Risk-On Rally Continues, Yen Remains Soft Following BoJ Hold – Action Forex

Global markets continues to a wave of risk-on sentiment today, with Japan’s Nikkei leading the charge in Asia. The index maintained its gains after BoJ decided to keep interest rates unchanged, a move that was widely anticipated.

This positive momentum stems from the strong performance of US equities overnight, as DOW and S&P 500 closed at record highs, in somewhat delayed reaction to Fed’s jumbo 50bps rate cut earlier in the week.

Meanwhile, China’s decision to hold its benchmark lending rates steady—though a disappointment for some expecting a cut—has had little effect on the overall bullish sentiment.

In the currency markets, Yen is currently the worst performer this week, followed by Dollar and Loonie. On the other hand, Aussie is the top gainer, followed closely by Kiwi and Sterling. Euro and Swiss Franc are positioning in the middle.

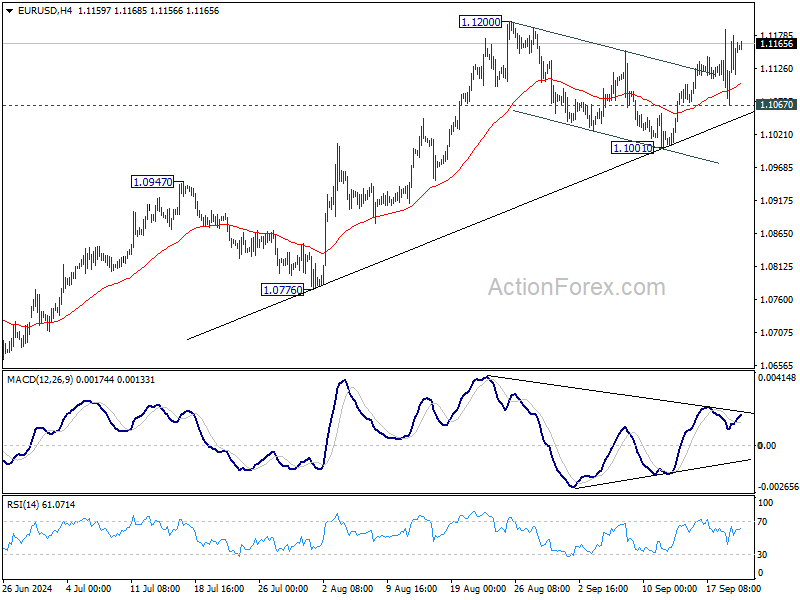

Technically, it’s important to highlight that key Dollar pairs like EUR/USD and USD/CHF are still trading within established near term ranges, suggesting that the recent market moves are more about risk appetite pushing up commodity currencies rather than a broad Dollar selloff in reaction to Fed’s actions.

To confirm sustained bearish shift in Dollar, EUR/USD would need to decisively break above the 1.1200 resistance, ideally accompanied by extended record run in Gold through 2600 mark.

In Asia, at the time of writing, Nikkei is up 2.10%. Hong Kong HSI is up 1.11%. China Shanghai SSE is down -0.19%. Singapore Strait Times is down -0.38%. Japan 10-year JGB yield is up 0.0035 at 0.857. Overnight, DOW rose 1.26%. S&P 500 rose 1.70%. NASDAQ rose 2.51%. 10-year yield rose 0.055 to 3.740.

BoJ stands pat at 0.25%, sees gradual inflation rise and economic growth

BoJ left its uncollateralized overnight call rate unchanged at around 0.25% during today’s meeting, as widely anticipated and decided by unanimously.

In the accompanying statement, BoJ maintained a positive outlook for the Japanese economy, projecting continued growth at a rate above its potential. The central bank expects “overseas economies will continue to grow moderately,” further supporting Japan’s economic expansion. Domestically, the “virtuous cycle from income to spending” will gradually intensify, aided by accommodating financial conditions.

On the inflation front, core CPI is forecast to rise through fiscal 2025. BoJ also noted that underlying inflation will “increase gradually” as output gap narrows and medium- to long-term inflation expectations firm up.

However, the central bank also outlined several risks to its outlook, including global economic developments, commodity prices, and the pace at which firms adjust wage and price setting.

Japan’s CPI core rises to 2.8% in Aug, core-core up to 2.0%

Japan’s core CPI, excluding fresh food, rose to 2.8% yoy in August, matching expectations and marking the fourth consecutive month of acceleration. This increase is up from 2.7% yoy in July and continues the upward trend from 2.2% yoy in April, keeping inflation above BoJ’s 2% target since April 2022.

Core-core CPI, which strips out both fresh food and energy, also rose from 1.9% yoy to 2.0% yoy, highlighting broader inflationary pressures in Japan. Headline CPI, which includes all categories, increased from 2.8% yoy to 3.0% yoy.

Energy prices surged 12.0% yoy, while food prices increased by 2.9% yoy, and household durable goods saw a significant rise of 7.7% yoy. These numbers indicate persistent inflationary pressures across a wide range of goods and services.

UK Gfk consumer confidence plummets to -20 ahead of expected painful budget

UK GfK Consumer Confidence dropped sharply in September, falling from -13 to -20, marking the biggest decline since April 2022. The seven-point drop reflects growing concerns about the economic outlook and personal finances, with households bracing for a difficult budget next month.

Key forward-looking indicators worsened significantly. Expectations for the general economy over the next 12 months dropped by -12 points to -27, while personal finance expectations fell by -9 points to -3. The major purchase index, which gauges consumers’ willingness to buy big-ticket items, also dropped -10 points to -23.

