NFP Set to Boost Dollar, But Trump Inauguration Risks May Limit Sustained Gains – Action Forex

Dollar holds onto its leadership position as markets await the US non-farm payroll report. Investors expect the data to reinforce Fed’s decision to pause rate cuts this month, particularly if the report confirms continued labor market strength. In such a scenario, rising US Treasury yields could further bolster the greenback.

However, any post-NFP rally might be short-lived, given the looming inauguration of President-elect Donald Trump on January 20. Trade policy rumors have already spurred market volatility, with conflicting reports about sector-specific tariffs and the possible use of emergency powers. Traders may be quick to take profits after NFP-driven moves, wary of sudden developments in Washington.

For the week, Canadian Dollar remains the top performer, consolidating gains against the second-ranked Dollar. Euro occupies third place, while Sterling languishes at the bottom, pressured by concerns over UK fiscal stability. Swiss Franc and Yen are next weakest, as Euro and Australian Dollar sit at middle positions.

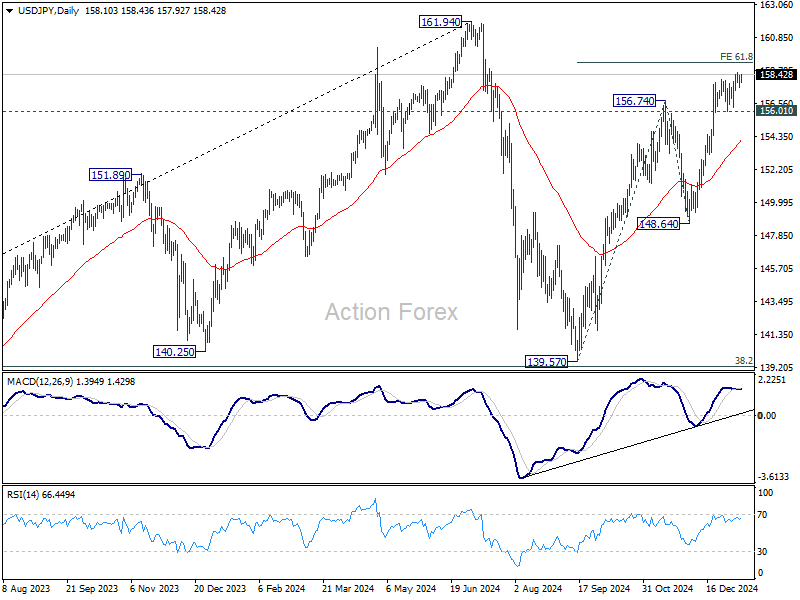

Technically, USD/JPY has seen its rally slow just shy of 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25. Caution is rising as the pair approaches 160 psychological level, where intervention risk from Japan looms. Nonetheless, further upside is favored as long as 156.01 support holds, pointing to a test of the 161.94 high once 159.25 is cleared. That zone represents significant resistance and could cap any near-term gains.

NFP to anchor Fed pause, 10-year yield eyes higher level

US non-farm payroll report is taking center stage today as markets look for confirmation of Fed’s anticipated decision to pause rate cuts this month. Recent comments from multiple Fed officials have highlighted a cautious approach to further monetary easing, with a consensus forming that the central bank is nearing a pause in its rate-cutting cycle.

Fed fund futures currently price 93% likelihood of a hold at the meeting, and an in-line or stronger-than-expected jobs report could push this probability closer to certainty.

The broader debate now shifts to two key questions: how long the Fed’s pause might last and how much more easing, if any, will occur this year. Current market pricing indicates a 60% chance of another hold in March, followed by a 53% probability of a rate cut in May. For the rest of 2025, markets see over an 85% chance that rates will remain steady at 4.00%-4.25%.

Following today’s data, the immediate focus is whether the odds of a March hold increase, reflecting an extended pause.

Regarding expectations on the data, for December, headline job growth is forecasted to slow to 150k, with the unemployment rate expected to hold steady at 4.2%. Average hourly earnings are anticipated to rise by 0.3% month-over-month.

While some signals, such as the ISM Manufacturing PMI Employment component falling to 45.3 and ADP private employment growth decelerating to 122k, point to a cooling labor market, others remain robust. ISM Services PMI Employment component held steady at 51.4, and the 4-week moving average of initial jobless claims fell to a historically strong 213k, suggesting resilience and leaving room for an upside surprise in today’s report.

In terms of market reactions, a major focus is on treasury yields. Technically, 10-year yield breached 61.8% projection of 3.603 to 4.505 from 4.126 at 4.683 this week, as rally from 3.603 resumed.

Strong NFP number could push TNX higher, and sustained trading above 4.683 should pave the way towards 100% projection at 5.028, which is close to 4.997 high, and 5% psychological level. Any upside acceleration could realize this target at around the end of Q1.

