Quiet Forex Start Masks Anticipation of US CPI-Driven Volatility – Action Forex

The forex markets have started the week on a subdued note, typical of a Monday morning in Asia, particularly with Japan on holiday. Yen remains in a consolidation phase, holding steady after its recent gains and staying as the strongest currency this month so far. Swiss Franc is not far behind, ranking as the second. This picture reflects the persistent caution in the market. The preference for these safe-haven currencies underscores the vulnerability in risk sentiment.

However, this calm is unlikely to last. Market participants are gearing up for a surge in volatility later in the week, driven by US CPI data. Recent sharp selloff in stock markets has amplified calls for Fed to ease its monetary policy sooner rather than later. Some analysts are even speculating about the possibility of a more significant rate cut in September. Nonetheless, if CPI data surprises to the upside, it could put the Fed in a tough position, trapped between the need to control inflation and the risk of exacerbating recession fears. Such a scenario could heighten market anxiety, leading to further turbulence across financial markets.

Meanwhile, the British Pound is struggling, currently the weakest performer among the major currencies this month. Pound’s decline comes at a time when BoE’s MPC is deeply divided on the path forward. This week’s economic data releases will be crucial in providing guidance on whether the MPC will continue with interest rate cuts in the near future. Dollar is not faring much better, positioned as the second weakest currency this month, just ahead of Canadian Dollar. Meanwhile, Euro, Australian Dollar, and New Zealand Dollar are trading in the middle of the spectrum.

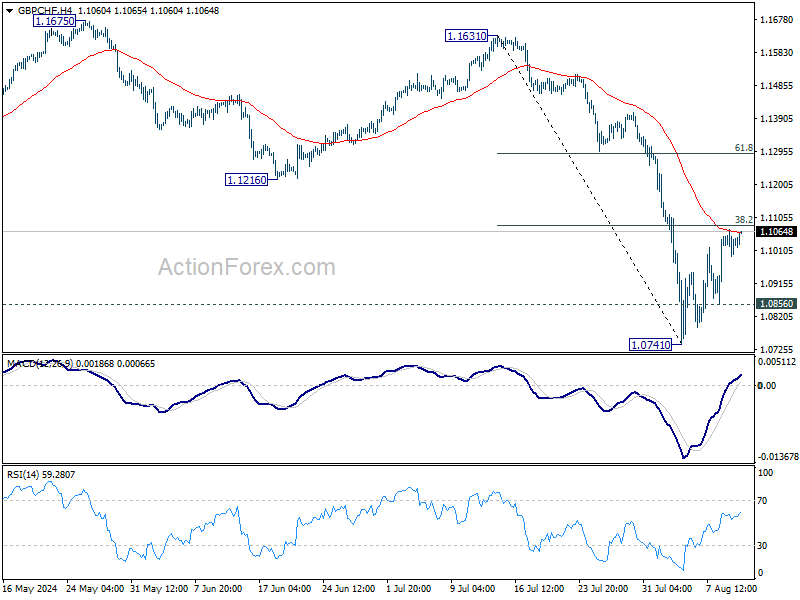

Technically, GBP/CHF’s recovery from 1.0741 is so far capped by 55 4H EMA as well as 38.2% retracement of 1.1631 to 1.0741 at 1.1108. Larger fall from 1.1675 is still expected to continue. Below 1.0856 minor support will argue that this decline is ready to resume through 1.0741 towards 1.0634 (2023 low). Nevertheless, firm break of 1.1108 will bring stronger rebound back to 1.1216 support turned resistance or above. The direction of this movement will likely become clearer as the week progresses, particularly with the release of key economic data.

In Asia, Japan is on holiday. Hong Kong HSI is up 0.18%. China Shanghai SSE is up 0.13%. Singapore Strait Times is down -0.82%.

Fed’s Bowman underlines priority on price stability

Fed Governor Michelle Bowman noted during a Saturday event that her “baseline” expectation is for inflation to decline further under the current policy stance. She added that if incoming data shows inflation moving sustainably toward the 2% target, it could become appropriate to “gradually lower the federal funds rate.” This would prevent monetary policy from becoming “overly restrictive” on economic activity and employment.

However, Bowman stressed that monetary policy is “not on a preset course,” with decisions to be guided by data. By the time of Fed’s September meeting, the committee will have additional economic data, including one employment and two inflation reports, as well as a broader view of financial conditions.