GfK noted, “Despite stable inflation and the prospect of further rate cuts, this is not encouraging news for the UK’s new government.” Neil Bellamy, Consumer Insights Director at GfK, linked the drop to concerns over Prime Minister Keir Starmer’s warnings of a “painful” budget. Bellamy said, “Consumers are nervously awaiting the Budget decisions on Oct. 30 after the withdrawal of winter fuel payments and warnings of further difficult measures.”

Looking ahead

Germany PPI and UK retail sales will be released in European session. Canada retial sales IPPI and RMPI will be released later in the day.

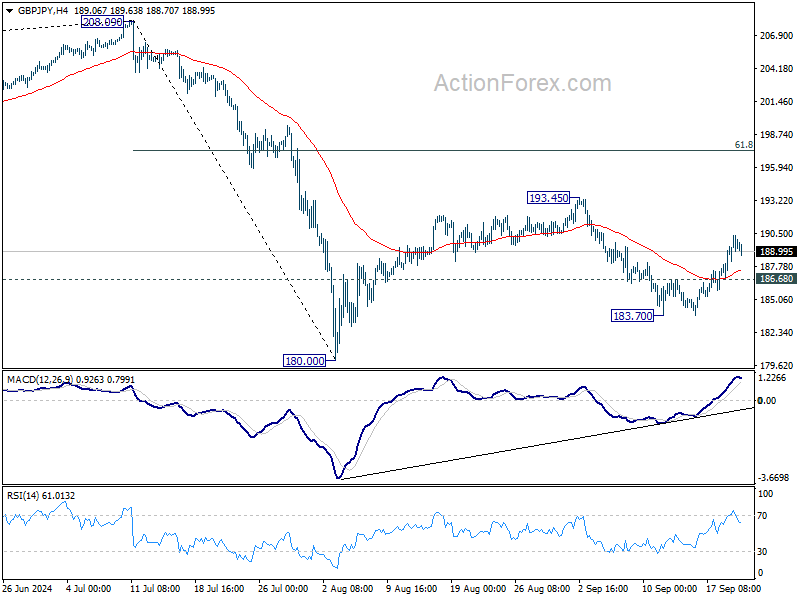

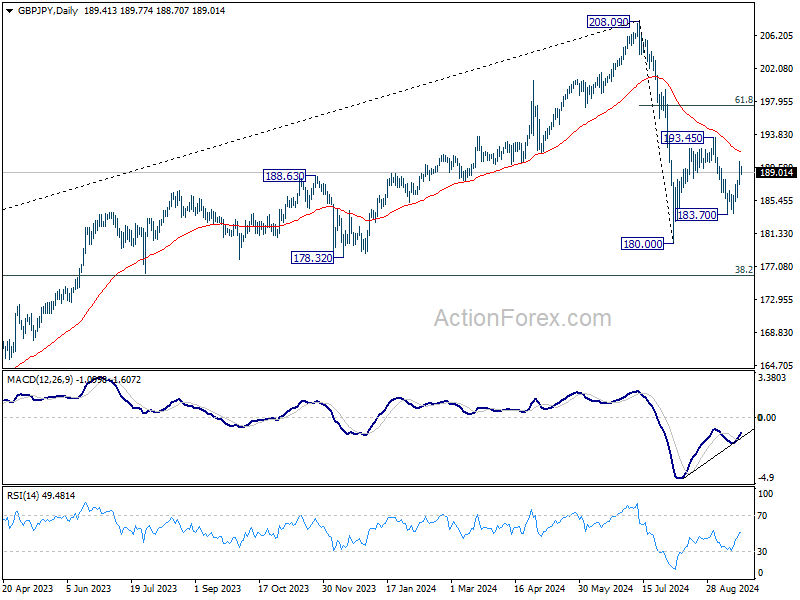

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.82; (P) 189.11; (R1) 190.77; More…

Intraday bias in GBP/JPY remains on the upside for the moment. Rise from 183.70 is seen as the third leg of the corrective pattern from 180.00. Further rally would be seen to 193.45 and possibly further to 61.8% retracement of 208.09 to 180.00 at 197.35. Nevertheless, break of 186.68 minor support will turn bias back to the downside for 183.70 instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence Sep | -20 | -13 | -13 | |

| 23:30 | JPY | CPI Y/Y Aug | 3.00% | 2.80% | ||

| 23:30 | JPY | CPI Core Y/Y Aug | 2.80% | 2.80% | 2.70% | |

| 23:30 | JPY | CPI Core-Core Y/Y Aug | 2.00% | 1.90% | ||

| 01:00 | CNY | 1-Y Loan Prime Rate | 3.35% | 3.35% | 3.35% | |

| 01:00 | CNY | 5-Y Loan Prime Rate | 3.85% | 3.85% | 3.85% | |

| 02:52 | JPY | BoJ Interest Rate Decision | 0.25% | 0.25% | 0.25% | |

| 06:00 | EUR | GermanyPPI M/M Aug | 0.00% | 0.20% | ||

| 06:00 | EUR | GermanyPPI Y/Y Aug | -1.00% | -0.80% | ||

| 06:00 | GBP | Retail Sales M/M Aug | 0.30% | 0.50% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Aug | 12.3B | 2.2B | ||

| 12:30 | CAD | Retail Sales M/M Jul | 0.50% | -0.30% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Jul | 0.20% | 0.30% | ||

| 12:30 | CAD | Industrial Product Price M/M Aug | -0.30% | 0.00% | ||

| 12:30 | CAD | Raw Material Price Index Aug | -2.00% | 0.70% | ||

| 14:00 | EUR | Eurozone Consumer Confidence Sep P | -13 | -13 |