Yen Recovers as BoJ Holds Rates; Euro Strengthens Ahead of Inflation Data – Action Forex

Yen recovers broadly today after BoJ left interest rates unchanged, and largely maintained the economic projections unchanged too. The direction of monetary policy remains clear as the next move is a hike if the outlook is realized. Yet, BoJ dropped no clue on the timing. Data from Japan were mixed, with stronger industrial production and weak retail sales, they’re not giving the markets any direction.

Overall, Euro is now the strongest one for the week so far, supported by yesterday’s Eurozone GDP data, which lessen the need for aggressive policy easing from ECB. Focuses will turn to October CPI flash today. An up tick in headline inflation is expected while core inflation would continue the down trend.

Dollar and Swiss Franc are following as the next strongest. Focuses in the US would be on September PCE which would show slight decline in both headline and core inflation. But the main event for the week would be tomorrow’s non-farm payroll which is the most important data for Fed’s near term moves. Still, US presidential election stays as the biggest influence for the US economy and Fed for the medium term.

On the other hand, Aussie continues to sit at the bottom despite today’s slight recovery. Yen is the next worst, followed by Canadian. Kiwi and Sterling are positioning in the middle.

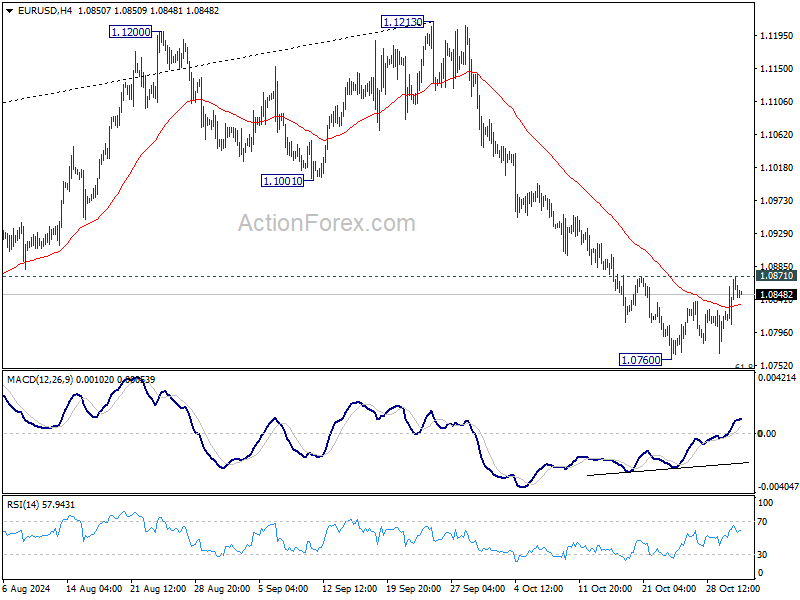

Technically, an immediate focus today is whether EUR/USD could bounce through 1.0871 resistance. That would confirm short term bottoming an 1.0760, on bullish convergence condition in 4H MACD. This development would turn the fall from 1.1213 into consolidation mode first, before staging another decline at a later stage.

In Asia, Nikkei fell -0.50%. Hong Kong HSI is up 0.36%. China Shanghai SSE is up 0.63%. Singapore Strait Times is down -0.88%. Japan 10-year JGB yield is down -0.0055 at 0.947. Overnight, DOW fell -0.22%. S&P 500 fell -0.33%. NASDAQ fell -0.56%. 10-year yield fell -0.008 to 4.266.

ECB’s Lagarde: Inflation target in sight but prudence warranted

In an interview with Le Monde, ECB President Christine Lagarde expressed cautious optimism about Eurozone’s inflation path, noting that the target is “in sight” but stressing that inflation is not yet fully subdued. While headline CPI dipped to 1.7% in September, core inflation, excluding energy and food, remained elevated at 2.7%.

