Markets Shaken by US Recession Fears, BoC Rate Cut Awaited – Action Forex

Risk aversion swept across US markets overnight, with the selloff extending into Asian trading, driven by renewed fears of a recession. Weak US manufacturing data brought economic concerns back into focus, leading to a sharp 600-point drop in DOW and a more than 3.2% plunge in NASDAQ. The negative sentiment spread broadly across asset classes, with WTI crude oil tumbling over 4% and Bitcoin diving below the 56k mark.

Despite increasing expectations for a larger 50bps rate cut by Fed later this month, market sentiment remains fragile. The probability of a 50bps cut has risen to 41%, up from 30% just a day earlier, according to Fed fund futures. However, market participants remain cautious, as sentiment could deteriorate further with the release of key US economic data later in the week.

The services sector, which has been a crucial driver of the US economy while manufacturing has been in contraction for nearly two years, is showing signs of strain. ISM services data, set to be released on Thursday, has been fluctuating around the 50 mark since Q2, reflecting weakening conditions. A further decline would raise the possibility that the US economy is already on the brink of a recession. Additionally, Friday’s non-farm payroll report will be closely watched, as it could confirm or ease recession fears.

Technically, immediate focus is now on whether NASDAQ could bounce from 38.2% retracement of 15708.53 to 18017.68 at 17153.59. If not, decisive break there would push the index to 61.8% retracement at 16590.63. That would also argue that the consolidation from 18671.06 has already started the third leg, which could extend through 15708.53 low.

Overall in the currency markets, Yen has emerged as the strongest performer this week so far, followed by Swiss Franc and then Euro. On the other hand, New Zealand Dollar is the weakest, followed by Australian Dollar and Canadian Dollar, with the latter awaiting the outcome of today’s BoC rate cut decision. Dollar and Sterling are positioning in the middle.

In Asia, at the time of writing, Nikkei is down -3.31%. Hong Kong HSI is down -1.04%. China Shanghai SSE is down -0.40%. Singapore Strait Times is down -1.41%. Japan 10-year yield is down -0.0382 at 0.888. Overnight, DOW fell -1.51%. S&P 500 fell -2.12%. NASDAQ fell -3.26%. 10-year yield fell -0.067 to 3.844.

Japan’s PMI services finalized at 53.7, expansion continues

Japan’s services sector continued its expansion in August, with PMI Services index finalized at 53.7, unchanged from July’s figure. This marks the 23rd month of growth out of the past 24. PMI Composite, which includes both services and manufacturing, rose to 52.9 from 52.5 in July, reflecting the strongest overall growth since May 2023.

The services sector showed solid performance, while manufacturing output posted its most significant increase since May 2022. According to Usamah Bhatti, economist at S&P Global Market Intelligence, August saw ongoing growth in activity, new business, and employment in the service sector. However, the pace of employment growth and business optimism slowed to seven- and 19-month lows, respectively.

Australia’s GDP grows 0.2% qoq in Q2, per capita down for sixth quarter

Australia’s GDP grew by 0.2% qoq in Q2, aligning with market expectations. However, GDP per capita declined for the sixth consecutive quarter, falling by -0.4% qoq. For the 2023-24 financial year, the economy expanded by 1.5%.

Katherine Keenan, head of national accounts at the Australian Bureau of Statistics, noted, “The Australian economy grew for the eleventh consecutive quarter, although growth slowed over the 2023-24 financial year.”

Keenan also pointed out that excluding the pandemic period, annual financial year growth was the lowest since 1991-92, a year marked by the recovery from the 1991 recession.

China’s Caixin PMI services falls to 51.6, composite unchanged at 51.2

China’s Caixin PMI Services fell to 51.6 in August, down from 52.1 in July and below expectations of 52.2. While this marked the continuation of an expansion that began in January 2023, the rate of growth is among the slowest seen this year. PMI Composite remained steady at 51.2, indicating ten consecutive months of expansion.

According to Wang Zhe, Senior Economist at Caixin Insight Group, the services sector experienced a slight slowdown in supply and demand growth, in contrast to a recovery in manufacturing. One key concern was the services sector’s shrinking labor market, which pulled the composite employment indicator below the 50.0 mark, signaling a marginal contraction in employment.

On the pricing front, while input costs increased in both sectors, prices charged by manufacturers and service providers fell, adding pressure to business profitability. This combination of slower services growth and declining prices suggests increasing challenges for Chinese businesses as they contend with rising costs and shrinking profit margins.

BoC poised for third straight rate cut and stays dovish

BoC is widely expected to cut interest rates for the third consecutive meeting today, lowering the policy rate by 25bps to 4.25%. With inflation at a 40-month low of 2.5% and trending toward the 2% target, coupled with ongoing weakness in the labor market, further easing is anticipated. As a result, BoC is likely to maintain a dovish stance in its statement.

A recent Reuters poll shows that 70% of economists expect additional rate cuts in October and December, with the rate reaching 3.75% by year-end. Seven economists predict the rate will be 4.00%, while only one expects a drop to 3.50%.

