Sterling Climb as Markets Dial Back BoE Rate Cut Expectations – Action Forex

Last week, global financial markets were heavily influenced by evolving expectations surrounding central bank monetary easing paths and unexpected political developments. British Pound emerged as the most significant gainer, buoyed by fading expectations of an immediate BoE rate cut in June. This shift was precipitated by latest inflation data and compounded by the UK government’s unexpected decision to hold an election in July. This combination of factors not only boosted the Pound but also contributed to a downturn in FTSE.

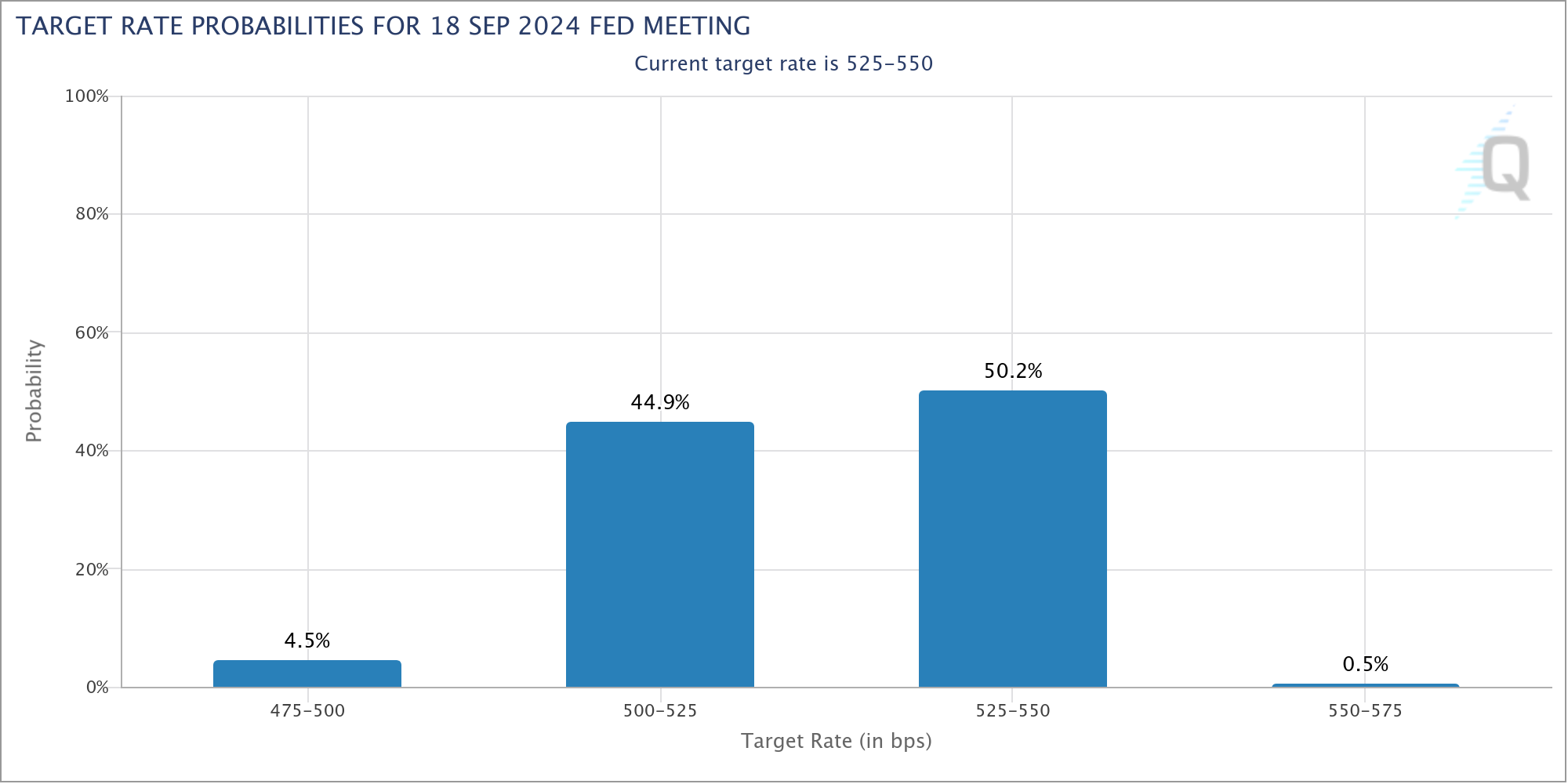

Dollar secured the position as the second strongest currency even though its momentum was relatively weak. Markets adjusted their expectations on Fed, moving away from anticipating a rate cut in September. This reassessment followed revelations from the hawkish tones in FOMC minutes and was supported by robust economic data. In the equity markets, results were mixed; DOW underperformed relative to S&P 500 and, notably, NASDAQ, which benefited from sector-specific dynamics.