In any case, outlook in TNX will stay bullish as long as 4.517 support holds, in case of retreat.

Japan’s household spending falls for fourth month, minister flags critical economic transition

Japan’s household spending declined for the fourth consecutive month in November, falling -0.4% yoy. While this was an improvement from October’s -1.3% drop and surpassed expectations of -0.8%, it still reflects ongoing consumer caution.

The decline was driven by significant cuts in expenditures on home appliances and food, highlighting weak domestic demand.

Spending on furniture and electric appliances plummeted by -13.8%, marking the third straight month of decline, while clothing and footwear saw a similar drop -of 13.7%, down for the second consecutive month. Food purchases also contracted slightly, falling by-0.6%.

Separately, Economy Minister Ryosei Akazawa acknowledged the challenges, stating that Japan’s economy is at a “critical stage” in shifting public sentiment away from deflation and toward sustainable growth driven by higher wages and investment.

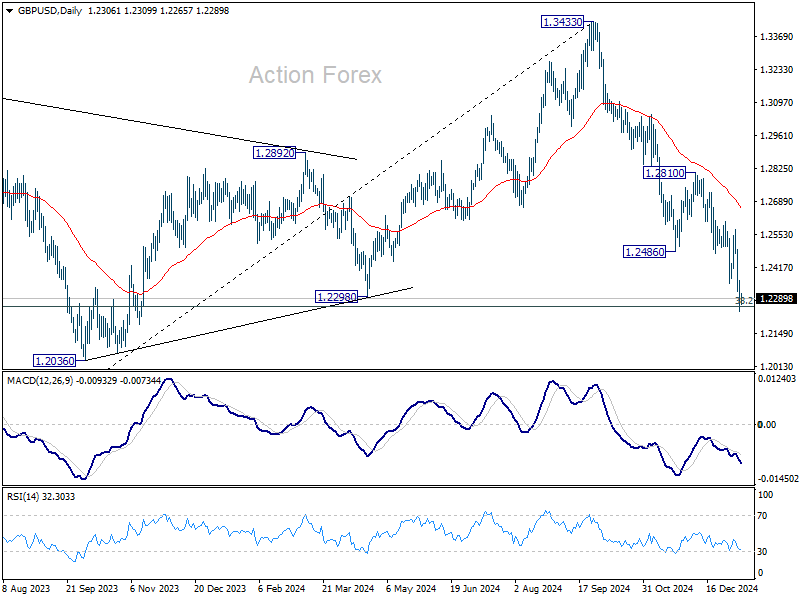

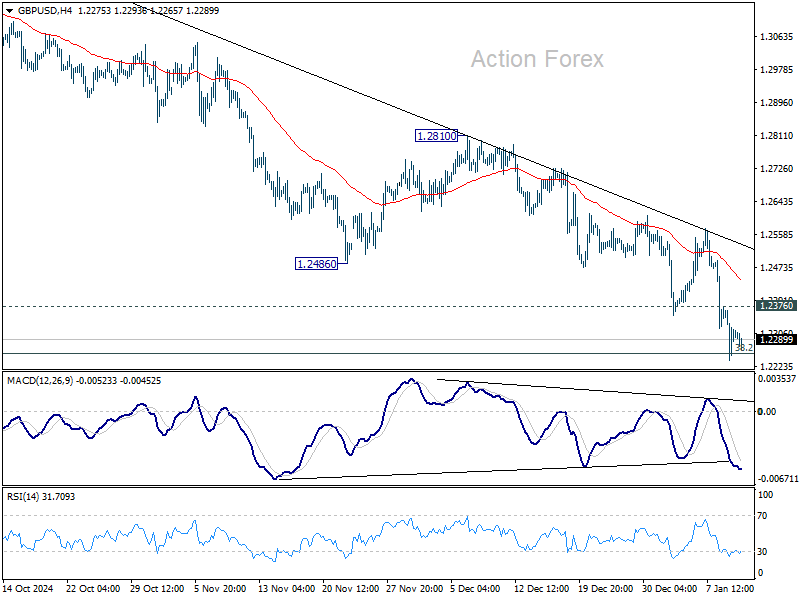

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2240; (P) 1.2306; (R1) 1.2375; More…

There is no clear sign of bottoming yet in GBP/USD and intraday bias remains on the downside. Sustained trading below 1.2256 fibonacci level will carry larger bearish implications. On the upside, break of 1.2376 will turn intraday bias neutral first. Further break of 1.2486 support turned resistance should confirm short term bottoming.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Strong support is still expected from 38.2% retracement of 1.0351 to 1.3433 at 1.2256 to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.