Dollar’s Slide Deepens, Yen Bolstered by Wage Optimism, Euro Awaits ECB – Action Forex

Dollar fell sharply overnight and the broad-based decline extended into Asian session today. Some analysts attributed this selloff to Fed Chair Jerome Powell’s commentary during his Congressional testimony. Powell’s mention of needing “a little bit more data” before contemplating rate cuts has ignited a wave of speculation among investors and analysts alike, interpreting this statement as an implicit nod towards the possibility of a rate cut as soon as May. However, such expectations seem to be only minimally mirrored in Fed funds futures, which currently peg the likelihood of May cut at a modest 20%. Instead, Dollar’s weakness seems more intricately tied to the extended decline in treasury yields, coupled with sustained appetite for riskier assets across global markets.

Meanwhile, Japanese Yen embarked on a significant rally today, spurred by the latest wages growth data from Japan, which exceeded expectations and marked the highest increase since last June. This robust wage growth intensified speculation around rate hike by BoJ at this month’s meeting. Adding fuel to the fire, remarks from BoJ board member Junko Nakagawa have lent further credence to the prospect of imminent monetary tightening. The positive momentum for Yen is also supported by encouraging developments within Japan’s labor market. Notably UA Zensen, Japan’s foremost industrial labor group, reported that 25 of its member unions have successfully secured their wage demands in full from management. The culmination of these wage negotiations over the next week is eagerly anticipated, setting the stage for BoJ’s policy decision on March 19.

As for the week, Yen is currently the standout performer. Australian and New Zealand Dollars are trailing closely behind, buoyed by China’s better-than-expected trade data. Conversely, Dollar languishes at the bottom of the performance chart, with Swiss Franc and Canadian Dollar also facing downward pressures. Euro and the Sterling occupy the middle ground, with all eyes set on the impending ECB rate decision and its accompanying economic projections for further directional cues.

