Swiss Franc Outperforms as Global Inflation Data Lack Lasting Impact on Forex – Action Forex

Inflation data were the key drivers in the forex markets last week, though they failed to produce any sustained movements across major currencies. Australian Dollar rallied following robust CPI figures, yet its gains were limited by the prevailing risk-off sentiment in the region.

Similarly, Euro received a modest boost after unexpected acceleration in inflation, but traders remained cautious, opting to wait for the upcoming ECB rate decision and economic projections before making significant bets. In US, PCE inflation data provided relief to stock investors, contributing to stabilization of risk sentiments that subsequently placed pressure on the Dollar.

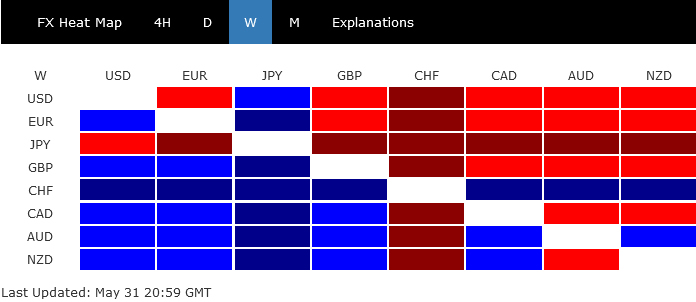

In terms of performance rankings, Swiss Franc dominated as the most impactful mover, significantly bolstered by SNB’s intervention signals. Australian and New Zealand Dollars rounded out as the next strongest. Conversely, Japanese Yen was the weakest, though it stayed above its near-term support against most counterparts. Dollar and Euro trailed as the second and third weakest, respectively, while British Pound and Canadian Dollar closed the week with middling performances.

Swiss Franc Rises as SNB Fires Warning Shot on Intervention

Swiss Franc ended as the standout performer in currency markets last week, primarily driven by SNB Chair Thomas Jordan’s emphatic remarks concerning the currency’s weak exchange rate. Jordan’s comments, which effectively served as a “warning shot” to the markets, signaled reduced tolerance for further weakness in the Franc.

Jordan, speaking at an event in Seoul, highlighted a weaker Franc remains the most likely catalyst for rising inflation in Switzerland. He suggested that SNB might intervene in the currency markets by selling foreign currencies to counteract this trend.

Additionally, robust Swiss GDP data also played a role in recalibrating market expectations of more policy easing by SNB in the near term. Probability of another rate cut in June is now perceived to be around 40%, a significant reduction from the over 65% chance seen at the beginning of May.

Despite the potential for more near-term rebound in the Franc, upside potential appears relatively limited. This is partly because SNB’s primary concern is preventing excessive depreciation rather than aggressively driving up the exchange rate. Additionally, interest rate differential between SNB and other major central banks is expected to remain wide, given that persistent inflation is a global issue.

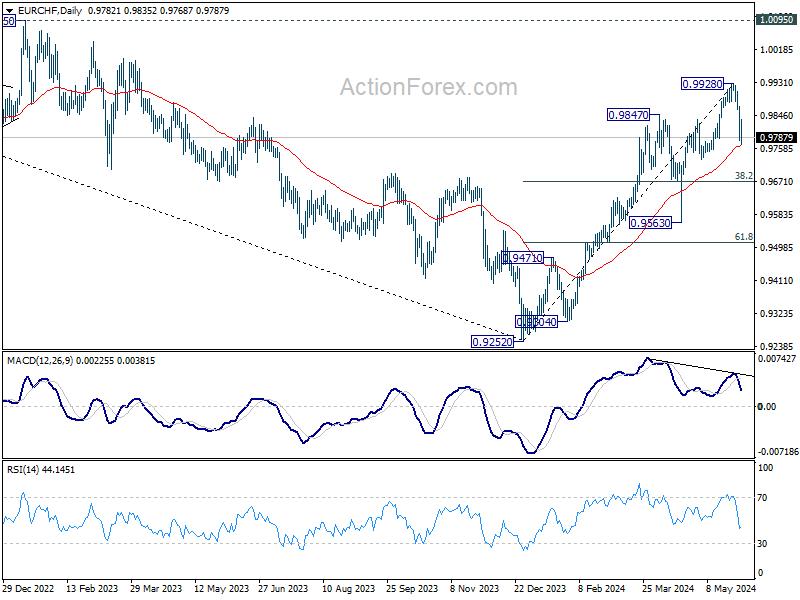

Taking a look at EUR/CHF, bearish divergence condition in D MACD argues that 0.9928 might already be a medium term top. Price actions from there are currently seen as developing into a correction to the up trend from 0.9252 only. Sustained break of 55 D EMA (now at 0.9765), will bring deeper fall to 38.2% retracement of 0.9252 to 0.9928 at 0.9670. Strong support should be seen there to bring rebound to set the range for the corrective pattern.