Euro ranked as the third strongest performer after ECB officials moderated expectations for further policy easing beyond the anticipated conditional cut in June. This cautious stance from the ECB helped temper aggressive market speculations about continued easing.

Conversely, Australian Dollar was the week’s weakest performer. Despite hawkish minutes from RBA, Aussie was adversely affected by a broader shift in global market sentiment, especially with regards to China. Yen and Swiss Franc also underperformed, reflecting broader trends in risk sentiment and monetary policy expectations.

New Zealand Dollar found itself in a middling position despite hawkish hold by RBNZ. Canadian Dollar also displayed mixed performance amidst these global shifts.

Sterling Rallies as Expectations for BoE Rate Cut Deferred to August

Sterling stood out as last week’s best performer, buoyed by the CPI report that came in stronger than anticipated, thus tempering expectations for an imminent rate cut by BoE in June. While the headline inflation rate for April showed significant deceleration, dropping from 3.2% to 2.3%, and core inflation also decreased from 4.2% to 3.9%, both figures exceeded market predictions.

More concerning was that services inflation only slightly decreased from 6.0% to 5.9%. That pointed to continued elevated domestic price pressures, particularly in sectors less responsive to monetary policy adjustments. This subtle decline indicates that underlying inflationary forces remain elevated.

Complicating matters further, former BoE policymaker Michael Saunders commented on the impact of UK government’s decision to hold an election on July 4. He noted that this political event solidified the already unlikely prospect of a June rate cut. BoE has since declared a moratorium on all speeches and public statements by its policymakers during the election campaign period. This communication blackout limits the Bank’s ability to prepare the markets for and elucidate the rationale behind a June rate cut, effectively taking such a move off the table.

Despite this, several top BoE officials have continued to suggest that a rate cut later in the summer could be feasible. Leading economists from major banks, including Goldman Sachs Group Inc., Morgan Stanley, HSBC Holdings Plc, and Barclays Plc, have adjusted their forecasts, now projecting that BoE will likely lower borrowing costs in August instead of the upcoming June policy meeting.

