Dollar Edges Lower as PCE Inflation Data Aligns with Expectations, Gold Hits Record – Action Forex

Dollar dips mildly in the wake of the latest PCE inflation data, which largely met market expectations without delivering any significant surprises. Notably, headline inflation saw a slight uptick, primarily driven by rising energy costs. Core inflation saw a slight deceleration from last month’s upwardly revised figures. However, a key point of concern remains the stubbornly high services inflation, which is expected to continue drawing attention from Fed.

Yen is mixed following Tokyo CPI data, which confirmed a slowdown in both core and core-core CPI. This supports BoJ’s cautious approach towards further policy tightening The contraction in industrial production raises flags, although this was offset by a notable uptick in retail sales, showcasing some positive momentum within the economy.

Looking at the week’s performance across currencies, Canadian Dollar emerges as the frontrunner, buoyed by robust Canadian GDP data. Sterling is occupying the second spot in strength, followed by Australian Dollar. Swiss Franc lags as the week’s weakest currency, with Kiwi and Euro trailing. Dollar and Yen find themselves positioned in the middle.

US PCE price index rises to 2.5% yoy in Feb, core PCE down to 2.8% yoy

US personal income rose 0.3% mom or USD 66.5B in February, below expectation of 0.4% mom. Personal spending rose 0.8% mom or USD 145.5B, above expectation of 0.8% mom.

PCE price index rose 0.3% mom below expectation of of 0.4% mom. Core PCE price index (excluding food and energy) rose 0.3% mom, matched expectations. Goods prices increased 0.1% mom while services index surged 0.6% mom. Food prices rose 0.1% mom and energy prices increased 2.3% mom.

Over the 12-month period, PCE price index accelerated from 2.4% yoy to 2.5% yoy, matched expectations. Core PCE price index slowed from upwardly revised 2.9% yoy to 2.8% yoy, matched expectations. Goods prices were up 0.2% yoy while services prices increased 3.8% yoy. Food prices were up 1.3% yoy while energy prices decreased -2.3% yoy.

Tokyo inflation moderates, supporting BoJ’s measured approach

Japan Tokyo CPI core (ex-food) slowed slightly from 2.5% yoy to 2.4% yoy in March, matched expectations. Headline CPI ticked up from 2.5% yoy to 2.6% yoy. CPI core-core (ex-food and energy) also slowed from 3.1% yoy to 2.9% yoy. Service price gains slowed to from 2.1% yoy to 2.0% yoy.

This constellation of data suggests softening of cost-push inflationary pressures within Tokyo, Japan’s economic nucleus, and a concurrent easing in service-sector inflation. This trend could provide BoJ a leverage for a more cautious approach on tightening, despite widespread expectations of another rate hike in the latter half of the year.

Other economic indicators for February released paint a mixed picture. Industrial production fell -0.1% mom, falling short of the anticipated 1.2% growth. In contrast, retail sales outperformed expectations, surging by 4.6% yoy against forecasted 3.0% increase. Meanwhile, unemployment rate rose from 2.4% to 2.6%, exceeding the projected steady rate of 2.4%.