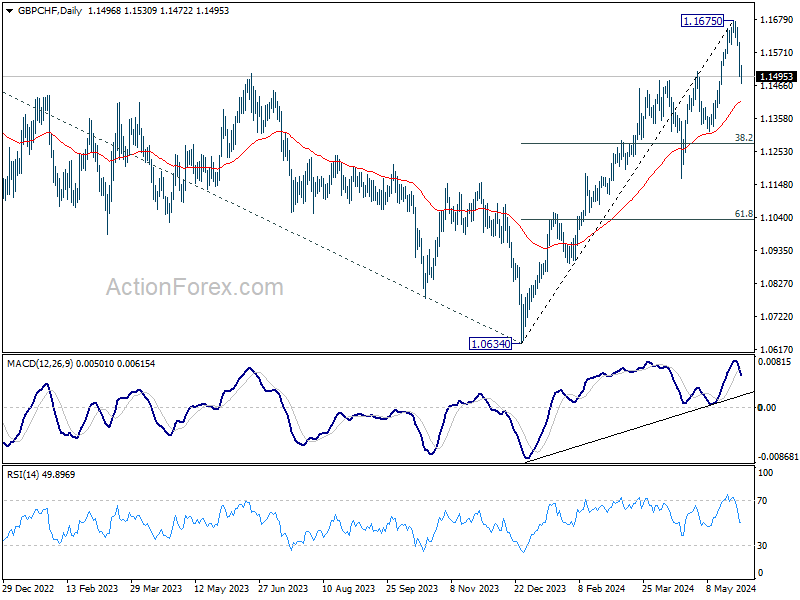

GBP/CHF has been as little stronger than EUR/CHF recently. But overall development in Franc still favors that a medium term is formed at 1.1675. Fall from there, as a correction to up trend from 1.0634, could extend to 55 D EMA (now at 1.1414) and possibly below. But strong support is expected from 38.2% retracement of 1.0634 to 1.1675 at 1.1277 to bring rebound.

Euro Struggles for Traction Despite Surging Inflation Figures

Euro had a temporary uplift following release of May’s inflation data, which indicated reacceleration in both headline and core figures within the Eurozone. Despite this, the currency’s momentum quickly dissipated, leaving Euro languishing at the lower end of the performance spectrum among major currencies.

ECB remains poised to lower interest rates by 25 basis points at its upcoming meeting this Thursday. This adjustment will bring deposit rate to 3.75% and main refinancing rate to 4.25%.

Initially, a significant portion of financial analysts, as polled in a recent Reuters survey, anticipated ECB would enact two additional rate cuts later this year, in September and December. However, the market’s expectations have shifted post-inflation data, now forecasting a total of slightly more than 50 bps in cuts for the year, suggesting only two rate reductions.

Market participants appear to be adopting a cautious stance, opting to withhold larger bets until ECB releases its new economic projections alongside the rate decision. This forthcoming information will likely play a critical role in shaping future market movements and monetary policy expectations.