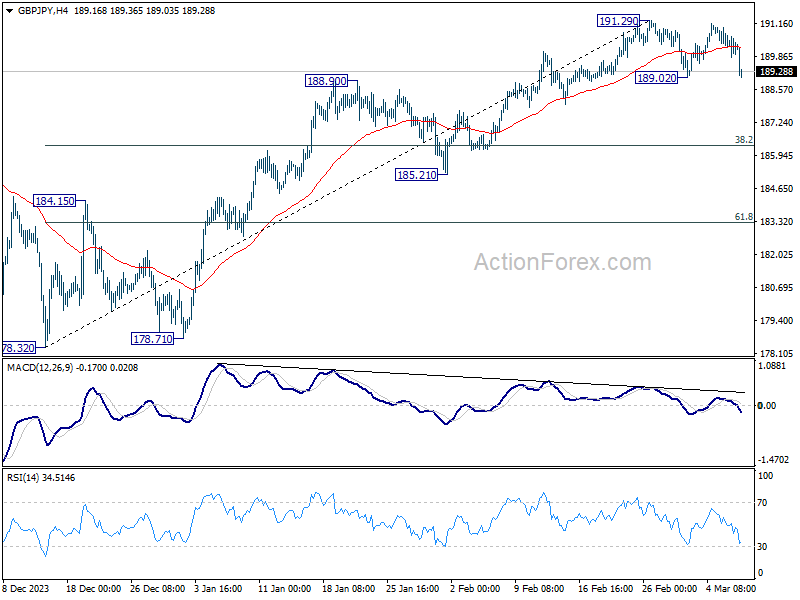

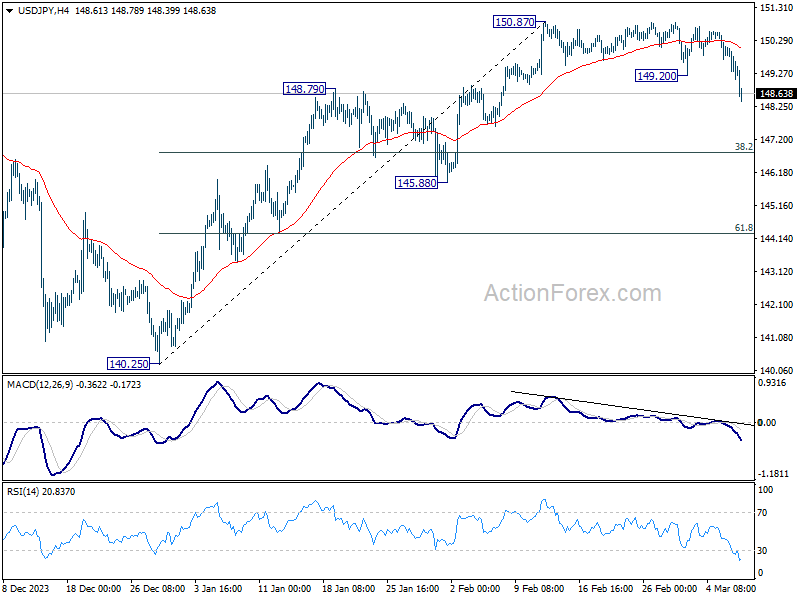

Technically, USD/JPY’s firm break of 149.20 is probably a leading signal of near term bearish signal in Yen pairs. Attention will now be on 161.67 support in EUR/JPY and 189.02 support in GBP/JPY. Decisive break of these levels will open up deeper, broad-based decline in Yen pairs, even as a corrective pullback.

In Asia, at the time of writing, Nikkei is down -1.00%. Hong Kong HSI is down -0.56%. China Shanghai SSE is down -0.23%. Singapore Strait Times is down -0.08%. Japan 10-year JGB yield is up 0.0170 at 0.735. Overnight, DOW rose 0.20%. S&P 500 rose 0.51%. NASDAQ rose 0.58%. 10-year yield fell -0.033 to 4.104.

BoJ’s Nakagawa: Promising cycle of wages and inflation on the horizon

BoJ board member Junko Nakagawa highlighted a promising outlook for wage growth, expressed confidence in the emergence of a positive cycle between inflation and wages, a prerequisite for the central bank to exit negative interest rate.

“We can say that prospects for the economy to achieve a positive cycle of inflation and wages are in sight,” she stated, pointing to a shift in the wage-setting behavior of companies as a sign of economic optimism.

According to Nakagawa, there are “clear signs of change in how companies set wages,” with businesses increasingly inclined to offer annual pay raises in response to the ongoing labor shortages. This adjustment marks a significant departure from previous practices and suggests that companies are prepared to propose wage increases surpassing those of the previous year.

“Japan is moving steadily towards sustainably and stably achieving our 2% inflation target,” she remarked.

Japan’s nominal wage growth hits seven-month high, real wages still in decline

Japan’s nominal wage growth surged by 2.0% yoy in January, surpassing expectations of 1.3%, and marking the most substantial growth since last June. This also represents a notable acceleration from the revised 0.8% increase observed in December.

The surge in wages largely stems from a significant 16.2% yoy advance in special payments, which include winter bonuses. Regular or base salaries maintained steady growth rate of 1.4% yoy, consistent with the previous month’s performance. Meanwhile, overtime pay, a key indicator of labor demand and economic activity, showed slight improvement of 0.4% yoy, recovering from revised decline of -1.2% yoy in the prior period.

Real wages declined by 0.6% yoy, marking a continued decrease in purchasing power for Japanese workers. However, the pace of decline was the joint-slowest since December 2022, indicating stabilization in the erosion of real earnings.

China’s exports jump 7.1% yoy in Jan-Feb, imports rise 3.5% yoy

Title: China’s Trade Performance Surpasses Expectations Amid PBOC’s Supportive Measures

China’s trade figures for the combined period of January and February have remarkably exceeded expectations, with exports rising by 7.1% yoy , surpassing the anticipated 1.9% increase. Imports also showed a robust performance, climbing 3.5% yoy, which beat the forecast of 1.5% growth.

This led to trade surplus of USD 125.2B, not only exceeding the expected USD 110.3B but also marking an increase from last year’s USD 103.8B during the same period.

Separately, Pan Gongsheng, PBoC, pointed out yesterday that there was room for further reductions in banks’ reserve requirement ratios the percentage of reserves banks are required to hold against deposits. Such a move would free up additional liquidity for lending and investment, potentially stimulating economic activity.

Fed’s Beige Book reveals modest economic growth and easing labor market tightness

Fed’s Beige Book report noted “slight to modest” increase in economic activity across various districts. Specifically, eight districts reported slight to modest growth, three observed no change, and one experienced slight softening in economic conditions.

