Yen Falls on Political Turmoil as Dollar Strengthens Ahead of Key Economic Data – Action Forex

Yen suffered broad-based selloff during an otherwise quiet Asian session, following the weekend’s indecisive snap election that left Japan without a clear governing party. In contrast, Dollar emerged as the main beneficiary despite its own political uncertain, building on its recent upward momentum and gained across the board.. Canadian Dollar and Euro also showed firmness. Conversely, Swiss Franc clearly lagged behind, while Australian and New Zealand Dollars displayed relative weakness.

With the economic calendar empty today, major shifts in market trends are unlikely. However, the upcoming US presidential elections remain a source of volatility, as any unexpected developments could sway investor sentiment. Traders are also gearing up for a week filled with high-impact economic releases, including US GDP, PCE, ISM and NFP, inflation data from Eurozone, Australia and Swiss.

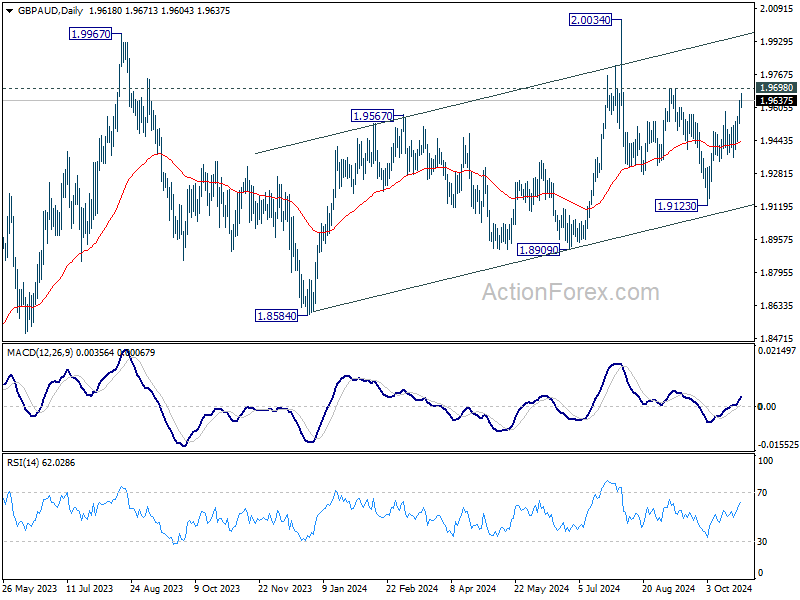

Technically, GBP/AUD’s extended rebound suggests that correction from 2.0034 has completed with three waves down to 1.9123. Firm break of 1.9698 resistance will argue that larger up trend is ready to resume through 2.0034. The next move could hinge of Australia quarterly CPI featured this week.

In Asia, Nikkei rose 1.85%. Hong Kong HSI is up 0.07%. China Shanghai SSE is up 0.24%. Singapore Strait Times is down -0.01%. Japan 10-year JGB yield rose 0.0187 to 0.971.

Yen depreciates sharply following inconclusive Japanese election

Yen fell significantly after this weekend’s snap election resulted in a fragmented parliament, leaving no single party with a clear mandate to govern. This political uncertainty introduces the prospect of days or even weeks of negotiations as parties attempt to form a coalition, raising concerns among traders about potential change in leadership and policy direction. Despite the political instability, Nikkei rebounded notably, primarily driven by the weaker yen rather than optimism about the electoral outcome.

Election results showed that Prime Minister Ishiba’s Liberal Democratic Party and its coalition partner Komeito secured only 215 seats in the lower house of parliament, a substantial decline from their previous 279 seats. The opposition Constitutional Democratic Party of Japan increased its seats to 148 from 98 but still fell short of the 233 required for a majority. Under Japan’s constitution, political parties now have 30 days to negotiate and form a governing coalition. The lack of a decisive outcome casts doubt on Ishiba’s tenure as premier, especially considering he assumed office less than a month ago.