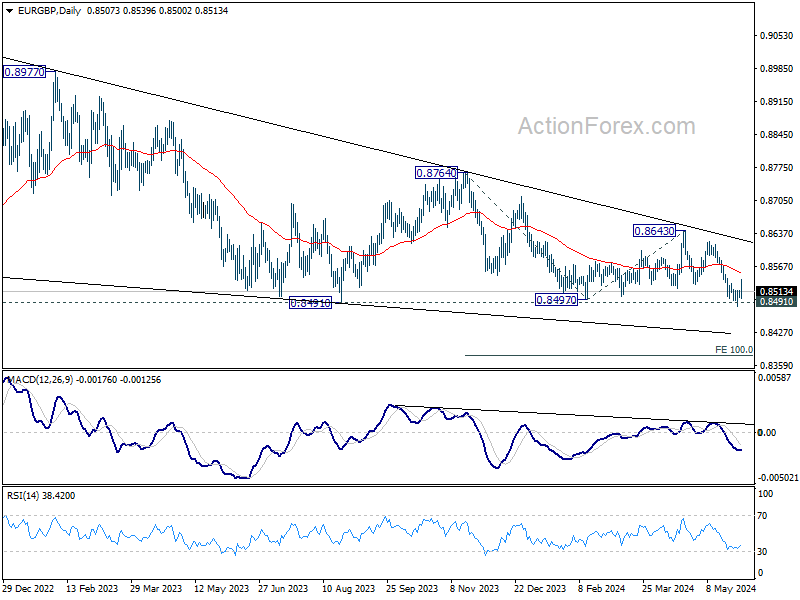

EUR/GBP recovered after breaching 0.8491 key support briefly, but upside is so far limited. Further decline will remain in favor as long as 55 D EMA (now at 0.8553) holds. Decisive break of 0.8491/7 will resume larger down trend to 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

Aussie Climbs Modestly Amid Uncertainty Over RBA’s Next Steps

Australian Dollar stood out as one of the stronger performers last week, buoyed by unexpected acceleration in headline inflation. Notably, RBA’s favored metric, trimmed mean inflation, which excludes volatile items such as petrol, also showed an uptick. However, its gains were tempered by a prevailing risk-off mood, particularly noticeable within the region.

In its recent meeting minutes, RBA disclosed that a rate hike was on the table in May, though it ultimately decided to maintain rates. Currently, Warren Hogan, Chief Economic Advisor at Judo Bank, stands alone in anticipating a rate hike in June, asserting it as the “only option” in light of the government’s inaction on price control. Additionally, there is a prevailing sentiment that RBA could be just “one bad inflation report” away from deciding to increase rates.

Contrarily, major banks continue to forecast a rate cut as the next move, with Westpac expecting a “forward-looking” RBA to initiate cuts in November. Market traders, on the other hand, have significantly dialed back their expectations for a rate cut, now foreseeing a possible easing only by December 2025—a delay from the previously anticipated cut in May next year.

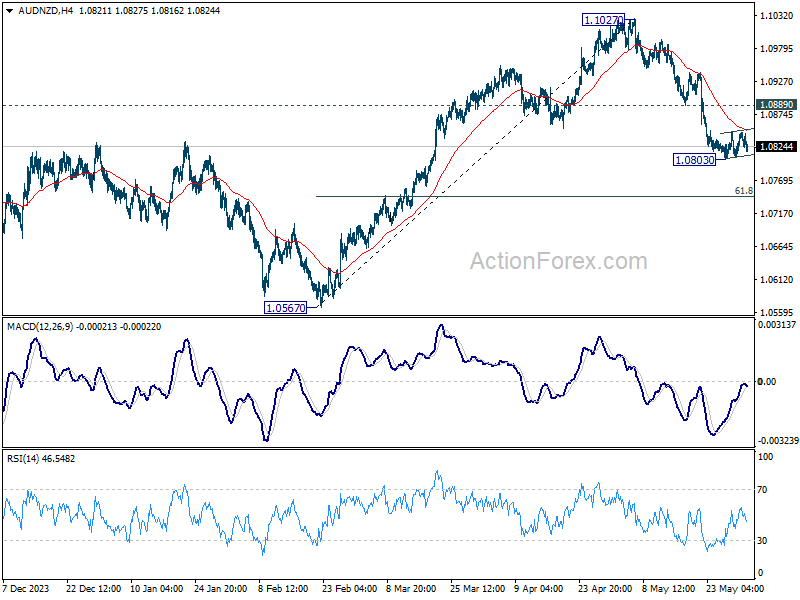

Even against Kiwi, Aussie’s recovery was lackluster. With 55 4H EMA intact, fall from 1.1027 is expected to resume sooner rather than later. Break of 1.0803 will target 61.8% retracement of 1.0567 to 1.1027 at 1.0743 and below.

Steady US Inflation Data Calms Markets

In the US, April’s PCE data, which indicated that both headline and core inflation rates remained unchanged from previous months, has provided a sense of relief to investors. This stability alleviates concerns about re-acceleration of inflation that might trigger further tightening by Fed. Currently, investors are accepting a balanced 50/50 probability that Fed will begin cutting interest rates in September. Any data supporting this move in the coming weeks could bolster risk sentiment weigh on the greenback.

