Markets Brace for NFP Impact as Yen Rally Gains Momentum – Action Forex

The financial markets are in a state of heightened anticipation as the much-awaited US non-farm payroll report is set to release today. This key data set will be critical in assessing whether the US economy is veering towards a recession, following the jump in the unemployment rate in July. For Fed, the NFP data will play a significant role in determining the size of the upcoming rate cut as the start of its policy easing cycle, which is expected at the FOMC meeting later this month. However, market reactions could be complex and volatile, as shifting dynamics between stocks, bond yields, and currencies may generate counteracting movements.

Dollar saw broad weakness overnight, but the selloff was tempered by ISM services PMI report, which indicated that the services sector remains in modest growth territory. As of now, Dollar and British Pound are positioned in the middle of the week’s performance chart. On the other hand, Japanese Yen is staying as the strongest performer, supported by declining US and European benchmark yields. Yen also extended its rally during today’s Asian trading session. Close behind are Swiss Franc and Euro. Meanwhile, Australian Dollar sits at the bottom of the performance ladder, followed by New Zealand Dollar and Canadian Dollar, signaling a cautious and risk-averse market atmosphere.

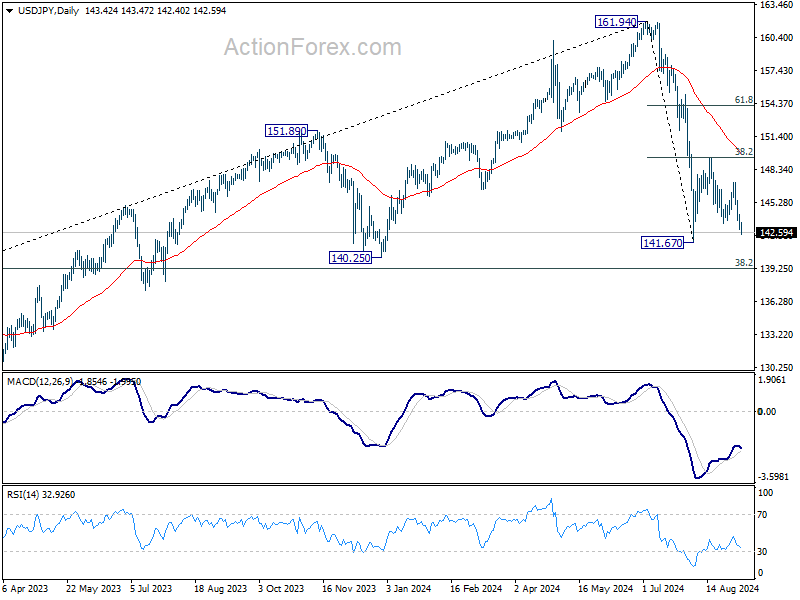

Technically, USD/JPY would be eyeing 141.67 support if current decline continues. Break there will resume whole decline from 161.94. But an important zone around 140 lies ahead with 140.25 support, as well as 38.2% retracement of 102.58 to 161.94 at 139.26. So, downside potential might be relatively limited. Yet, decisive break of 140 would risk deeper acceleration in the selloff.

In Asia, at the time of writing, Nikkei is down -0.07%. Hong Kong HSI is down -0.07%. China Shanghai SSE is down -0.44%. Singapore Strait Times is flat. Japan 10-year JGB yield is down -0.0173 at 0.858. Overnight, DOW fell -0.54%. S&P 500 fell -0.30%. NASDAQ rose 025%. 10-year yield fell -0.037 to 3.731.

Fed’s Goolsbee signals multiple rate cuts as labor market weakens

In an interview with MarketWatch, Chicago Fed President Austan Goolsbee indicated that the current economic data justifies multiple interest rate cuts, with the process beginning soon.

Goolsbee pointed out that inflation is coming down “very significantly,” while the unemployment rate is “rising faster,” suggesting a cooling labor market.

He expressed concern that the persistent weakness in the job market could “turn into something worse” if the trend continues.

Given the balance of more favorable inflation data and deteriorating unemployment figures, Goolsbee suggested that the path forward is “not just rate cuts soon,” hinting at a sustained easing cycle by Fed.

Japan’s household spending rises only 0.1% in Jul, lagging expectations despite wage growth

Japan’s household spending edged up by 0.1% yoy in July, falling well short of the expected 1.2% yoy increase. While this marked the first annual rise in three months, the modest growth suggests that households are still holding back on spending due to inflationary pressures.

The increase was driven by a 17.3% yoy surge in housing outlays, with more people undertaking home renovations such as installing new kitchens and bathtubs, according to the Ministry of Internal Affairs and Communications. Entertainment spending also grew by 5.6% yoy, supported by purchases of televisions for the Paris Olympics. Expenditures on domestic and overseas package tours saw significant jumps of 47.0% yoy and 62.6% yoy, respectively.

Despite the tepid spending growth, the average monthly income of salaried households with at least two people rose by 5.5% yoy in real terms, marking the third consecutive monthly increase after 3.1% yoy and 3.0% yoy gains in June and May.

A ministry official noted that “spending has not increased as much as wages grew,” suggesting that some households might be saving part of their higher incomes. The ministry plans to continue monitoring how rising wages impact consumption going forward.