Lagarde acknowledged satisfaction with the recent drop in headline inflation but warned that “inflation is going to rise again in the coming months” due to base effects. Thus, she emphasized that “prudence is warranted.”

She reiterated the importance of reaching the 2% target “on a sustained and durable basis,” projecting that, barring any major shocks, the ECB expects this goal to be achieved by 2025.

BoJ maintains rate at 0.25% on unanimous vote

BoJ kept its uncollateralized overnight call rate steady at approximately 0.25% in a unanimous decision, aligning with market expectations. The central bank indicated that if the outlook for economic activity and prices materializes as anticipated, it will “accordingly continue to raise the policy interest rate and adjust the degree of monetary accommodation.” This signals readiness to tighten monetary policy further, contingent on economic developments.

Nevertheless, BoJ emphasized the necessity of paying close attention to the “future course of overseas economies,” particularly the US, along with developments in financial and capital markets due to their impact on Japan’s economic activity and price outlook.

In its latest economic projections, the BoJ made the following adjustments:

Real GDP Growth:

- Fiscal 2024: Unchanged at 0.6%.

- Fiscal 2025: Revised upward from 1.0% to 1.1%.

- Fiscal 2026: Unchanged at 1.0%.

CPI Core (excluding fresh food):

- Fiscal 2024: Unchanged at 2.5%.

- Fiscal 2025: Revised downward from 2.1% to 1.9%.

- Fiscal 2026: Unchanged at 1.9%.

CPI Core-Core (excluding fresh food and energy):

- Fiscal 2024: Increased from 1.9% to 2.0%.

- Fiscal 2025: Unchanged at 1.9%.

- Fiscal 2026: Unchanged at 2.1%.

Japan’s industrial production rises 1.4% mom in Sep, continues to fluctuate indecisively

Japan’s industrial production increased by 1.4% mom in September, exceeding expectations of 0.8%. This recovery follows a sharp -3.3% mom drop in August when a typhoon disrupted operations across various sectors.

Out of the 15 industrial sectors surveyed, 10, including motor vehicles and chemical production, recorded growth. Five sectors, such as production machinery, saw declines.

Despite this recovery, the Ministry of Economy, Trade and Industry maintained its cautious view, describing industrial production as “fluctuating indecisively.”

Looking ahead, manufacturers polled by the ministry expect a robust 8.3% mom increase in output for October, followed by a -3.7% mom decline in November, indicating ongoing volatility in Japan’s production.

Meanwhile, Japan’s retail sales rose by a modest 0.5% yoy in September, falling significantly short of the anticipated 2.3% yoy growth.

China’s NBS PMI manufacturing rises to 50.1, first expansion in six months

China’s NBS Manufacturing PMI increased to 50.1 in October, meeting expectations and marking the first expansion since April. The improvement was led by large enterprises, which rose to 51.5 from 50.6, while medium-sized firms inched up to 49.4. Small enterprises, however, saw a further contraction, declining to 47.5 from 48.5.

Key subindices pointed to slight domestic improvement: production reached a six-month high of 52.0, and new orders returned to neutral at 50.0 after five months of contraction.

Though still below 50, subindices for employment (48.4), purchases (49.3), imports (47.0), and backlog of orders (45.4) showed smaller declines, suggesting a gradual stabilization.

However, new export orders continued to weaken, reaching an eight-month low at 47.3, underscoring soft external demand.

Non-Manufacturing PMI edged up from 50.0 to 50.2, just shy of the 50.5 forecast, with the employment subindex rising by 1.1 points to 45.8.

NZ ANZ business confidence hits 10-yr high , optimism grows on lower interest rates

New Zealand’s ANZ Business Confidence surged from 60.9 to 65.7 in October, marking its highest level in a decade and reflecting a wave of optimism among businesses.