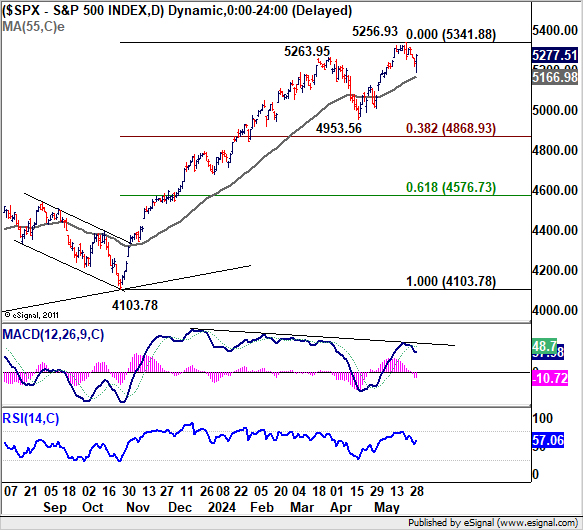

In the stock markets, while DOW’s correction was steep, S&P 500 and NASDAQ have been resilient. For now, S&P 500’s pull back from 5256.93 looks more likely a near term correction than not. Another rally through 5256.93 to resume the larger up trend is still in favor.

However, sustained break of 55 D EMA (now at 5166.98) will indicate that it’s already correcting the whole rise from 4103.78. Deeper fall would then be seen back towards 4953.56, and possibly below.

Dollar index struggled in tight range around flat 55 D EMA last week. On the downside, firm break of 104.08 will resume the fall from 106.51. More importantly, that would argue that whole rebound from 100.61 has completed with three waves up to 106.51. In this case, deeper fall would be seen to 102.35 and possibly below..

Nevertheless, strong bounce from current level will retain near term bullishness. Break of 105.74 resistance will argue that rise from 100.61 is ready to resume through 106.51 to 107.34 resistance.

