Sterling Tumbles Amid UK Bond Selloff, Dollar Backed by Resilient Data – Action Forex

Sterling plunged across the board as the sharp selloff in UK government bonds sent shockwaves through financial markets. Yields on 10-year gilts surged to their highest levels since August 2008, while 30-year yields reached a 26-year high. These developments have reignited concerns about the UK’s fiscal health and are reminiscent of the turmoil during Liz Truss’s brief tenure as shortest serving UK Prime Minister back in 2022. However, it’s emphasized that the current moves in Sterling and gilt yields remain much less dramatic than those seen during the mini-budget crisis.

Meanwhile, Dollar continues to find support from robust economic data. Yesterday’s ISM services report highlighted resilience in the sector, while the slight miss in ADP private employment numbers did little to shake optimism about the labor market, with Friday’s non-farm payroll report poised as a critical test. FOMC minutes reiterated that Fed is close to slowing down the policy easing cycle. Current pricing in Fed fund futures reflects an 85% likelihood of just one 25bps rate cut by Fed by the end of 2025.

For the week, Loonie leads the pack so far, closely followed by Dollar. However, USD/CAD remains in near-term consolidation phase within a broader up trend. Euro stands as the third strongest currency, supported by flows out of Sterling. On the weaker side, Sterling sits at the bottom, followed by Yen and Kiwi, while Swiss Franc and Aussie occupy middle positions.

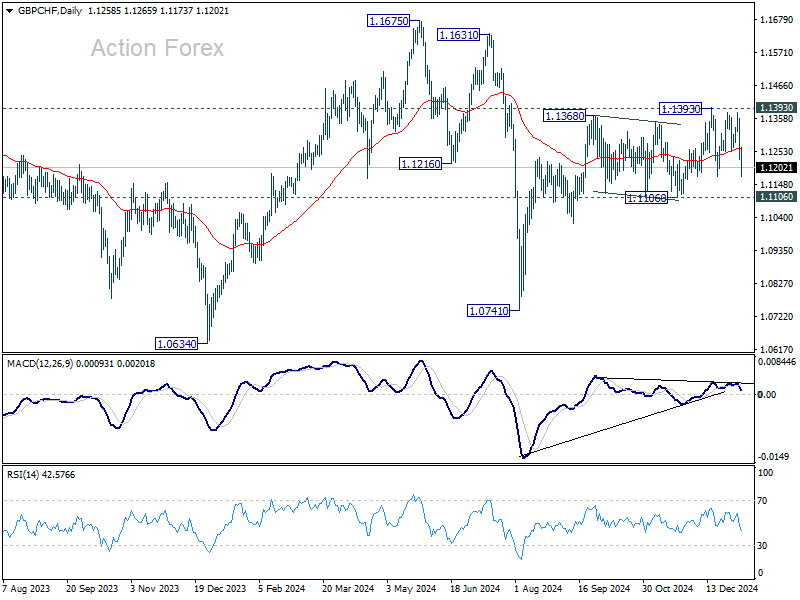

Technically, while GBP/CHF dives deeply this week, downside is still contained well above 1.1106 structural support. The cross is seen as in a sideway pattern between 1.1106/1393 only, and near term outlook is neutral at worst. Rally from 1.0741 is still in favor to resume through 1.1393 at a later stage, as the markets are back to normal with expectations on SNB rate cut and stabilization in UK sentiment. However, firm break of 1.1106 will indicate bearish trend reversal, and indicates some important underlying bearish fundamental developments.

BoJ regional report highlights broadening price hikes

BoJ, in its latest Regional Economic Report, upgraded its economic outlook for two of Japan’s nine regions—Tohoku and Hokuriku—citing signs of moderate recovery.

The assessment for the remaining seven regions was left unchanged, with all areas described as either “picking up” or “recovering moderately.”

The report highlighted an increasingly widespread trend of price hikes by firms aiming to accommodate rising wages. While some companies, particularly larger ones, are already deliberating the scale of wage increases, smaller firms remain cautious. Concerns about the impact of higher costs on profit margins have slowed their willingness to commit to pay raises.

Japan’s nominal wage gains hit 3% in Nov, but inflation erodes real earnings

Japan’s real wages fell by -0.3% yoy in November, marking the fourth consecutive monthly decline as wage growth failed to outpace inflation again.

While nominal wages rose by a robust 3.0% yoy—beating expectations of 2.7% yoy and extending a 35-month streak of growth—consumer prices grew at an even faster pace of 3.4% yoy during the same period, up from 2.6% yoy in October.

A notable highlight in the data was the sharp rise in special cash earnings, including bonuses, which surged by 7.9% yoy. Excluding bonuses and nonscheduled payments, average wages increased by 2.7% yoy, the fastest rate in 32 years, suggesting some underlying improvement in base wages.