US NFP in focus as Fed’s rate cut decision hangs in the balance

Today’s US non-farm payroll report is crucial for all market participants, as it could determine the size of Fed’s expected rate cut this month. Currently, fed fund futures are pricing in 43/57% chance of a 25/50 bps reduction. Market reaction to NFP will also likely set the trading tone for the remainder of the quarter.

Economists expect job growth of 163k in August, with the unemployment rate forecasted to tick down from 4.3% to 4.2%. Average hourly earnings are projected to increase by 0.3% mom, indicating solid wage growth.

Recent economic data offers a mixed outlook. ISM Manufacturing Employment rose to 46.0 from 43.4, but the ISM Services Employment fell to 50.2 from 51.1. Meanwhile, ADP Employment report showed a disappointing 99k new jobs, down from July’s 111k. Initial unemployment claims averaged 230k over four weeks, down from last month’s 240k.

A key data point to watch will be the unemployment rate. Last month’s unexpected rise to 4.3% triggered the “Sahm Rule,” a reliable recession indicator. If the unemployment rate doesn’t fall as expected, or worse, increases further, it could signal deeper labor market troubles. This scenario might prompt Fed to take pre-emptive action with a 50 bps rate cut at the upcoming FOMC meeting. Yet, markets’ bearish reaction could overwhelm Fed cut optimism.

The stock markets’ reaction to NFP today is worth high attention. S&P 500 top at 5651.37, just ahead of 5669.67 historical high. On the downside, decisive break of 55 D EMA (now at 5475.02) will argue that rebound from 5119.26 has completed. Corrective pattern from 5669.67 should have then started the third leg. In this case, deeper fall would be seen to wards 5119.26 support again.

But of course, strong bounce from 55 D EMA would set the stage for breaking through 5669.67 to resume the long term up trend, sooner rather than later.

Elsewhere

Germany industrial production and trade balance, France industrial production and trade balance; Swiss foreign currency reserves, and Eurozone GDP revision will be released in European session. Later in the day, Canada will also publish job data, along with US NFP.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1048; (P) 1.1071; (R1) 1.1107; More….

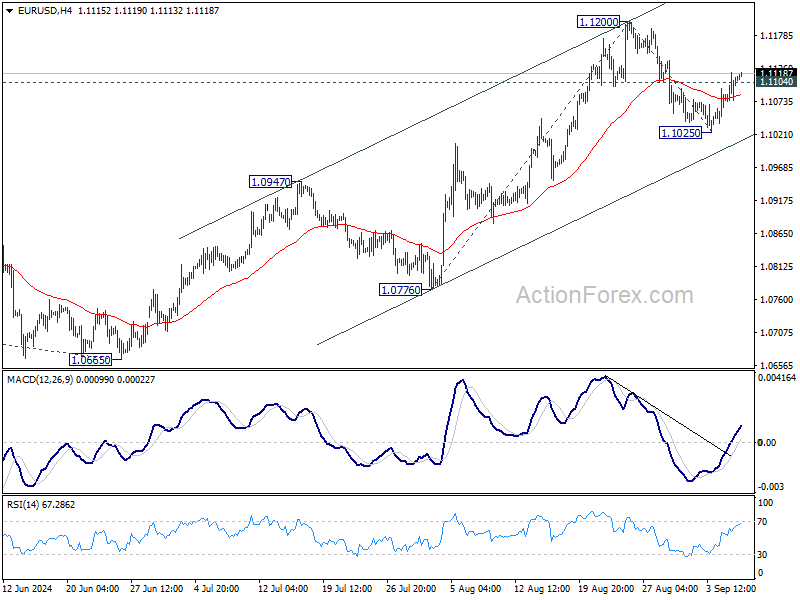

EUR/USD’s break of 1.1104 minor resistance suggests that pullback from 1.1200 has completed at 1.1025 already. Intraday bias is back on the upside for retesting 1.1200 first. Firm break there will resume larger rally and target 61.8% projection of 1.0776 to 1.1200 from 1.1025 at 1.1287. However, break of 1.1025 support will resume the fall from 1.1200 instead.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 has completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Overall Household Spending Y/Y Jul | 0.10% | 1.20% | -1.40% | |

| 05:00 | JPY | Leading Economic Index Jul P | 109.5 | 109.4 | 109 | |

| 06:00 | EUR | Germany Industrial Production sM/M Jul | -0.20% | 1.40% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Jul | 21.2B | 20.4B | ||

| 06:45 | EUR | France Trade Balance (EUR) Jul | -5.7B | -6.1B | ||

| 06:45 | EUR | France Industrial Output M/M Jul | -0.20% | 0.80% | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Aug | 704B | |||

| 09:00 | EUR | Eurozone GDP Q/Q Q2 | 0.30% | 0.30% | ||

| 12:30 | USD | Nonfarm Payrolls Aug | 163K | 114K | ||

| 12:30 | USD | Unemployment Rate Aug | 4.20% | 4.30% | ||

| 12:30 | USD | Average Hourly Earnings M/M Aug | 0.30% | 0.20% | ||

| 12:30 | CAD | Net Change in Employment Aug | 25.0K | -2.8K | ||

| 12:30 | CAD | Unemployment Rate Aug | 6.50% | 6.40% | ||

| 14:00 | CAD | Ivey PMI Aug | 55.3 | 57.6 |