difficulties, with PMI Manufacturing plummeting to a 4-month low of 42.3, PMI Services rising from 48.2 and Composite PMI also hitting a 4-month low at 46.1.

On the other hand, France’s economic indicators offer more positive news, with PMI Manufacturing surging to an 11-month high of 46.8, Services PMI rising to an 8-month high at 48.0, and PMI Composite reaching a 9-month high at 47.7.

UK PMI composite rises to 53.3, growth accelerates as inflation concerns loom

UK’s PMI Manufacturing edged up from 47.0 to 47.1, aligning with expectations, while PMI Services was steady at 54.3, just shy of the anticipated 54.4. PMI Composite index rose from 52.9 to 53.3, underscoring a period of accelerated economic growth and marking the highest reading in nine months.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, emphasized the significance, noting that recent uptick is part of a consistent pattern of improvement over the “four straight months”. Williamson’s analysis suggests that the economy is expanding at a quarterly rate of 0.2-0.3% in Q1 2024, signaling that UK’s recessionary phase may have concluded.

Williamson highlighted supply chain disruptions, particularly those related to Red Sea shipping, have led to the most significant delays observed in over 18 months. These disruptions have escalated shipping costs, contributing to a notable increase in selling prices for goods—the largest monthly rise seen in nine months.

Moreover, service sector inflation has edged higher due to increased wage costs and the indirect effects of rising goods prices. The survey data suggest consumer price inflation may hover around 4% in the coming months, doubling BoE’s target rate.

Given these dynamics—accelerating growth coupled with rising prices—February’s PMI data suggests that BoE are “increasingly likely to err on the side of caution” towards reducing interest rates.

Japan’s PMI composite drops to 50.3, from recovery to stagnation

Japan’s PMI Manufacturing dipped further to 47.2 from 48.0, marking the ninth consecutive month of sector contraction and hitting the lowest point since August 2020. PMI Services also declined, albeit more moderate, falling from 53.1 to 52.5. Consequently, Composite PMI, which combines both manufacturing and service sectors, decreased from 51.5 to a near-stagnation point of 50.3.

Usamah Bhatti, Economist at S&P Global Market Intelligence, commented on the recent data, noting that the slight improvement observed at the beginning of the year has “all but evaporate[d]” in February. He described the month’s growth as “only fractional,” attributing it to “softer upturn in services activity” that was insufficient to counterbalance the “steepest contraction in manufacturing output for a year.”

Australia’s Composite PMI climbs to 51.8, diminishing prospects for near-term RBA rate cut

Australia’s PMI Manufacturing fell sharply from 50.1 to 47.7 in February, with Manufacturing Output marking a 45-month low at 45.0. In stark contrast, PMI Services surged to a 10-month high of 52.8, propelling the Composite PMI to 51.8, the first time it has breached the 50-mark threshold since last June.

Warren Hogan, Chief Economic Advisor at Judo Bank, said the PMI results “weaken the case for monetary policy easing any time soon”. Improvement in activity indicators and modest rise in price indexes suggest that “risks to monetary policy remain even balanced”.

Hogan’s analysis also points to an economy that is gaining momentum, expanding at more vigorous pace in 2024 compared to the latter half of 2023. He posits that continuous improvements could herald stronger economic growth this year than the last, hinting that “soft landing is behind us”.

Furthermore, Composite Employment Index reached its highest level since last September, indicating “rising labour demand and employment growth” in the overall economy. This is accompanied by intensifying price pressures, with Composite Output Price Index’s climb to its highest point since last September 2023, indicating that domestic inflation could be hovering between 4% and 5%. Hogan cautions that the recent trend of disinflation “may well have run its course.”

New Zealand’s trade deficit widens, exports falls -7.1% yoy and imports down -20% yoy

New Zealand’s trade activity in January showed notable downturn, with goods exports dropping by -7.1% yoy to NZD 4.9B and goods imports declining by a substantial -20.0% yoy to NZD 5.9B. This resulted in trade deficit of NZD -976m, significantly larger than the anticipated NZD -200m.

A closer examination of the data reveals Australia as the leading contributor to the monthly fall in New Zealand’s exports, with a -17% decrease amounting to NZD -112m. Not far behind, Japan saw a dramatic -34% reduction in its exports from New Zealand, translating to NZD -105m. Conversely, EU was a rare bright spot, where New Zealand’s exports actually increased by 5.8%, or NZD 15m. Other major trading partners like China and the USA also experienced declines in exports from New Zealand, by -2.8% (NZD -42m) and -5.6% (NZD -31m), respectively.

On the import side, EU recorded the most significant monthly drop, with imports falling by -33% to NZD -386m. South Korea followed closely with a -34% decrease, equating to NZD -286m. Other notable decreases in imports came from China (NZD -84m, -5.4%), Australia (NZD -57m, -9.2%), and the USA (NZD -30m, -5.6%).

