Dollar Stays Pressured, NFP Revisions and FOMC Minutes Unlikely Change Its Course – Action Forex

Dollar remains under broad-based selling pressure, with markets likely to keep this trend until Fed Chair Jerome Powell delivers his speech at the Jackson Hole Symposium on Friday. While today’s events, including the non-farm payroll revision and the release of FOMC minutes, warrant some attention, they are unlikely to cause significant market shifts.

The US Bureau of Labor Statistics is set to release 2024 Preliminary Benchmark Revision to Establishment Survey Data, which includes adjustments to non-farm payroll numbers for the period between April 2023 and March 2024. Analysts at Goldman Sachs have suggested that the revision could result in a downward adjustment to labor growth by 600k to 1m jobs, equating to a monthly reduction of 50k to 85k jobs.

The implications of the downward revision to NFP data are complex. On one hand, it could indicate that the US job market has not been as robust as previously thought, which might be perceived negatively. However, as Fed Governor Michelle Bowman pointed out, this could also imply that the job market isn’t cooling as much as the recent rise in unemployment suggests.

Regarding FOMC minutes, it’s unlikely that they will provide clear guidance on the future path of monetary policy easing, given the current uncertainties. One key takeaway will likely be that Fed is increasingly balancing its dual mandate of price stability and full employment, with potential of tilting slightly more towards the latter. While the minutes may offer subtle hints that the committee is prepared for a rate cut in September, the market’s focus will be on what Fed plans to do after the initial reduction.

So far this week, Dollar has been the weakest performer among major currencies, followed by Canadian Dollar and British Pound. New Zealand Dollar is leading gains, followed by Yen and Swiss Franc, while Euro and Australian Dollar are positioned in the middle.

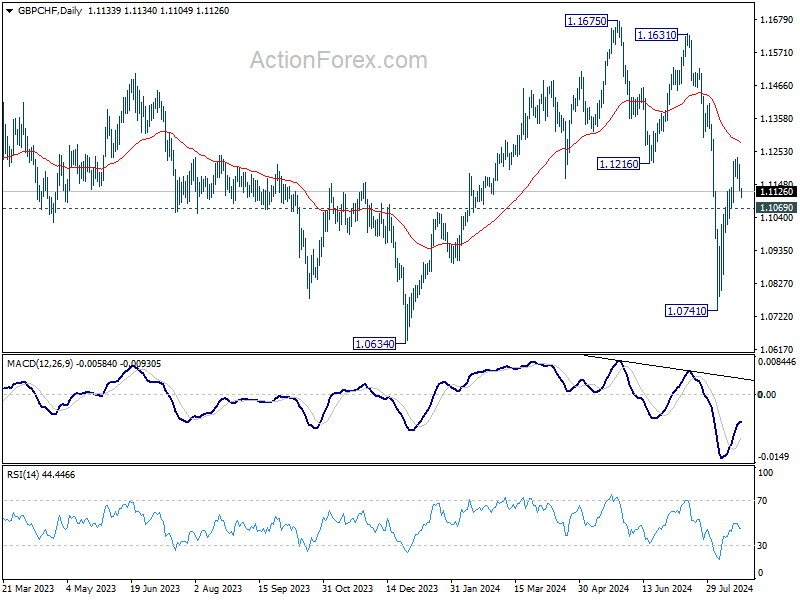

Technically, GBP/CHF’s rebound lost much momentum after hitting 1.1235 earlier in the week. For now, further rally will remain in favor as long as 1.1069 minor support holds. However, firm break of 1.1069 will indicate that the rebound from 1.0741 could have completed, after rejection by 1.1216 support turned resistance, and capped below 55 D EMA. That would keep the whole fall from 1.1675 alive, and set up for deeper decline back to 1.0741 low.

In Asia, at the time of writing, Nikkei is down -0.31%. Hong Kong HSI is down -0.91%. China Shanghai SSE is down -0.39%. Singapore Strait Times is down -0.35%. Japan 10-year JGB yield is down -0.0091 at 0.883. Overnight, DOW fell -0.15%. S&P 500 fell -0.20%. NASDAQ fell -0.33%. 10-year yield fell -0.0490 to 3.818.

Japan’s July exports value reaches record amid yen weakness

Japan’s exports surged 10.3% yoy in July, reaching JPY 9,619B—a record high for the month. The growth of export value was was largely driven by the weaker yen, which marked a -12.3% depreciation from a year ago. On volume basis, exports actually declined by -5.2% yoy.

Regionally, Japan’s exports to the US grew by 7.3%, a slight deceleration from the previous month. Exports to China remained steady with a 7.2% increase, while shipments to the EU saw a decline of -5.3%.

On the import side, Japan recorded a 16.6% yoy increase, bringing the total to JPY 10,241B—the largest ever for July. As a result, the trade balance showed a deficit of JPY -622 B.

In seasonally adjusted terms, exports rose 1.7% mom to JPY 9,137B, while imports increased by 0.9% mom to JPY 9,893B, leading to a seasonally adjusted trade deficit of JPY -755B.

Australia’s Westpac leading index points to modest growth, but sustainability in doubt

Australia’s six-month annualized growth rate in the Westpac–Melbourne Institute Leading Index inched up to +0.06%, signaling a slight improvement in economic momentum.

However, Westpac cautioned that this positive signal may not be sustained due to “sharp falls in commodity prices.” The detailed report highlights that the economy is facing “significant cross-currents,” with economic activity improving but expected to remain “below trend into early 2025.”

As RBA gears up for its next meeting on September 23–24, Westpac emphasized the importance of the upcoming June quarter national accounts, set to be released on September 4. These figures are expected to shed light on the strength of domestic demand and could ease some of the RBA’s concerns regarding productivity growth.