Australia’s retail sales growth misses expectations at 0.8% mom in Nov

Australia’s retail sales increased by 0.8% mom in November, falling short of market expectations for 1.1% mom rise. Despite the miss, all retail industries recorded growth during the month, reflecting the ongoing impact of Black Friday.

This marks the third consecutive month of retail sales growth, following gains of 0.5% mom October and 0.4% mom in September. The steady trend highlights a degree of resilience in consumer spending, though the pace remains moderate.

Robert Ewing, head of business statistics at the Australian Bureau of Statistics, noted “Black Friday sales events proved once again to be a big hit”. He also pointed out that the sales promotions now extend beyond the traditional weekend, influencing spending patterns across the entire month of November.

China’s inflation stalls at 0.1% in Dec, factory prices remain deflationary

China’s inflation decelerated again in December, with the CPI rising only 0.1% yoy, matching expectations and marking the slowest pace since April.

This brings full-year inflation for 2024 to 0.2%, far below the official target of around 3%, extending a 13-year streak of missing the annual inflation goal.

Core inflation, which strips out volatile food and energy prices, offered a slight reprieve, ticking up from 0.3% yoy to 0.4% yoy, the highest in five months.

PPI data showed a marginal improvement, with factory-gate prices contracting by -2.3% yoy compared to -2.5% yoy in November, slightly better than market expectations of -2.4% yoy. However, PPI has now stayed in deflationary territory for an extended 27 months.

FOMC minutes signal nearness to slow pace of rate cuts

The minutes from Fed’s December meeting revealed divided sentiment among policymakers regarding the latest rate cut. While the decision to lower rates was ultimately made, it was described as “finely balanced,” with some participants emphasizing the “merits” of pausing rate reductions given persistent challenges in curbing inflation.

The minutes highlighted a growing sense within the FOMC that monetary easing might need to slow. After a cumulative 100 basis points of cuts in 2024, participants noted that the Committee is “at or near the point at which it would be appropriate to slow the pace of policy easing.” Most agreed that a more cautious approach would be prudent when considering additional rate adjustments.

The inflation outlook remained a key area of focus. While participants expected inflation to gradually align with the 2% target, recent higher-than-anticipated inflation readings and uncertainty stemming from potential changes in trade and immigration policy raised concerns.

These developments suggest that the disinflation process may “take longer than previously anticipated”, with some participants observing signs that progress might have stalled temporarily.

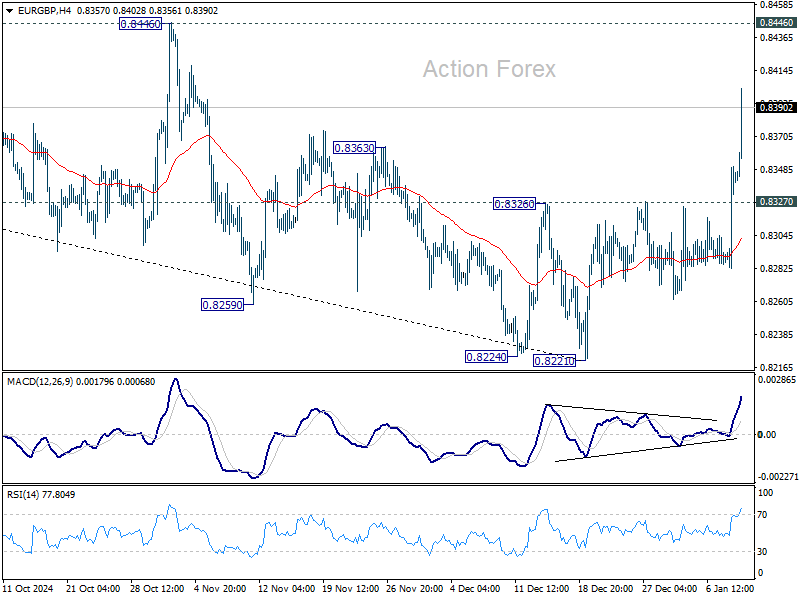

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8301; (P) 0.8326; (R1) 0.8373; More…

EUR/GBP’s rally from 0.8221 accelerates higher today and intraday bias stays on the upside for 0.8446 key resistance. Strong resistance might be seen there to limit upside, at least on first attempt. But for now, further rally will remain in favor as long as 0.8327 resistance turned support holds, in case retreat. Decisive break of 0.8446 will carry larger bullish implications.

In the bigger picture, considering bullish convergence condition in D MACD, decisive break of 0.8446 resistance should confirm medium term bottoming at 0.8221, just ahead of 0.8201 key support (2022 low). Further rally should be seen towards 0.8624 key resistance, even as a correction to the down trend from 0.9267 (2022 high). Overall, however, medium term outlook will be neutral at best until decisive break of 0.8624 cluster zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621). Risk will stay on the downside even in case of strong rebound.