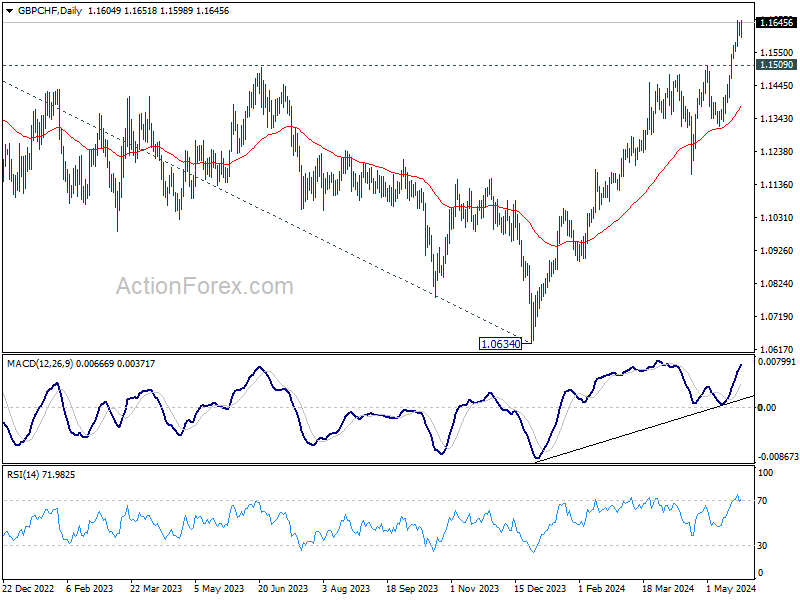

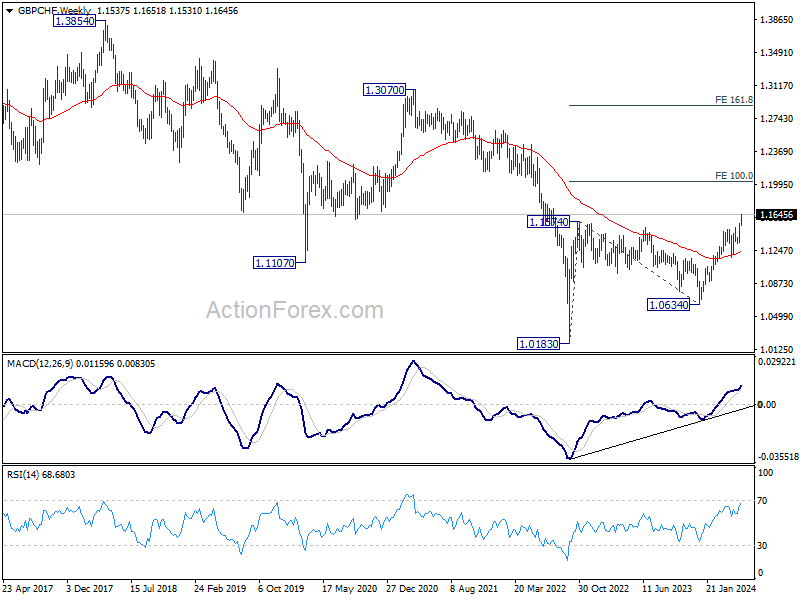

GBP/CHF finally broke through 1.1574 resistance to resume the medium term rebound from 1.0183 (2020 low). Near term outlook will stay bullish as long as 1.1509 resistance turned support holds. Next target is 100% projection of 1.083 to 1.1574 from 1.0634 at 1.2025. Sustained break there could prompt further upside acceleration, and strengthen the case of long term bullish trend reversal.

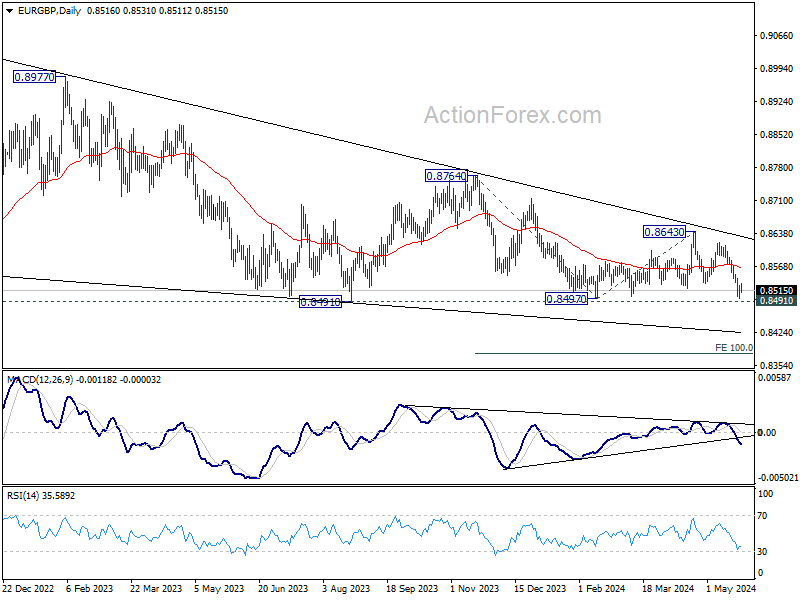

EUR/GBP is now eyeing 0.8491/7 key support zone. Decisive break there will confirm resumption of whole down trend from 0.9267 (2022 high). Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Fall from could be interpreted as the third leg of the pattern from 0.9499 (2020 high0. Firm break of 0.8376 would pave the way towards 0.8201 (2022 low).

FTSE extended the correction from 8474.41 record high in response to the developments. First level support is seen as 223.6% retracement of 7404.08 to 8474.41 at 8221.81. Strong support from there will keep the correction a near term one. Further break of 8474.41 will target 100% projection of 6707.62 to 8047.06 from 7404.08 at 8743.52. However, strong break of 8221.81 will indicate that lengthier and deeper correction is underway to 38.2% retracement at 8065.81 instead.

Australian Dollar Struggles Despite Bullish Domestic Developments

Australian Dollar the week as the weakest performer despite some bullish domestic developments. According to minutes from RBA’s meeting on May 7, a rate hike was indeed contemplated but ultimately set aside. The decision to maintain the cash rate target at 4.35% was only based on the assessment that recent economic data did not yet justify a change in policy.

Further domestic data showed robust economic activity, with April’s PMIs indicating that the economy remains solidly in expansion territory. At the same time, composite input price index, reached a six-month high, and manufacturing input prices at a one-year peak, with service industry cost pressures rising slightly, suggest persistent inflation pressures that are unlikely to abate in the near term.