However, Westpac noted that there is little chance of a policy shift at the September meeting, as the next quarterly CPI update isn’t due until October 30.

Fed’s Bowman: Gradual rate cuts on the table if inflation continues to ease

Fed Governor Michelle Bowman, in a speech overnight, stated that her baseline outlook anticipates further declines in inflation under the current monetary policy. Should incoming data continue to confirm that inflation is moving steadily toward the 2% target, it may become appropriate to “gradually lower” the federal funds rate. This adjustment would prevent monetary policy from becoming “overly restrictive” on economic activity and employment.

However, Bowman urged to be “patient” and “avoid undermining” the continued progress on disinflation by “overreacting to any single data point”. She emphasized that monetary policy is “not on a preset course,” and decisions will depend on upcoming economic data. By the September meeting, Fed will review additional employment and inflation reports, as well as broader financial conditions, to assess their impact on the economic outlook.

Bowman also warned of “some upside risks to inflation,” citing concerns that supply conditions, now largely normalized, may not sufficiently counteract price pressures from geopolitical tensions, fiscal stimulus, and increased housing demand driven by immigration.

She also noted that the labor market might not be as strong as payroll data suggests, and the recent rise in unemployment could be “exaggerating the degree of cooling in labor markets.”

Looking ahead

UK will release public sector net borrowing in European session. Canada will release IPPI and RMPI later in the day. But main focus will be on FOMC minutes.

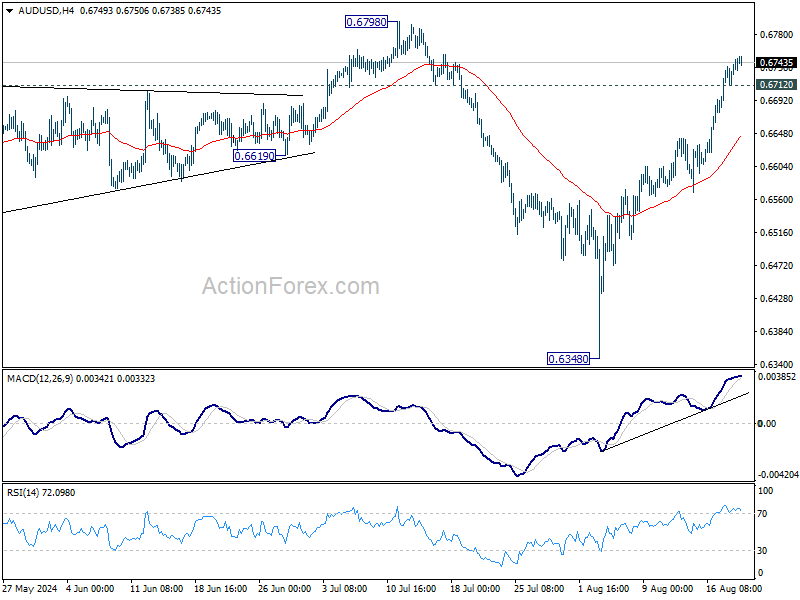

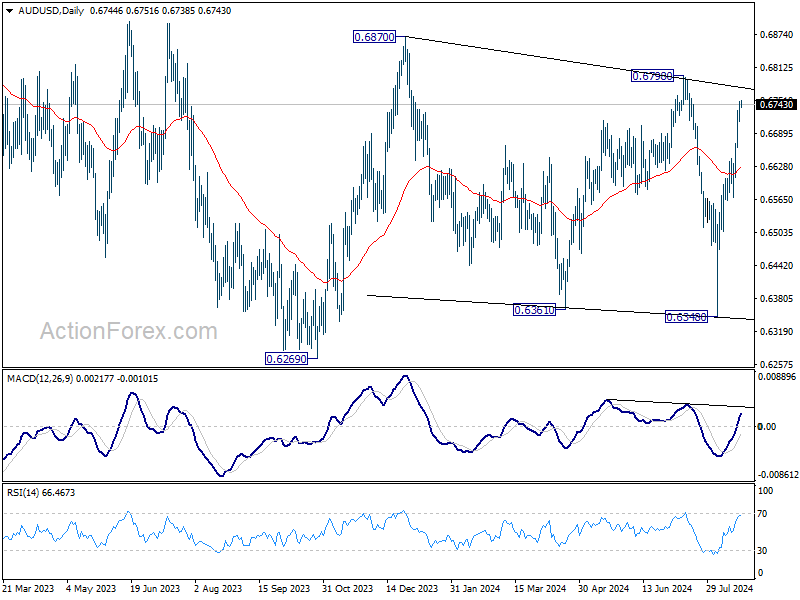

AUD/USD Daily Report

Daily Pivots: (S1) 0.6723; (P) 0.6737; (R1) 0.6761; More...

Intraday bias in AUD/USD remains on the upside as rise from 0.6348 is in progress for 0.6798 resistance. Firm break there will argue that larger rise from 0.6269 is ready to resume through 0.6870 resistance. On the downside, below 0.6712 minor support will turn intraday bias neutral and bring consolidations first. But further rally will remain in favor as long as 55 4H EMA (now at 0.6642) holds, in case of retreat.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern. Rise from 0.6340 is likely developing into another rising leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Jul | -0.76T | -0.76T | -0.82T | |

| 01:00 | AUD | Westpac Leading Index M/M Jul | 0.00% | 0.00% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jul | 0.5B | 13.6B | ||

| 12:30 | CAD | Industrial Product Price M/M Jul | -0.50% | 0.00% | ||

| 12:30 | CAD | Raw Material Price Index Jul | -0.90% | -1.40% | ||

| 14:30 | USD | Crude Oil Inventories | -2.0M | 1.4M | ||

| 18:00 | USD | FOMC Minutes |