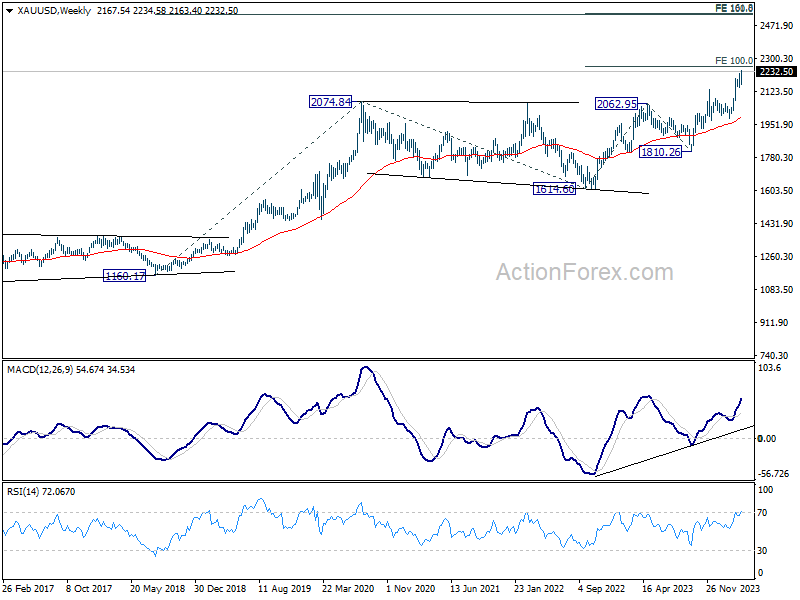

Record-breaking Gold targets 2250, poised for push toward 2500

Gold surges to new record high in quiet holiday trading today. The precious metal continues to be supported by expectation of global central bank easing ahead. SNB has already started rate cutting earlier this month. ECB is widely expected to follow in Spring, probably in June. Whether Fed is going to cut two or three times this year, the cycle will start anyway.

Inflation is looking more like a rear-mirror thing now, and benchmark treasury yields also dip notably recently because of that. US 10-year yield now looks more likely heading back to 4% handle, rather than 4.4%. Germany 10-year yield is back pressing 2.3%, comparing over 2.45% earlier in the month. US 10-year yield is also back to 3.95%, comparing to above 4.2% earlier in the month.

Geopolitical risks is another factor support Gold as there is not end of seen yet with Russian invasion of Ukraine, Israel/Hamas conflicts, nor Houthi’s Red Sea attacks. In addition, US election in November approaching, with far-fetching implications.

Technically, immediate focus is now on 100% projection of 1614.60 to 2062.95 from 1810.26 at 2258.61. Decisive break there would pave the way to 161.8% projection at 2535.69. This level coincides with long term target of 100% projection of 1160.17 to 2074.84 at 1614.60 at 2529.27. So in short, overcoming 2250 handle would send Gold through 2500 mark. In any case, near term outlook will stay bullish as long as 2156.88 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Mar | 2.60% | 2.60% | 2.50% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Mar | 2.40% | 2.40% | 2.50% | |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Mar | 2.90% | 3.10% | ||

| 23:30 | JPY | Unemployment Rate Feb | 2.60% | 2.40% | 2.40% | |

| 23:50 | JPY | Industrial Production M/M Feb P | -0.10% | 1.20% | -6.70% | |

| 23:50 | JPY | Retail Trade Y/Y Feb | 4.60% | 3.00% | 2.10% | |

| 05:00 | JPY | Housing Starts Y/Y Feb | -8.20% | -5.50% | -7.50% | |

| 07:45 | EUR | France Consumer Spending M/M Feb | 0.00% | 0.20% | -0.30% | -0.60% |

| 12:30 | USD | Personal Income M/M Feb | 0.30% | 0.40% | 1.00% | |

| 12:30 | USD | Personal Spending Feb | 0.80% | 0.40% | 0.20% | |

| 12:30 | USD | PCE Price Index M/M Feb | 0.30% | 0.40% | 0.30% | 0.40% |

| 12:30 | USD | PCE Price Index Y/Y Feb | 2.50% | 2.50% | 2.40% | |

| 12:30 | USD | Core PCE Price Index M/M Feb | 0.30% | 0.30% | 0.40% | 0.50% |

| 12:30 | USD | Core PCE Price Index Y/Y Feb | 2.80% | 2.80% | 2.80% | 2.90% |

| 12:30 | USD | Wholesale Inventories Feb P | 0.50% | 0.20% | -0.30% | |

| 12:30 | USD | Goods Trade Balance (USD) Feb P | -91.8B | -89.6B | -90.5B |