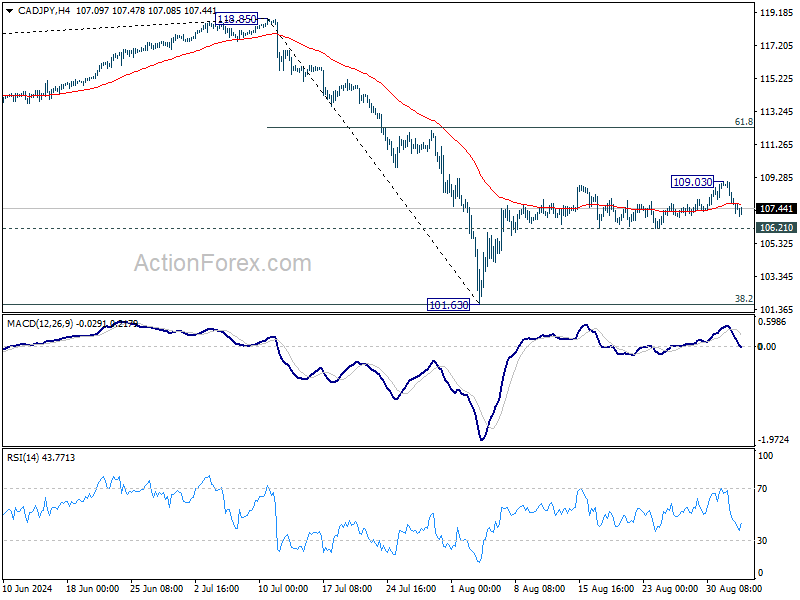

CAD/JPY saw a notable decline after briefly rising to 109.03 earlier this week. A couple of factors could be in force today. BoC’s decision and statement, overall risk sentiment, and the risks for further declines in oil prices could all impact the pair’s next move.

Technically, rebound from 101.63 is still in favor to continue as long as 106.21 support holds. Above 109.03 will target 61.8% retracement of 118.85 to 101.63 at 112.27. However, firm break of 106.21 will argue that the rebound has completed and bring deeper fall back to retest 101.63 low.

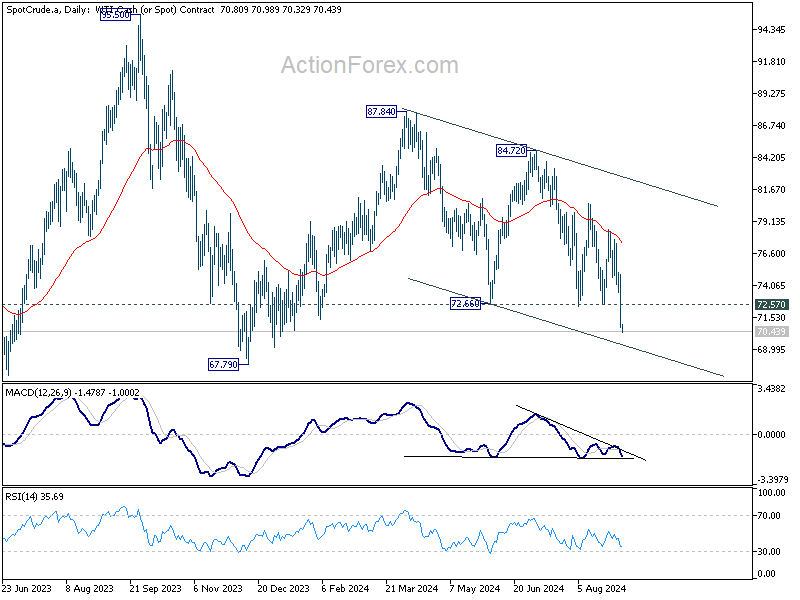

WTI crude oil tumbles, to test key 70 support level

WTI crude oil dropped sharply overnight, losing more than -4% and falling to its lowest level since last December. A combination of bearish factors contributed to this steep decline. The 70 psychological level is now critical for support, and if broken decisively, it could lead to an accelerated drop toward the 2023 low of around 63.

The decline was triggered by news that Libya’s rival governments may reach a deal to restore disrupted oil production. Oil prices were already facing downward pressure as OPEC+ prepares to increase output in the coming weeks. Further fueling concerns, weak US ISM manufacturing data, along with China’s disappointing Caixin PMI release earlier this week, raised demand worries for oil.

From a technical perspective, WTI remains bearish as long as the 72.57 resistance level holds. The falling trendline support at 69.47, near the 70 psychological level, is the key area to watch. A decisive break below this level could trigger further downside momentum.

Technically, near term outlook in WTI would stay bearish as long as 72.57 supported turn resistance holds. Falling trend line support (now at 69.47), which is close to 70 psychological level, is the key level the defend. Decisive break there could trigger downside acceleration.

Price actions from 95.50 (2023 high) are seen as the second leg of the pattern from 63.67 (2023 low). Fall from 87.84 is the third leg of the decline from 95.50. Any downside acceleration below the mentioned channel support could easily push WTI to 63.67/67.79 support before bottoming.