This renewed confidence is supported by a range of positive indicators: the outlook for own activity increased slightly from 45.3 to 45.9, while export intentions jumped from 13.8 to 17.1, the highest since September 2018. Investment intentions also surged from 9.2, reaching 20.0, the highest level since June 2021, and employment intentions rose from 11.8 to 14.2, the highest since November 2021.

Several key metrics highlight this optimism. Cost expectations dropped from 66.8 to 64.2, indicating some relief in business expenses, while wage expectations edged up slightly from 76.4 to 77.0. Pricing intentions also rose, climbing from 42.8 to 44.2, suggesting businesses may feel confident in passing some costs to consumers. Profit expectations strengthened from 22.2 to 27.0, and inflation expectations continued their downward trend, dipping from 2.92% to 2.82%.

According to ANZ, “steady falls in interest rates” have provided a strong boost to business sentiment, encouraging growth across multiple sectors.

Australia’s retail sales show modest 0.1% mom growth in Sep

Australia’s retail sales turnover increased by a modest 0.1% mom in September, reaching AUD 36.46B but falling short of the expected 0.4% mom rise. This follows a 0.7% gain in August and a flat outcome in July.

Commenting on the data, Robert Ewing, Head of Business Statistics at ABS, noted that “retail spending held firm in September” following a boost in August from warmer-than-usual weather.

The report also highlighted quarterly retail sales volumes, which grew by 0.5% in Q3, marking a recovery after back-to-back declines of -0.4% in both Q2 and Q1.

Ewing added that this increase in volumes reflects “some of the lost ground in discretionary spending this year,” marking only the second quarterly rise in retail volumes over the past two years.

Looking ahead

Eurozone CPI flash is the main focus in European session while unemployment rate will also released. Germany import prices and retail sales will also be published.

Later in the day, US PCE inflation will be the main focus. Jobless claims and Chicago PMI will also be released. Canada will publish monthly GDP.

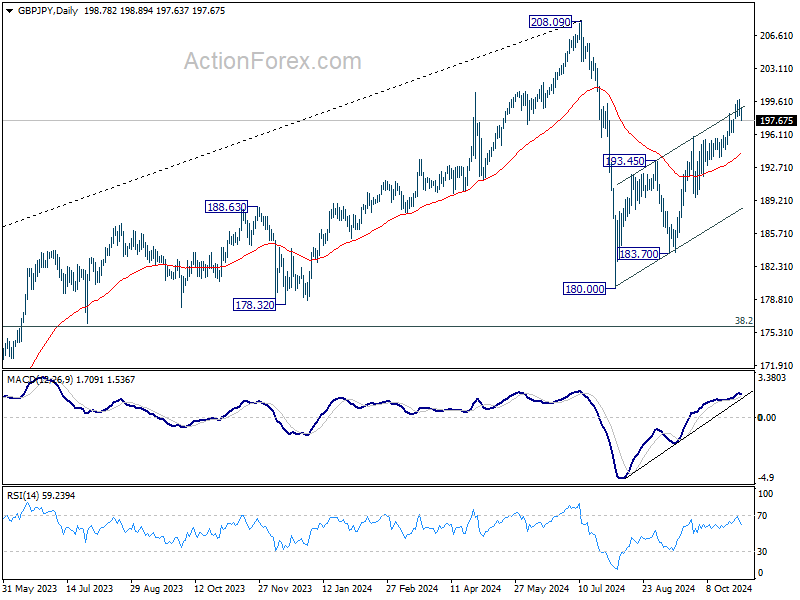

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.10; (P) 198.96; (R1) 199.70; More…

A temporary top is formed at 199.79 in GBP/JPY with current retreat. Intraday bias is turned neutral for consolidations first. Further rally would remain in favor as long as 55 D EMA (now at 194.20) holds. Above 199.79 will resume the rebound from 180.00 to retest 208.09 high. However, sustained break of 55 D EMA will argue that the corrective rise has completed already, and turn near term outlook bearish for 180.00/183.70 support zone.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.