European Majors Dip in Holiday Calm, China’s PMIs Next – Action Forex

The forex markets remain subdued as traders maintain a cautious stance ahead of the New Year. European major are notably weaker, with Swiss Franc leading the declines. Euro is also under pressure, while Sterling has shown resilience, managing to avoid sharper losses.

Meanwhile, Yen has staged a modest recovery, supported by easing US and European benchmark yields, which have tempered earlier selloffs. Commodity currencies, including Australian Dollar, are firming slightly as they digest steep losses accumulated over December. Dollar is trading sideways, reflecting an overall lack of momentum as the markets consolidate in thin year-end trading.

Looking ahead, attention is on China’s NBS PMIs, scheduled for release during the upcoming Asian session. Expectations point to slight expansions in both the manufacturing and non-manufacturing sectors for December, which could provide insights into the state of China’s recovery efforts.

Adding to the focus, President Xi Jinping is set to deliver his New Year’s address later in the week. Markets will be keen to parse his remarks for any reaffirmation of commitments to revive China’s struggling economy.

China’s authorities have already pledged to issue CNY 3 trillion in special treasury bonds in 2025 to boost fiscal stimulus, although further details are unlikely until March’s National People’s Congress. Analysts remain cautious about the effectiveness of these measures, particularly given structural challenges such as sluggish household consumption and a soft real estate market.

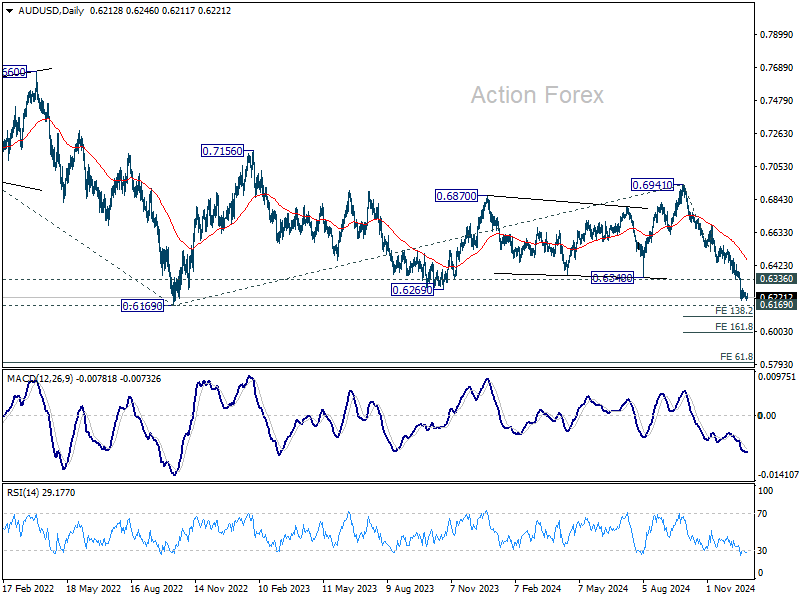

Aussie would be particularly sensitive to developments in China. While downside surprises in tomorrow’s Chinese PMI data could reignite selling pressure in AUD/USD, 0.6169 (2022 low) could continue to act as a critical support level. Yet any recovery might be capped below 0.6336 support turned resistance. The next big move would hinge on both the development surrounding China’s outlook in 2025, as well as whether RBA would start easing sooner in February.

In Europe, at the time of writing, FTSE is down -0.51%. DAX is down -0.38%. CAC is down -0.41%. UK 10-year yield is down -0.024 at 4.616. Germany 10-year yield is down -0.021 at 2.377. Earlier in Asia, Nikkei fell -0.96%. Hong Kong HSI fell -0.24%. China Shanghai SSE rose 0.21%. Singapore rose 0.64%. Japan 10-year JGB yield fell -0.0106 to 1.094.

Swiss KOF falls below average, signals dampened outlook

Swiss KOF Economic Barometer fell to 99.5 in December, down from 102.9 in November and below market expectations of 101.1. This decline brings the indicator slightly below its medium-term average, signaling a “dampened” outlook for the Swiss economy .

KOF Economic Institute attributed the drop to weaker performance across multiple sectors. In particular, indicators for manufacturing, other services, the hospitality industry, foreign demand, and private consumption showed significant declines, collectively driving the overall decrease.