Looking ahead

Eurozone PMI services final and PPI will be released in European session, and UK PMI services final will also be published. Later in the day, US will release trade balance and Fed’s Beige Book report. BoC rate decision would be the main highlight and Canada will also release trade balance.

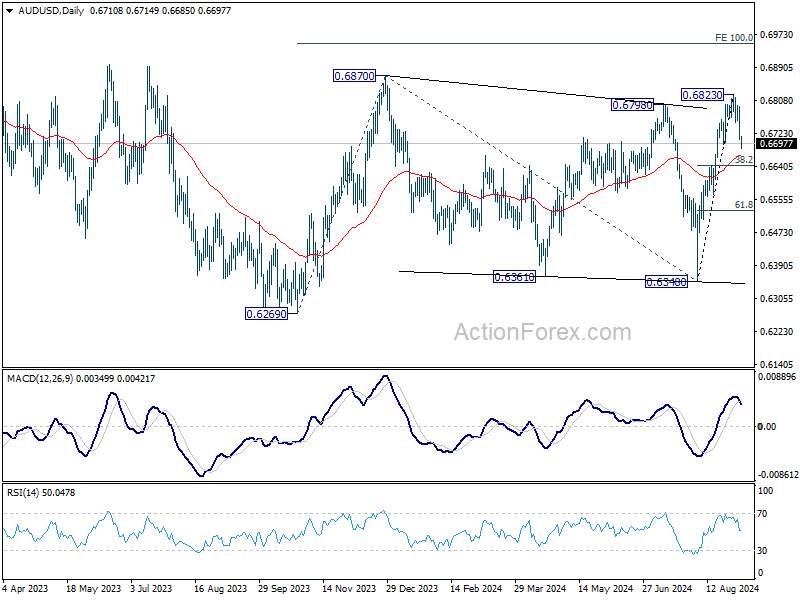

AUD/USD Daily Report

Daily Pivots: (S1) 0.6681; (P) 0.6738; (R1) 0.6769; More...

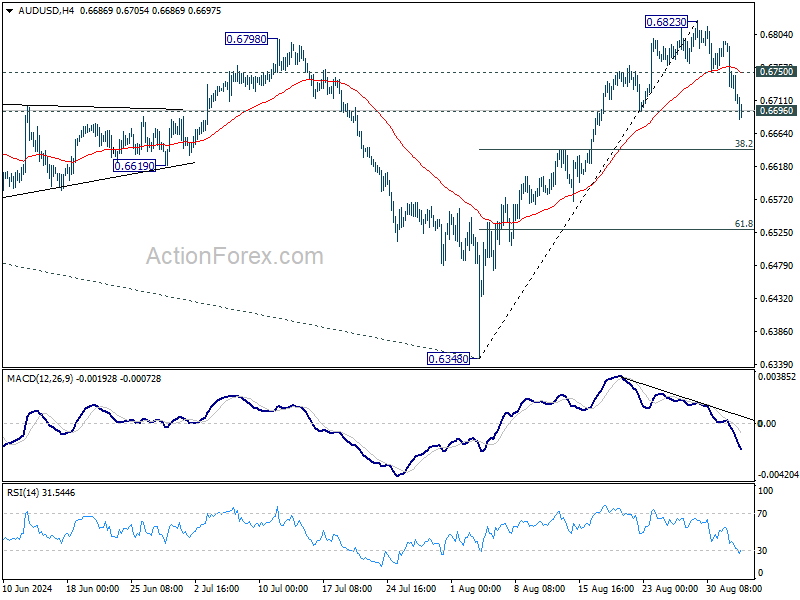

AUD/USD’s breach of 0.6696 support indicates that 0.6823 is already a short term top and deeper correction is underway. Intraday bias is now on the downside for 38.2% retracement of 0.6348 to 0.6823 at 0.6642. Break will target 61.8% retracement at 0.6529. On the upside, though, above 0.6750 support turned resistance will bring retest of 0.6823 instead.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | GDP Q/Q Q2 | 0.20% | 0.20% | 0.10% | |

| 01:45 | CNY | Caixin Services PMI Aug | 51.6 | 52.2 | 52.1 | |

| 07:50 | EUR | France Services PMI Aug F | 55 | 55 | ||

| 07:55 | EUR | Germany Services PMI Aug F | 51.4 | 51.4 | ||

| 08:00 | EUR | EurozoneServices PMI Aug F | 53.3 | 53.3 | ||

| 08:30 | GBP | Services PMI Aug F | 53.3 | 53.3 | ||

| 09:00 | EUR | Eurozone PPI M/M Jul | 0.30% | 0.50% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Jul | -2.50% | -3.20% | ||

| 12:30 | USD | Trade Balance (USD) Jul | -76.4B | -73.1B | ||

| 12:30 | CAD | Trade Balance (CAD) Jul | -0.3B | 0.6B | ||

| 13:45 | CAD | BoC Interest Rate Decision | 4.25% | 4.50% | ||

| 14:30 | CAD | BoC Press Conference | ||||

| 18:00 | USD | Fed’s Beige Book |