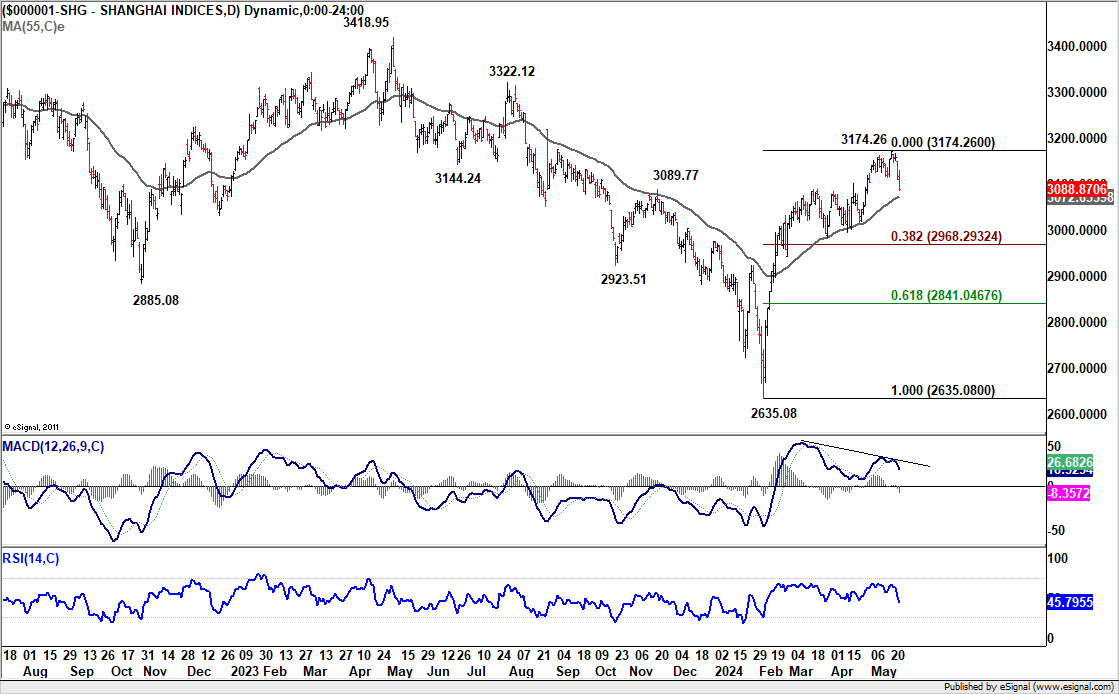

Aussie’s weakness was more attributed to the downturn in global risk sentiment, including the developments in China. Shanghai SSE experienced significant declines on Thursday and Friday, reacting to the realization that high US interest rates might persist longer than previously expected. Additionally, geopolitical tensions flared as China conducted military exercises around Taiwan for consecutive days, as so-called “punishment” on Taiwan’s new President Lai Ching-te after his inauguration.

A short term top should be formed at 3174.26 in Shanghai SSE, on bearish divergence condition in D MACD. Deeper correction could be seen through 55 D EMA (now at 3088.87). But strong support should emerge from 38.2% retracement of 2635.08 to 3174.26 at 2968.29 to bring rebound. That is, 3000 psychological level should broadly hold. Another rise through 3174.26 remains in favor. But for the near term, extended pullback in SSE could cap Aussie’s rebound.