Japan’s PMI manufacturing finalized at 49.6, nears stabilization and cost pressures persist

Japan’s Manufacturing PMI for December was finalized at 49.6, an improvement from November’s 49.0, indicating a gradual move toward stabilization in the sector.

According to Usamah Bhatti of S&P Global Market Intelligence, the data “painted a picture of a near-stabilization” in manufacturing conditions as declines in both production and new orders softened.

Encouraged by these improvements, firms increased hiring, partly to address existing labor shortages and in anticipation of future demand recovery.

However, price pressures remained elevated, with input costs rising at their fastest pace since August due to higher raw material and labor costs, compounded by Yen’s weakness. To manage these cost burdens, manufacturers passed on higher prices to clients, resulting in the strongest output charge increases in five months.

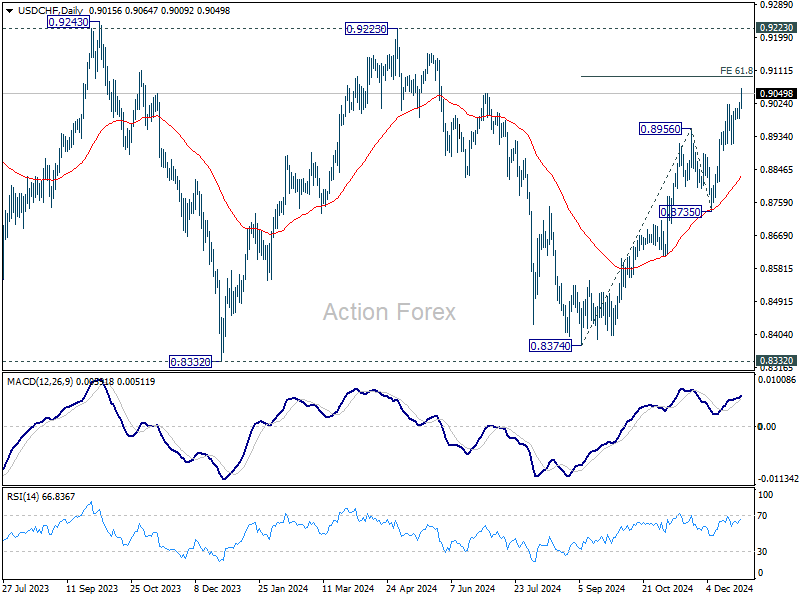

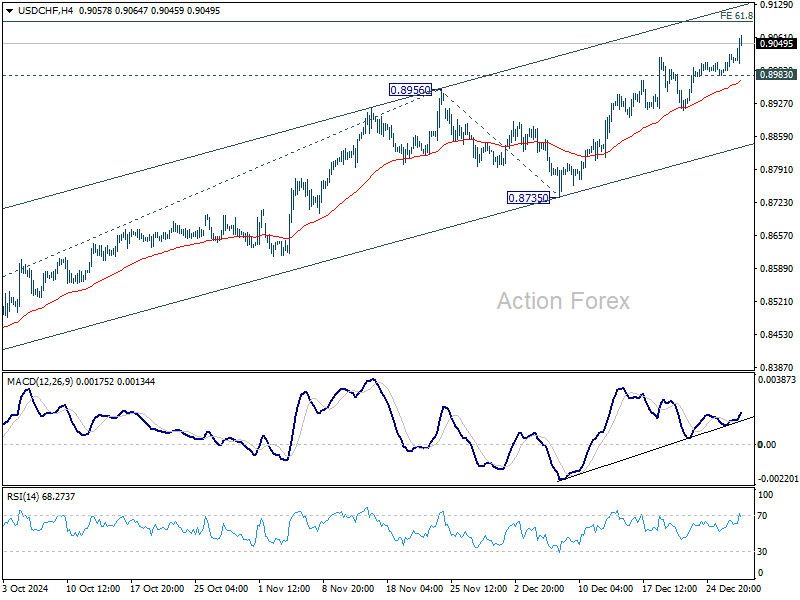

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8995; (P) 0.9011; (R1) 0.9038; More…

USD/CHF’s rally continues today and intraday bias stays on the upside. Rise from 0.8374 is in progress for 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095. On the downside, below 0.8983 minor support will turn bias neutral and bring consolidations again first.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.