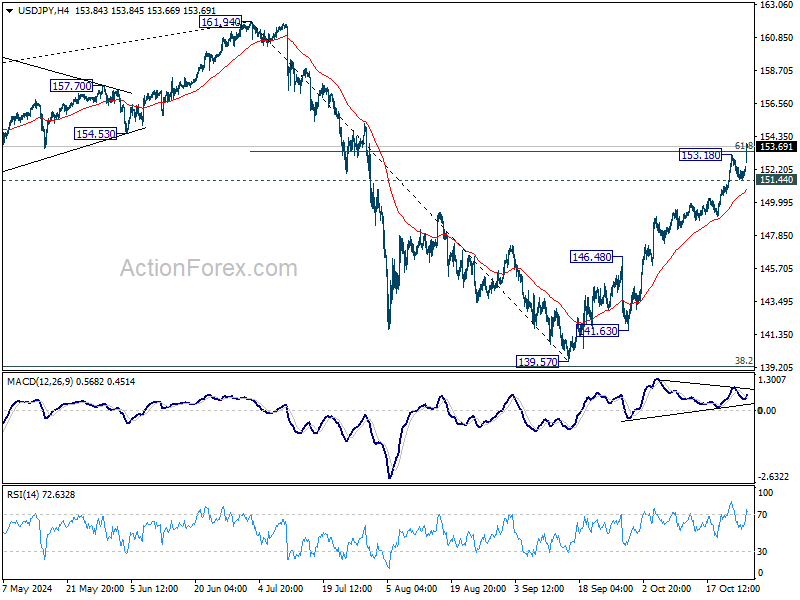

USD/JPY’s rise from 139.57 resumed after brief consolidations by breaking through 153.18 temporary low. Further rally is expected as long as 151.44 support holds. The question is whether USD/JPY could sustain above 61.8% retracement of 161.94 to 139.57 at 153.39. If it can, the next target wil be a retest on 161.94 high.

ECB’s Knot cautions against overly enthusiastic rate cut expectations

Speaking on Saturday, Dutch ECB Governing Council member Klass Knot acknowledged the market’s heightened expectations for ECB rate cuts, noting that this shift occurred after disappointing PMIs and consumption data.

Knot described these expectations as having increased “quite dramatically” but cautioned that the market may have been “a little bit over-enthusiastic.” He highlighted that “We will only know once we do our own calculations again in December.”

Knot outlined two contrasting scenarios regarding the ECB’s rate path. On one hand, if incoming data reveal a rapid pace of disinflation or signal a notable shortfall in economic recovery, ECB could accelerate policy easing. On the other, if inflation risks shift upwards or data show resilience in growth and inflation, a more gradual reduction of restrictive measures might be warranted.

Knot underscored the importance of retaining “full optionality,” a strategy designed to act as a hedge against unpredictable shifts in the economic outlook. He stressed that ECB’s meeting-by-meeting and data-dependent approach has been effective.

Top-tier global economic data take center stage

The global financial markets are bracing for an array of critical economic data this week, from the world’s major economies. The upcoming US presidential election on November 5 adds a layer of complexity. Any unexpected news related to the election could introduce significant volatility, making it imperative to stay informed.

In the US, attention centers on Q3 GDP growth, PCE inflation, ISM Manufacturing Index, and the highly anticipated non-farm payrolls report. Fed has been increasingly focusing on the employment component of its dual mandate, making the October NFP report particularly significant. Currently, market expectations are for Fed to cut interest rates by 25bps at both the November and December meetings. However, these expectations may be recalibrated based on this week’s economic data.

Eurozone is set to release its flash estimate for Q3 GDP and October CPI. While some dovish members of ECB have advocated for discussion of a 50bps rate cut at the December meeting, others have opposed such aggressive easing. The base case remains for a 25bps cut for now. Nevertheless, ECB’s decision will hinge on the depth of economic deterioration reflected in the GDP figures and whether inflation is rebounding as policymakers anticipate.

