Canada inflation set to drop further in September, giving BoC reasons for another cut

- The Canadian Consumer Price Index is expected to rise 1.8% YoY in September.

- The Bank of Canada has reduced its policy rate by 75 bps so far this year.

- The Canadian Dollar has been losing considerable ground in October.

Statistics Canada is set to release its latest inflation data tracked by the Consumer Price Index (CPI) for the month of September on Tuesday. Forecasts suggest that the headline CPI could have risen 1.8% year-over-year (YoY) last month.

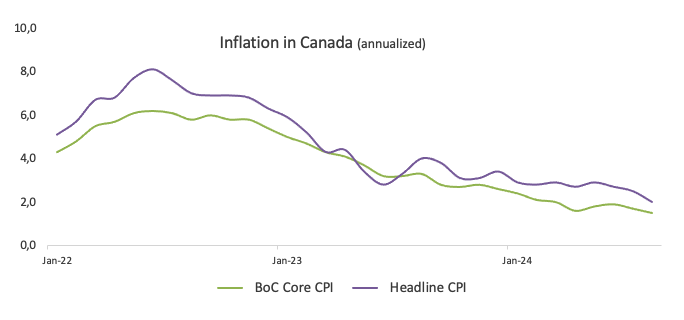

Alongside the headline data, the Bank of Canada (BoC) will release its core CPI, which excludes more volatile components such as food and energy. In August, the core CPI showed a 0.1% monthly decrease and a 1.5% rise from a year earlier. Meanwhile, the headline CPI climbed by 2.0% over the last twelve months — the lowest level since February 2021 — and dropped by 0.2% compared to the previous month.

These inflation figures are being closely monitored for their potential impact on the Canadian Dollar (CAD), especially in light of the BoC’s current easing cycle. It is worth recalling that the BoC has reduced its policy rate by 25 basis points at its June, July, and September meetings so far this year, taking the reference interest rate to 4.25%.

In the FX world, the Canadian Dollar has depreciated in the last nine consecutive days, sending USD/CAD to the 1.3800 zone for the first time since early August.

What can we expect from Canada’s inflation rate?

Analysts appear divided regarding the path of price pressures in Canada in September, though they agree that domestic headline prices will fall below the Bank of Canada’s target for the time being. Banning an outsized surprise, the underlying disinflationary trend is likely to prompt the BoC to maintain its course regarding the easing cycle that started in June.

After the BoC’s rate cut on September 4, Governor Tiff Macklem stated that a 25 bps reduction was appropriate, although he added that BoC officials discussed different scenarios, including slowing the pace of rate reductions and even a 50 basis point cut.

Regarding inflation, Macklem suggested that further rate cuts are likely, citing the Bank of Canada’s progress in reducing inflation towards its 2% target. In an interview in Toronto on September 24, Macklem emphasized the importance of maintaining inflation near the midpoint of the 1%–3% control range, stating, “We need to stick the landing.” He also highlighted the need for ongoing moderation in core inflation, which, he noted, remains slightly above 2%.

In light of the upcoming release, analysts at TD Securities noted, “We look for CPI to dip to 1.9% on a large drag from gasoline, offset by a stabilization in core goods and strength in travel components. Our forecast would see Q3 CPI undershoot BoC projections from July, but with softer oil prices helping to drive that move and a modest pickup for the BoC’s core measures in Sept, we do not believe this would justify a move to 50bp cuts.”

When is the Canada CPI data due, and how could it affect USD/CAD?

Canada will release its September CPI data on Tuesday at 12:30 GMT, and the Canadian Dollar’s response will hinge only on any significant surprise in the figures. Absent a major deviation from expectations, the data is unlikely to influence the Bank of Canada’s rate outlook.

USD/CAD has kicked off the month with a marked upward bias, reaching two-month highs around 1.3800 on Monday. The monthly advance has so far been on the back of a strong rebound in the US Dollar (USD), which has been keeping the broad risk-linked currencies on the back foot.

Pablo Piovano, Senior Analyst at FXStreet, points out that the continuation of the recovery could well see USD/CAD challenging its 2024 top of 1.3946 (August 5), just ahead of the 1.4000 milestone, an area last visited in May 2020.

“In the opposite direction, there are provisional contention levels at the 100-day and 55-day SMAs of 1.3655 and 1.3618, respectively, prior to the more relevant 200-day SMA at 1.3612. A break below this level could trigger further weakness, potentially targeting the next support at the September bottom of 1.3418 (September 25), ahead of the weekly low of 1.3358 (January 31)”, Pablo adds.

Economic Indicator

Consumer Price Index (MoM)

The Consumer Price Index (CPI), released by Statistics Canada on a monthly basis, represents changes in prices for Canadian consumers by comparing the cost of a fixed basket of goods and services. The MoM figure compares the prices of goods in the reference month to the previous month. Generally, a high reading is seen as bullish for the Canadian Dollar (CAD), while a low reading is seen as bearish.

Next release: Tue Oct 15, 2024 12:30

Frequency: Monthly

Consensus: –

Previous: -0.2%

Source: Statistics Canada

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.