Dollar Gains Momentum on Fed Outlook, Copper Decline Weighs on Aussie – Action Forex

Dollar strengthened broadly overnight, underpinned by the solid rebound in US Treasury yields, while stock markets closed mixed. Stalling disinflation progress, as indicated by the latest CPI data, reinforced the likelihood that Fed will only adopt a gradual approach to lowering interest rates in the future. The aggressive 50bps rate cut back in September is clearly a one-off action that’s not going to be repeated.

Additionally, market participants are increasingly concerned about the inflationary impact of the incoming administration’s fiscal and trade policies. Furthermore, structural changes in the US economy suggest that the terminal rate of the current easing cycle could be higher than previously anticipated. These factors may keep the Fed’s easing hands tied in 2025, limiting the scope for significant policy easing.

In Asian session, selling focus has shifted to Yen, Aussie, and Kiwi, all of which are at the bottom of today’s performance charts. Japanese authorities have remained unusually quiet after USD/JPY breached the 156 level, possibly indicating that the critical 155 threshold is now behind us. This silence could suggest that intervention may only be considered as USD/JPY approaches the next psychological level at 160.

Simultaneously, Aussie and Kiwi are grappling with intensifying concerns over China’s economic outlook, as reflected in continued pressure on Hong Kong equities and Copper prices. US President-elect Donald Trump has nominated Marco Rubio—a prominent China hawk who is sanctioned by China—as Secretary of State. The only way for geopolitical and trade tension between the US and China is on the up, potentially jeopardizing China’s anticipated manufacturing recovery. Moreover, recent stimulus efforts by the Chinese government are perceived as focusing primarily on refinancing local government debt, which may not significantly boost physical demand or stimulate broader economic activity.

Meanwhile, Loonie has shown relative strength, standing as the second best performer for the day, though it broke to a four-year low against the greenback. European currencies are mixed, with the Swiss Franc holding a slight advantage, while the euro and pound trade at more subdued levels.

Technically, Copper is now clearly in downside acceleration as seen in D MACD. Fall from 4.6904 is likely the third leg of the whole down trend from 5.165. Outlook will stay bearish as long as 4.2082 support turned resistance holds, for 3.9127 low first. Decisive break there will target 100% projection of 5.165 to 3.9127 from 4.6904 at 3.4381. Extended weakness in Copper could drag down AUD/USD in the medium term.

In Asia, at the time of writing, Nikkei is up 0.08%. Hong Kong HSI is down -0.75%. China Shanghai SSE is down -0.32%. Singapore Strait Times is up 0.03%. Japan 10-year JGB yield is up 0.0159 at 1.057. Overnight, DOW rose 0.11%. S&P 500 rose 0.02%. NASDAQ fell -0.26%. 10-year yield rose 0.0190 to 4.451.

RBA’s Bullock: Policy to stay restrictive until demand cools to sustainable levels

RBA Governor Michele Bullock commented at a panel discussion today on Australia’s economic and labor market conditions, noting that the economy is still operating at a level that risks fueling inflation.

According to Bullock, while labor market tightness has eased slightly, “it’s still not easy to get staff,” indicating persistent hiring challenges for businesses.

Bullock attributed the resilience in the job market to strong “demand” and “population growth”. These factors, she noted, continue to support employment levels despite some easing in labor market constraints.

Comparing RBA’s policy stance with other central banks, Bullock remarked that while others have already moved to lower rates, RBA remains “not as restrictive.”

Nevertheless, she emphasized that the bank considers its policy “restrictive enough” to address inflation risks and is committed to maintaining this stance until there’s clear evidence of a sustained “downward trajectory in demand.”

Australia’s employment growth 15.9k in Oct, slowest rate in recent months

Australia’s employment grew modestly in October, rising by 15.9k or 0.1% mom, falling short of the anticipated 25k increase. This represents the slowest pace of employment growth in recent months, following a period of more robust gains averaging 0.3% per month over the last six months. Full-time positions rose by 9.7k, while part-time jobs increased by 6.2k, both contributing to the incremental rise.

Unemployment rate remained steady at 4.1%, matching expectations, although the participation rate saw a slight dip from 67.2% to 67.1%. The number of unemployed rose by 1.3% mom, adding 8.3k to the job-seeking pool. In terms of labor utilization, monthly hours worked inched up by 0.1% mom, reflecting only minimal expansion in total labor demand.

This marks the third consecutive month with an unemployment rate of 4.1%, which stands 0.6% points higher than June 2023 low of 3.5%. Nonetheless, this rate remains 1.1% below the pre-pandemic level of 5.2% in March 2020.

The deceleration in employment growth could indicate a stabilizing labor market, aligning with recent RBA commentary on maintaining a restrictive policy stance until clear demand cooling is observed.

Fed’s Musalem: To cut judiciously and patiently as inflation risks rising

St. Louis Fed President Alberto Musalem stated in a speech overnight that he expects inflation to converge toward the Fed’s 2% target over the medium term. His baseline scenario anticipates a cooling labor market that remains within the range of full employment, alongside moderating compensation growth.

Musalem emphasized that this outlook depends on monetary policy staying “appropriately restrictive” while inflation exceeds 2%, a situation that would allow Fed to “judiciously and patiently” continue lowering interest rates.