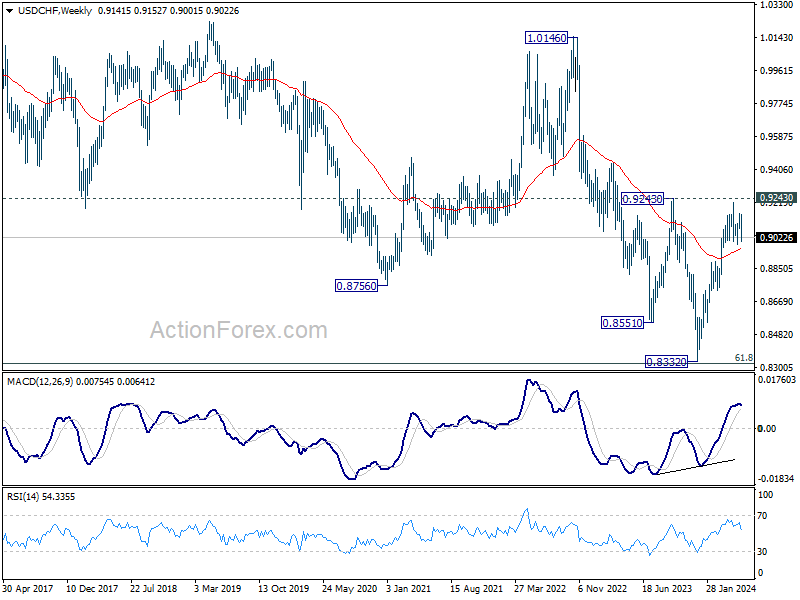

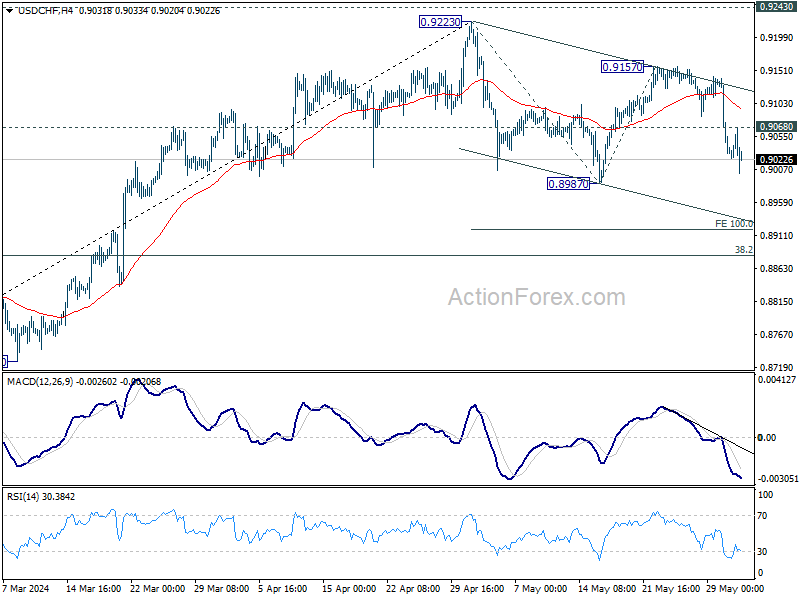

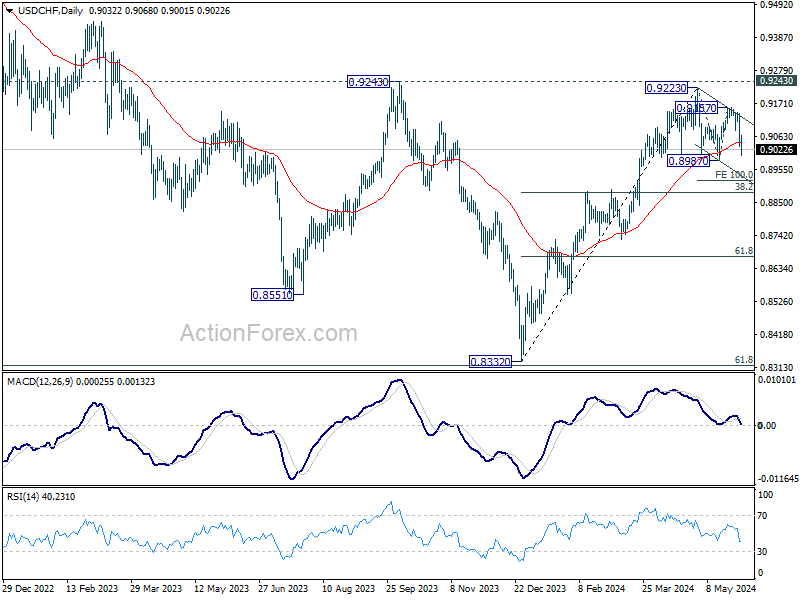

USD/CHF Weekly Outlook

USD/CHF’s steep decline last week suggests that rebound from 0.8987 has completed at 0.9157. Initial bias stays on the downside this week for 0.8987. Firm break there will resume the fall from 0.9223 to 100% projection of 0.9223 to 0.8987 from 0.9157 at 0.8921. On the upside, above 0.9065 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

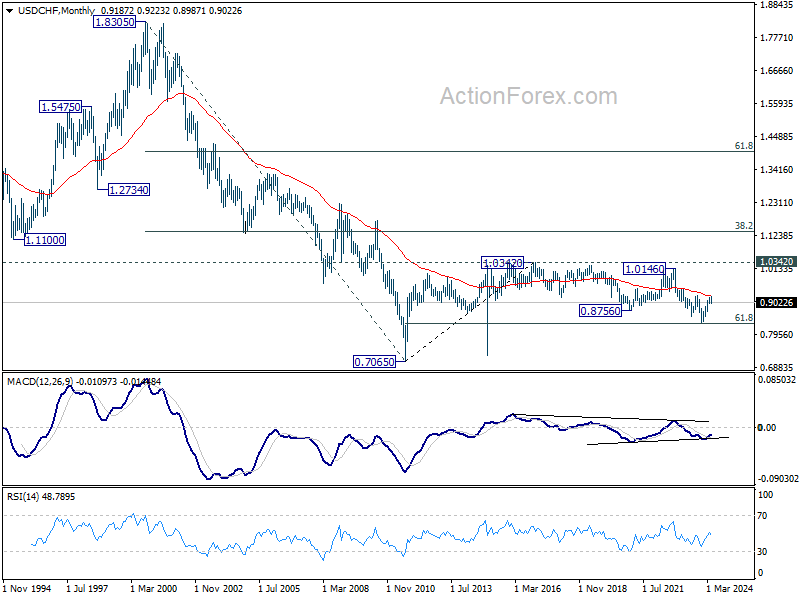

In the long term picture, price action from 0.7065 (2011 high) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Strong rebound from 61.8% retracement of 0.7065 to 1.0342 (2016 high) will start the third leg as a medium term rally. But there will be no sign of long term reversal until firm break of 38.2% retracement of 1.8305 to 0.7065 at 1.1359.