In the realm of consumer spending, the report indicates slight downturn, especially concerning retail goods. This trend is attributed to a “heightened price sensitivity” among consumers, who are increasingly opting to trade down and shift their spending away from discretionary goods. Manufacturing activity remained “largely unchanged”, with disruptions in shipping through the Red Sea and Panama Canal reportedly having minimal overall impact.

The report also highlights persistent price pressures, although some districts observed moderation in inflation. Businesses are finding it increasingly difficult to pass higher costs onto customers, who are becoming more resistant to price increases. Labor market conditions have shown further signs of improvement, with nearly all districts reporting increased labor availability and enhanced employee retention.

Fed’s Kashkari sees two, or maybe just one rate cut this year

Minneapolis Fed President Neel Kashkari has refined his expectations for interest rate cuts in 2024, now leaning towards possibility of fewer reductions due to robust economic data emerging since the year’s start.

Initially forecasting two rate cuts for the year, Kashkari expressed in a WSJ Live interview that current economic indicators might necessitate only a single cut. “I was at two in December,” he remarked. “It’s hard to see, with the data that’s come in, that I’d be saying more cuts than I had in December, or potentially one fewer, but I haven’t decided.”

Kashkari emphasized that Fed’s “base case scenario” no longer includes further rate hikes. He suggested that should inflation persist beyond current projections, Fed’s immediate response would be to maintain the existing interest rates for “an extended period of time.” rather than implementing additional increases.

Euro mixed awaiting ECB’s rate cut perspective

ECB is widely anticipated to maintain main refinancing rate at 4.50% and deposit rate at 4.00% in today’s meeting. There is clear consensus among officials on the plan for rate cuts this year. However, the timing and pace of these reductions remain subjects of debate among them.

Economists generally agree on a June timeline for the initial rate reduction, citing that current economic indicators do not yet justify an earlier move. Also, ECB is expected to await further wage data due in May, rendering an April cut less probable.

Key points of interest in today’s meeting include: the possibility of a rate cut being actually discussed, any indicative changes in the statement towards policy easing, and, importantly, the new economic projections. These projections are key to understanding the ECB’s confidence in returning inflation to its 2% symmetric target within a feasible timeframe.

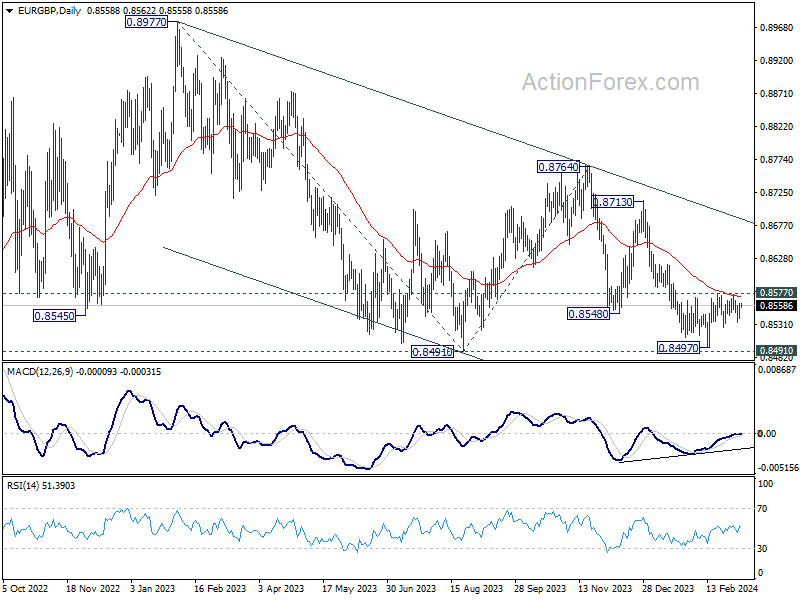

Euro’s performance this week has been mixed, registering gains against Dollar, Swiss Franc, and Canadian Dollar, but falling short against other major counterparts. A significant focal point will be EUR/GBP’s response to the ECB’s decisions.

Decisive break of 0.8577 resistance and sustained trading above 55 D EMA (now at 0.8571) will argue that fall from 0.8764 has completed at 0.8497, after successfully defending 0.8491 medium term support (2023 low). In this case, near term outlook will be turned bullish for stronger rise back towards 0.8713/8764 resistance zone.