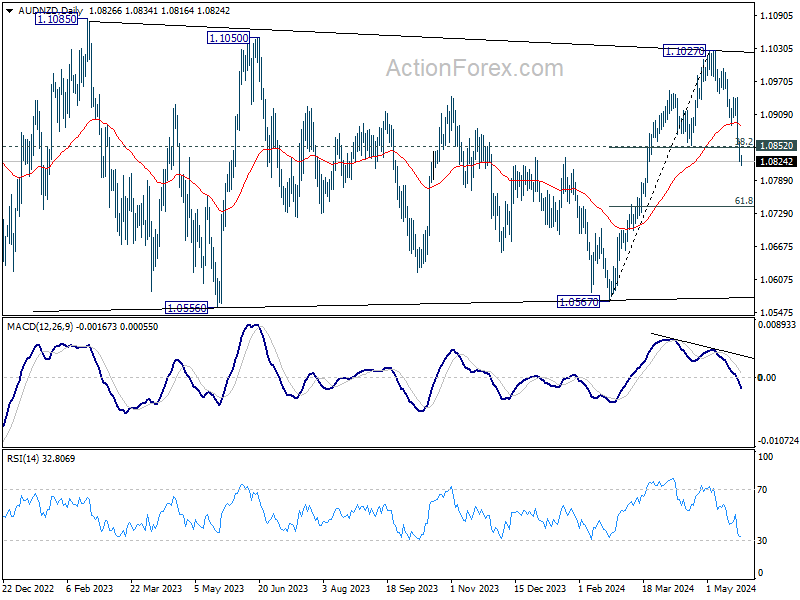

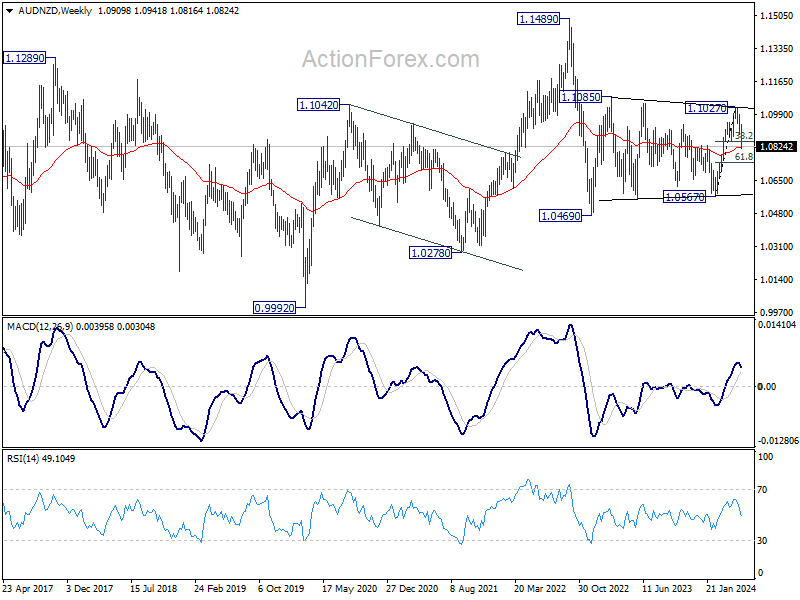

Compounding Australian Dollar’s challenges was its performance selloff against New Zealand Dollar. RBNZ’s decision to hold Official Cash Rate unchanged at 5.50% came with a hawkish tilt. The central bank raised its projected rate path, indicating increased possibility of a rate hike later this year while pushing the timeline for rate cuts to the latter half of 2025.

AUD/NZD’s break of 1.0852 cluster support (38.2% retracement of 1.0567 to 1.1027 at 1.0851) suggests that whole rise from 1.0567 has completed at 1.1027, ahead of 1.1050/85 key resistance zone. Fall from 1.1027 is now seen as another downleg in the medium term range pattern from 1.1085. Deeper fall should be seen to 61.8% retracement at 1.0743, or even to 1.0567 support.

Hawkish FOMC Minutes Spur Sentiment Change, Leading to Dollar Recovery

Sentiment in the US financial markets displayed notable divergence. DOW closed the week down -2.33%, marking its first negative week after four consecutive weeks of gains. In contrast, NASDAQ demonstrated resilience with 1.41% increase, while S&P 500 ended nearly flat, edging up by a mere 0.03%.

This mixed performance in major indexes came amid shifting expectations regarding US monetary policy. The minutes from the latest FOMC meeting indicated that there is an openness among various participants to tighten monetary policy further if inflation risks escalate to a degree that necessitates such action.

This revelation has led economists and traders to recalibrate their expectations regarding the timing of Fed’s first rate cut. The likelihood of a 25 bps reduction in September has now diminished to just under 50%. Furthermore, the market has also begun to price in a 0.5% chance of a rate hike—a scenario that had not been considered likely for some time.

There are various interpretation in DOW’s price actions. The first line of support could come from 55 D EMA (now at 38856.99). Strong rebound from there will keep the corrective pattern from 40077.40 relatively brief. However, considering bearish divergence condition in D MACD, strong break of 55 D MEA will argue that lengthier correction is underway, with risk of deeper pullback to 38.2% retracement of 32327.20 to 40077.50 at 37116.82.