In Japan, BoJ is expected to maintain its current monetary policy stance during its upcoming meeting. The new economic projections will be crucial in gauging the central bank’s confidence in achieving its 2% inflation target sustainably. This outlook is critical for timing the next rate hike.

For Australia, Q3 CPI release is expected to be pivotal for RBA’s approach to future rate cuts, possibly as early as next year. The inflation data will reveal whether RBA can have the room to relax its vigilant stance against inflation and possibly adjust its guidance in the upcoming meeting. A softer CPI reading could pave the way for a rate cut in early 2025. Additionally, Australia’s economic prospects are closely tied to China’s performance; thus, China’s PMI data will be significant in assessing the impact of government stimulus measures announced since September.

Other noteworthy data releases include Switzerland’s CPI and Canada’s monthly GDP.

Here are some highlights for the week:

- Tuesday: Japan unemployment rate; German Gfk consumer climate; UK M4 money supply, mortgage approvals; US goods trade balance; house price index; consumer confidence.

- Wednesday: Australia CPI; Japan consumer confidence; Germany CPI flash, unemployment GDP; French GDP flash; Swiss KOF economic barometer, UBS economic expectations; Eurozone GDP flash; US ADP employment, GDP advance, pending home sales.

- Thursday: Japan industrial production, retail sales, BOJ rate decision; New Zealand ANZ business confidence; Australia retail sales building approvals, import prices; China PMIs; Germany import price, retail sales; Eurozone CPI flash; Canada GDP; US jobless claims personal income and spending, PCE Inflation, Chicago PMI.

- Friday: Australia PPI; Japan PMI manufacturing final; China Caixin PMI manufacturing; Swiss CPI, retail sales, PMI manufacturing; UK PMI manufacturing final; US non-farm payrolls, ISM manufacturing.

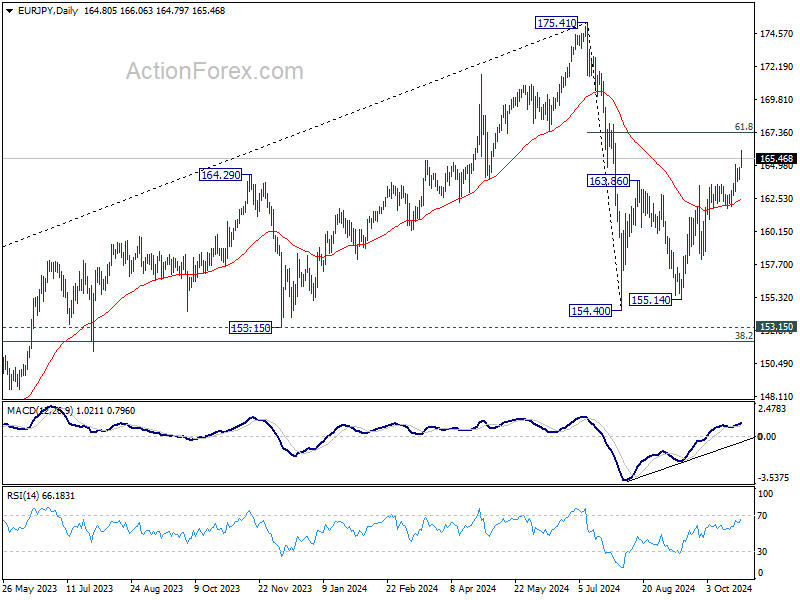

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.98; (P) 164.39; (R1) 164.83; More….

EUR/JPY’s rally resumed after brief consolidations and intraday bias is back on the upside. Current rally from 154.40 should target 61.8% retracement of 175.41 to 154.40 at 167.38. Sustained break there will pave the way to retest 175.41 high. On the downside, below 163.79 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.