She acknowledged that while equity prices have been “volatile” recently, they remain “still higher than at the end of last year,” indicating resilience in financial markets.

Despite some progress, Bowman expressed concerns that inflation remains “somewhat elevated” with “some upside risks.” She emphasized the need to “pay close attention to the price-stability side of our mandate,” while also monitoring for any significant weakening in the labor market.

RBNZ to hold, US CPI in spotlight with UK data

RBNZ is at the forefront this week, expected to keep its Official Cash Rate steady at 5.50%. Despite recent speculations of an early rate cut at this meeting, the central bank seems poised to hold off on easing for now. Instead, the spotlight will be on the Monetary Policy Statement, where new economic projections could lay the groundwork for policy easing later in the year.

Currently, November is seen as the most likely month for RBNZ to initiate the policy loosening cycle, but there’s a possibility that the timeline be brought forward to October if economic conditions warrant. The economic projections would hopefully provide clarity on these questions.

In the US, focus is squarely on July CPI and retail sales data. With a September rate cut by Fed already fully priced into the market, the debate now centers on the magnitude of this cut. Fed officials appear well-prepared for a reduction in rates, but the question remains: will incoming data warrant a 25 basis point cut, or will Fed need to take more aggressive action with a 50 basis point reduction?

The key factors here are inflation and consumer spending. Should inflation slow significantly and consumption weaken, the case for a larger cut strengthens. Conversely, if the data merely meets expectations without major surprises, Fed may stick to a more modest adjustment. The prospect for a total of 75 basis points in cuts by the end of the year is on the table, though some analysts are even contemplating a full percentage point reduction if the economy shows further signs of distress.

Across the Atlantic, the UK is bracing for a flurry of important economic data, including GDP, employment figures, CPI, and retail sales. BoE recent decision to cut interest rates was a close call, with a narrow 5-4 vote. Notably, Chief Economist Huw Pill dissented, underscoring the division within the MPC.

A rebound in July CPI in the UK, coupled with slowdown in Q2 GDP growth, would present the MPC with a complex dilemma. On one hand, resurgence of inflation pressures might argue for a pause in further rate cuts, while on the other, slowing economic growth could push the MPC to continue its easing cycle. The coming data will be critical in determining the BoE’s next steps, as the central bank seeks to balance the conflicting signals from the economy.

In Asia Pacific, Japan’s Q2 GDP data is expected to reveal a strong rebound driven by consumption. However, BoJ faces limited room for continuing with rate hikes, especially if global financial markets remain unstable. In Australia, employment data will be under scrutiny, alongside key economic indicators from China, including industrial production, retail sales, and fixed asset investment.

Here are some highlights for the week:

- Monday: Canada building permits.

- Tuesday: Japan PPI; Australia Westpac consumer sentiment, NAB business confidence wage price index, UK employment; German ZEW economic sentiment; US PPI.

- Wed: RBNZ rate decision; UK CPI, PPI; Eurozone GDP revision, industrial production; US CPI.

- Thursday: Japan GDP; Australia employment; China industrial production, retail sales, fixed asset investment; UK GDP, production, trade balance; Swiss PPI; Canada wholesale sales; US retail sales, jobless claims, Philly Fed survey, Empire State manufacturing, import prices, industrial production, business inventories, NAHB housing index.

- Friday: Japan tertiary industry index; UK retail sales; Eurozone trade balance; Canada housing starts, manufacturing sales; US building permits and housing starts; U of Michigan consumer sentiment.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.49; (P) 160.44; (R1) 161.05; More…

Intraday bias in EUR/JPY stays neutral for the moment. While recovery from 154.40 might extending, outlook will remain bearish as long as 38.2% retracement of 175.41 to 154.40 at 162.42 holds. On the downside, below 157.71 minor support will bring retest of 154.40 first. Break there will resume the fall from 175.41 to 153.15 support next. However, sustained break of 162.42 will bring strong rise to 61.8% retracement at 167.38, even as a corrective move.

In the bigger picture, fall from 175.41 medium term top should be correcting the whole rise from 114.42 (2020 low). Deeper decline could be seen as long as 55 W EMA (now at 161.88) holds. But strong support should emerge between 153.15 and 38.2% retracement of 114.42 to 175.41 at 152.11 to bring rebound, at least on first attempt. Meanwhile, sustained trading above 55 W EMA will argue that the range of the medium term corrective pattern has already been set.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 12:30 | CAD | Building Permits M/M Jun | 5.60% | -12.20% |