Manufacturing Stabilization Supports Dollar, European Struggle Continues – Action Forex

Dollar strengthened modestly following the latest ISM Manufacturing PMI, which indicated some stabilization in the US manufacturing sector toward the end of 2024. Despite the improvement, the sector continues to face challenges, with half of its industries still contracting.

The ISM report did little to shift expectations that Fed will pause its easing cycle at its next meeting on January 29, with fed fund futures pricing an 88% chance of a hold. Market attention now turns to next week’s ISM services data and the non-farm payroll report to further solidity this expectation.

For the holiday-shortened week, Yen is currently the best perform, in tight race with second-placed Dollar, while Canadian is the third. On the other hand European majors are clearly struggling with Sterling at the bottom, followed by Euro and then Swiss Franc. Aussie and Kiwi are positioning in the middle.

In Europe, at the time of writing, FTSE is down -0.38%. DAX is down -0.62%. CAC is down -1.49%. UK 10-year yield is down -0.0335 at 4.566. Germany 10-year yield is up 0.032 at 2.415. Earlier in Asia, Japan was still on holiday. Hong Kong HSI rose 0.70%. China Shanghai SSE fell -1.57%. Singapore Strait Times rose 0.03%.

US ISM manufacturing improves to 49.3, but remains in contraction territory

US ISM Manufacturing PMI edged up from 48.4 to 49.3 in December, exceeding market expectations of 48.3. Despite the improvement, the index remained below the 50.0 threshold, signaling contraction for the ninth consecutive month and for the 25th time in the past 26 months.

The ISM highlighted that the December reading corresponds to an annualized 1.9% growth in real GDP, indicating a modest contribution to the broader economy.

Delving into the subcomponents, new orders climbed from 50.4 to 52.5, while production improved notably, rising from 46.8 to 50.3. However, employment fell sharply from 48.1 to 45.3. Additionally, prices accelerated, increasing from 50.3 to 52.5, pointing to renewed input cost pressures.

Yuan Pressure Against Dollar, But Rises Against CFETS Basket

The Chinese Yuan presented an interesting paradox in today’s market action. Onshore Yuan sank below 7.3 mark against US Dollar, registering a 14-month low. This decline has intensified speculation that the People’s Bank of China might be adopting a more lenient stance toward currency depreciation. Such a move could be part of broader efforts to bolster economic growth amid mounting headwinds. The downward bias has been further fueled by the possibility of a renewed “Trade War 2.0” under the incoming US administration.

Conversely, the CFETS RMB Index—a measure of the Yuan’s trade-weighted performance against a basket of currencies—surged to its highest level since October 2022. Although primarily driven by the relative weakness of major currencies versus the Dollar, this uptick hints at potential challenges for China’s export competitiveness to other key markets.

These moves also coincide with CFETS basket weighting adjustments for 2025, including reductions in the weightings of Dollar (from 19.46% to 18.903%), Euro (from 18.08% to 17.902%), and Yen (from 8.963% to 8.584%).

The larger question remains: How far is China willing to let Yuan depreciate? This is a mounting question given the uncertainty surrounding any trade measures the US might impose after Donald Trump’s January 20 inauguration. Beijing’s true intentions would become clearer after that.

Technically, it does look like that USD/CNH (Dollar vs offshore Yuan) is ready to resume it’s long term up trend from 6.3057 (2022 low). Decisive break of 7.3745 (2022 high) will pave the way to 100% projection of 6.6971 to 7.3673 from 6.9709 at 7.6411.

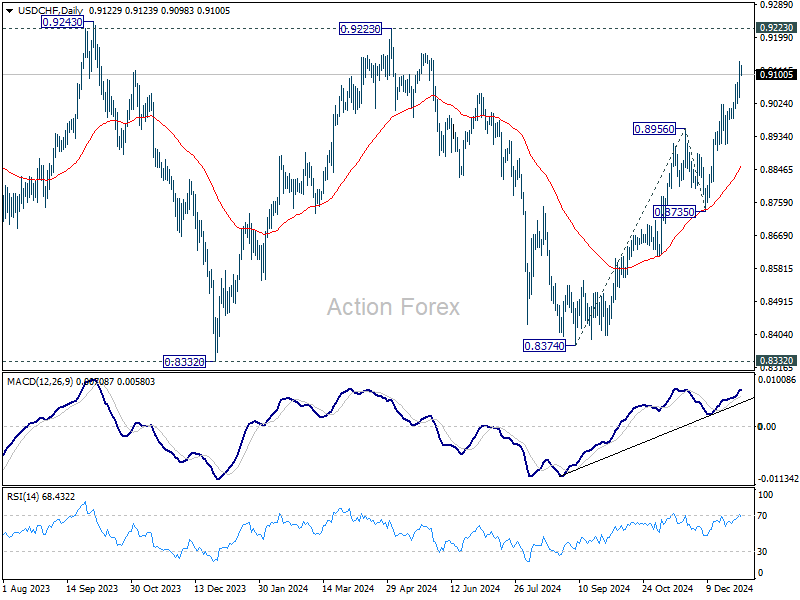

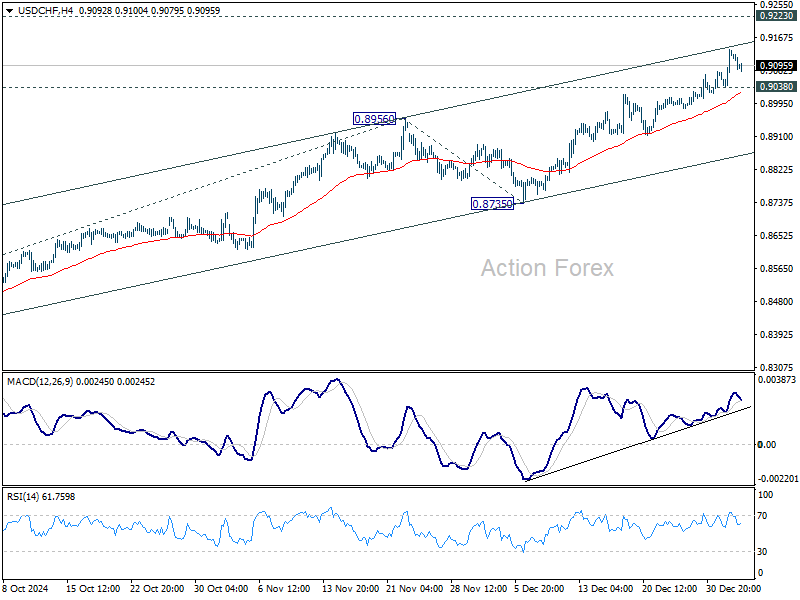

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9063; (P) 0.9100; (R1) 0.9161; More…

Intraday bias in USD/CHF stays on the upside for now despite current shallow retreat. Rally from 0.8374 is in progress for 0.9223 key resistance. Strong resistance is expected there to limit upside, at least on first attempt. On the downside, below 0.9038 minor support will turn intraday bias neutral first. Nevertheless, decisive break of 0.9223 will carry larger bullish implications.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.