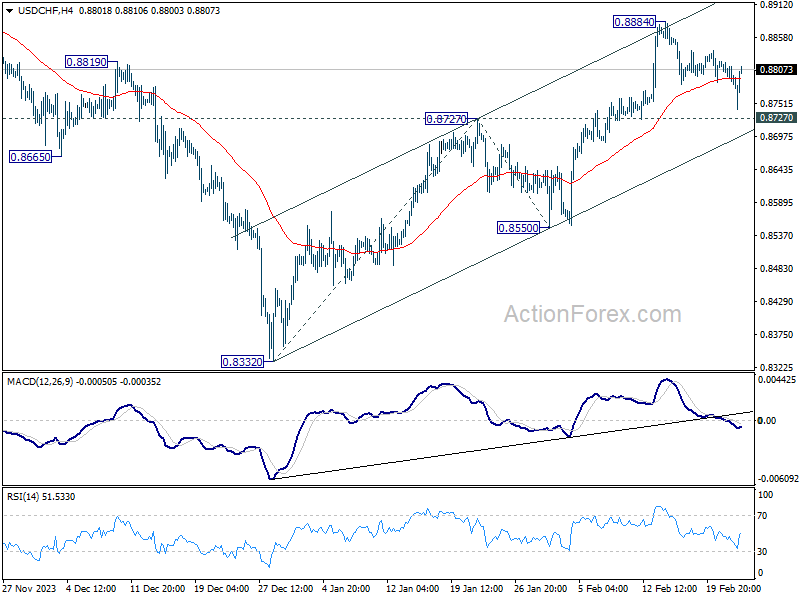

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8783; (P) 0.8802; (R1) 0.8816; More….

Despite earlier dip, USD/CHF recovered ahead of 0.8727 resistance turned support. Intraday bias remains neutral and further rally is still expected. On the upside, break of 0.8885 will resume the rise from 0.8332 and target and 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

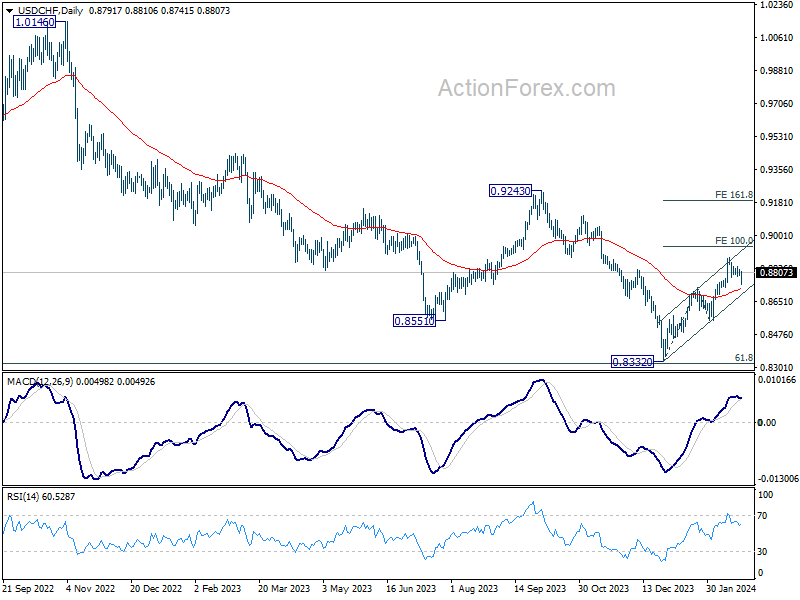

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support. It’s still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Jan | -976M | -200M | -323M | -368M |

| 22:00 | AUD | Manufacturing PMI Feb P | 47.7 | 50.1 | ||

| 22:00 | AUD | Services PMI Feb P | 52.8 | 49.1 | ||

| 00:30 | JPY | Manufacturing PMI Feb P | 47.2 | 48.2 | 48 | |

| 00:30 | JPY | Services PMI Feb P | 52.5 | 53.1 | ||

| 08:15 | EUR | France Manufacturing PMI Feb P | 46.8 | 44 | 43.1 | |

| 08:15 | EUR | France Services PMI Feb P | 48 | 45.6 | 45.4 | |

| 08:30 | EUR | Germany Manufacturing PMI Feb P | 42.3 | 46.1 | 45.5 | |

| 08:30 | EUR | Germany Services PMI Feb P | 48.2 | 48 | 47.7 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Feb P | 46.1 | 47.1 | 46.6 | |

| 09:00 | EUR | Eurozone Services PMI Feb P | 50 | 48.7 | 48.4 | |

| 09:30 | GBP | Manufacturing PMI Feb P | 47.1 | 47.1 | 47 | |

| 09:30 | GBP | Services PMI Feb P | 54.3 | 54.4 | 54.3 | |

| 10:00 | EUR | Eurozone CPI Y/Y Jan F | 2.80% | 2.80% | 2.80% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan F | 3.30% | 3.30% | 3.30% | |

| 12:30 | EUR | ECB Meeting Accounts | ||||

| 13:30 | CAD | Retail Sales M/M Dec | 0.90% | 0.80% | -0.20% | |

| 13:30 | CAD | Retail Sales ex Autos M/M Dec | 0.60% | 0.70% | -0.50% | |

| 13:30 | USD | Initial Jobless Claims (Feb 16) | 201K | 217K | 212K | 213K |

| 14:45 | USD | Manufacturing PMI Feb P | 50.2 | 50.7 | ||

| 14:45 | USD | Services PMI Feb P | 52 | 52.5 | ||

| 15:00 | USD | Existing Home Sales Jan | 3.95M | 3.78M | ||

| 15:30 | USD | Natural Gas Storage | -59B | -49B | ||

| 16:00 | USD | Crude Oil Inventories | 3.9M | 12.0M |