On the data front

Swiss unemployment rate and foreign currency reserves, and Germany factory orders will be released in European sesision. Later in the day, Canada will release building permits and trade balance; US will release jobless claims and trade balance.

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.98; (P) 149.53; (R1) 149.97; More…

Intraday bias in USD/JPY back on the downside with strong break of 149.20 support. Fall from 150.87 could either be correcting the rise from 140.25, or completely reversing it. In either case, deeper decline is expected to 38.2% retracement of 140.25 to 150.87 at 146.81. Sustained break there will bolster the latter case, and target 61.8% retracement at 144.30 and below. For now, risk will stay on the downside as long as 150.87 resistance holds, in case of recovery.

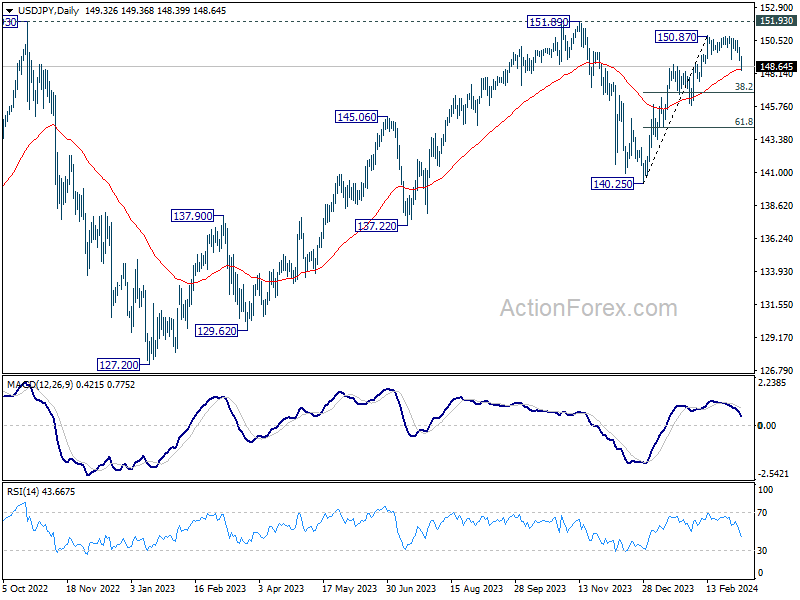

In the bigger picture, outlook is mixed up as fall from 150.87 accelerates lower. Sustained trading below 55 D EMA (now at 148.45) will open up the case that corrective pattern from 151.89 (2023 high) is extending, with fall from 150.87 as the third leg. In this case, deeper decline would be seen to 140.25 support or below. Nevertheless, strong bounce from 55 D EMA will retain near term bullishness for at least another take on 151.89.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Sales Q4 | -0.70% | -2.80% | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Jan | 2.00% | 1.30% | 1.00% | 0.80% |

| 00:30 | AUD | Trade Balance (AUD) Feb | 11.03B | 11.50B | 10.96B | 10.74B |

| 03:00 | CNY | Trade Balance (USD) Feb | 125.2B | 110.3B | 75.3B | |

| 03:00 | CNY | Trade Balance (CNY) Feb | 891B | 620B | 541B | |

| 06:45 | CHF | Unemployment Rate Feb | 2.20% | 2.20% | ||

| 07:00 | EUR | Germany Factory Orders M/M Jan | -6.00% | 8.90% | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Feb | 662B | |||

| 13:15 | EUR | ECB Main Refinancing Rate | 4.50% | 4.50% | ||

| 13:30 | CAD | Trade Balance (CAD) Jan | 0.3B | -0.3B | ||

| 13:30 | CAD | Building Permits M/M Jan | 2.10% | -14% | ||

| 13:30 | USD | Initial Jobless Claims (Mar 1) | 212K | 215K | ||

| 13:30 | USD | Trade Balance (USD) Jan | -63.2B | -62.2B | ||

| 13:30 | USD | Nonfarm Productivity Q4 | 3.20% | 3.20% | ||

| 13:30 | USD | Unit Labor Costs Q4 | 0.50% | 0.50% | ||

| 13:45 | EUR | ECB Press Conference | ||||

| 15:00 | USD | Fed’s Chair Powell testifies | ||||

| 15:30 | USD | Natural Gas Storage | -42B | -96B |