SPY flag vs. yields

S&P 500 remained in the consolidation one day longer, bond yields rose and rotations faltered as tech with semis offered short-term buying opportunities rather than selling ones. What follows, is that I still view the market as going higher rather than setting up for a slide, as one with improving internals, and with the sectoral leadership as talked amply lately.

In spite of the rising volatility seen in many high beta stocks, the market as a whole has not topped, and the flaglike structure on the daily offers and offered plenty of opportunities to get in, and enjoy the spurts of risk-on directional volatility such as the one we all benefited from on Wednesday CPI.

Look not further than rate cut odds since that data announcement, how little it changed since – and then see the bond market chart such as the one below, that put in proper context Thursday and Friday rise in yields that didn‘t really make the dollar flourish.

Once we get through the Fed speakers‘ intraday volatility, housing data with services and manufacturing PMI and the usual unemplloyment claims, are what matters. The key point to remember is that right after PPI, Powell again practically ruled out rate hikes, which was also what formed the late Oct bottom. Forget not the market moving NVDA earnings Wednesday after the close – it‘s about guidance.

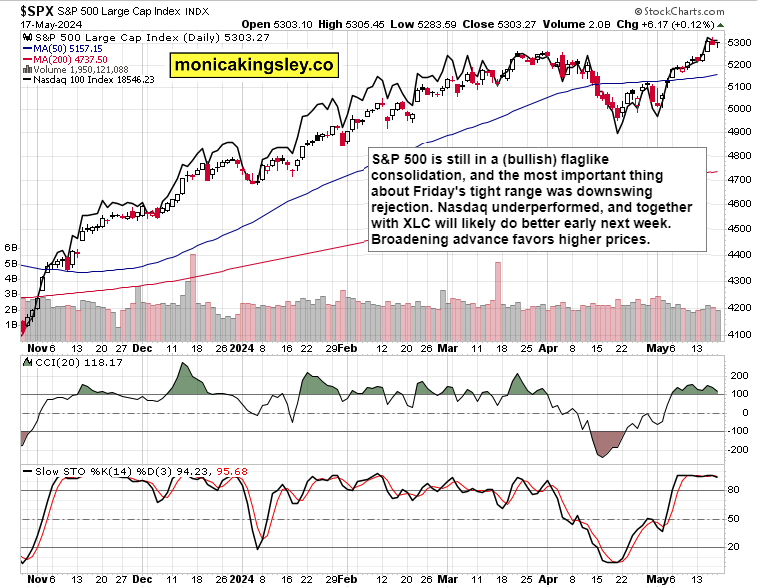

S&P 500 and Nasdaq

-638517537419201431.png)

As written Friday, if not 5,315, then 5,307 as daily supports are to do the job, and they held the late session flush at bay.