However, Musalem expressed concerns that recent information indicates the risk of inflation failing to converge toward 2%, or even moving higher, “has risen.”

Simultaneously, he noted that the risk of an unwelcome deterioration in the labor market “has remained unchanged or possibly fallen.”

Although he is “attuned to the possibility of rising layoffs going forward,” Musalem believes the overall strength of the economy “provides some confidence that a disorderly labor market deterioration is unlikely.”

Fed’s Schmid: Rate cut depth unclear, productivity holds key

Kansas City Fed President Jeffrey Schmid highlighted overnight Fed’s confidence that inflation is on track to reach its 2% target, attributing this progress to “signs that both labor and product markets have come into better balance in recent months.”

Schmid acknowledged that conditions are right to begin easing the Fed’s restrictive monetary policy but stressed that “it remains to be seen how much further interest rates will decline or where they might eventually settle.”

He added that sustained gains in productivity could enable the economy to grow robustly without significant inflation. However, Schmid cautioned that economic growth could be dampened if the energy supply fails to meet the increasing demands, such as those driven by AI development.

“As an optimist, my hope is that productivity growth can outrun both demographics and debt,” yet as a central banker, he remains committed to the Fed’s dual mandate, ensuring price stability and full employment, guided by data.

Looking ahead

ECB meeting accounts is the main focus in European session. Eurozone will publish GDP revision and industrial production. Later in the day, US will release PPI and jobless claims.

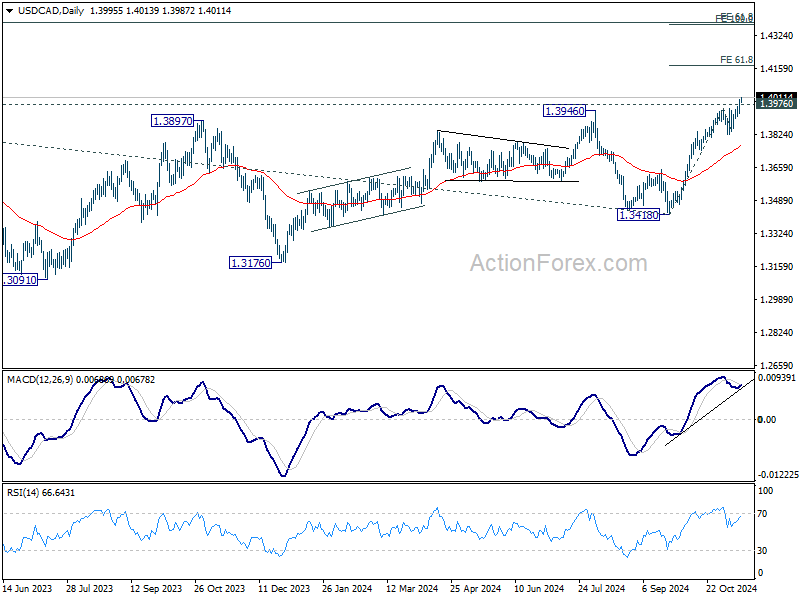

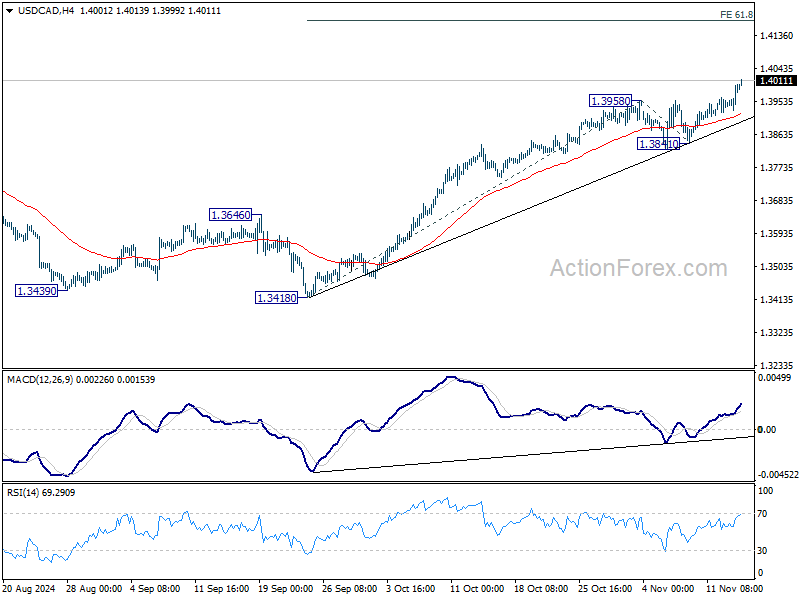

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3951; (P) 1.3977; (R1) 1.4025; More…

USD/CAD surges through 1.3976 key resistance as larger up trend resumes. Intraday bias is back on the upside. Next near term target is 61.8% projection of 1.3418 to 1.3958 from 1.3841 at 1.4175. For now, outlook will stay bullish as long as 1.3841 support holds, in case of retreat.

In the bigger picture, up trend from 1.2005 (2021) is resuming with break of 1.3976 key resistance (2022 high). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.