While Dollar index recovered fro medium term rising channel support, momentum has been far from convincing. Risk will stay on the downside as long as 105.74 resistance holds. Firm break of 104.08 would indicate that whole rise from 100.61 has completed with three waves up to 106.51 already. Fall from 106.51, as another down leg in the sideway pattern from 99.57, would target 102.35 and then 100.61. Nevertheless, break of 105.74 will retain near term bullishness.

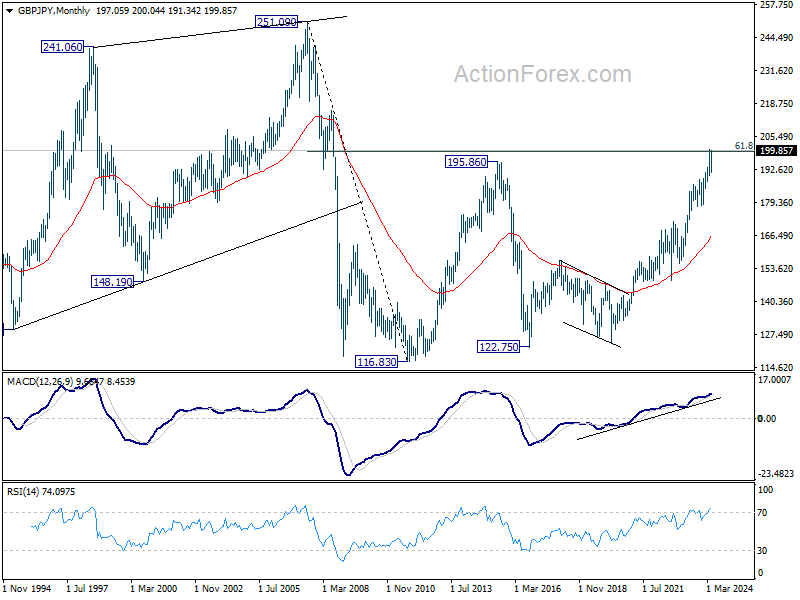

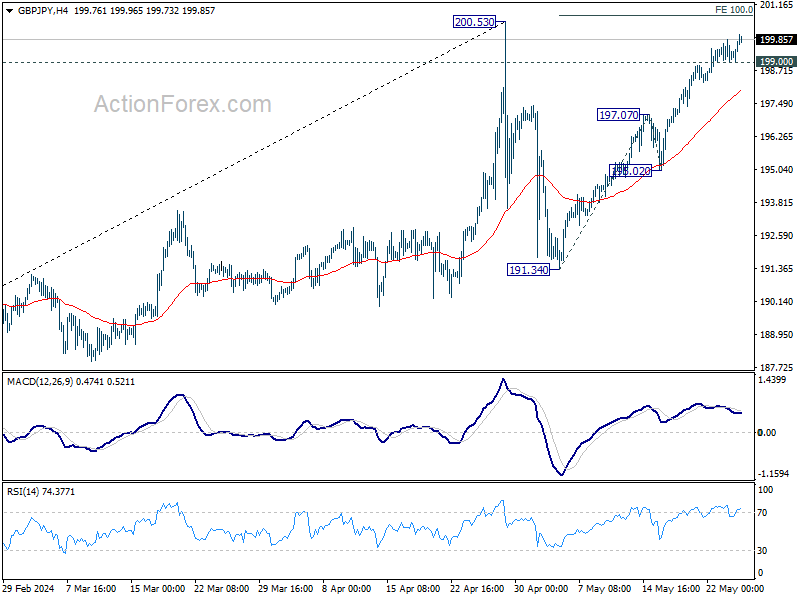

GBP/JPY Weekly Outlook

GBP/JPY’s rally from 191.34 continued last week and outlook is unchanged. This rise is still seen as the second leg of the corrective pattern from 200.53. Initial bias stays on the upside for 100% projection of 191.34 to 180.07 from 195.02 at 200.75. But upside should be limited there. On the downside, below 198.25 minor support will turn intraday bias neutral first. Further break of 197.07 will argue that the third leg has started, and target 191.34 support and possibly below.

In the bigger picture, a medium term top could be in place at 200.53 after breaching 199.80 long term fibonacci level. As long as 55 W EMA (now at 183.92) holds, price actions from there is seen as correcting the rise from 178.32 only. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 178.32 support.

In the longer term picture, rise from 122.75 (2016 low) is seen as the third leg of the pattern from 116.83 (2011 low). Focus is now on 61.8% retracement of 251.09 (2007 high) to 116.83 at 199.80. Decisive break there would pave the way back to 251.09 in the long term.