Sterling Slides Further as UK Fiscal Concerns Persist, UK-China Trade Efforts Fail to Reassure Markets – Action Forex

Sterling extended its losses at the start of the week as deepening concerns over the UK’s fiscal situation continued to dominate market sentiment. Yields on 10-year UK Gilts surged above 4.88%, inching closer to the psychologically significant 5% mark. Market participants remain skeptical about the government’s fiscal discipline, despite repeated reassurances from Chancellor Rachel Reeves.

At a press conference in China, Reeves reaffirmed her commitment to fiscal responsibility, stating, “We will pay for day-to-day spending through tax receipts and we will get debt down as a share of GDP.” However, these declarations fell flat with the markets, which is ore focused on the UK’s mounting fiscal challenges and sluggish economic growth.

Reeves’ attempts to rejuvenate UK-China trade ties also failed to make a meaningful impact on sentiment. During her visit to Beijing, she announced trade and investment agreements worth GBP 600m over the next five years, following discussions with Chinese Vice-Premier He Lifeng.

However, markets dismissed the news, viewing it as insufficient to offset broader economic and fiscal challenges. Domestically, Reeves faced criticism for engaging too closely with China, with some accusing her of compromising national interests for limited gains.

In broader currency markets, Pound is currently the worst performer of the day, with Euro close behind. Dollar, consolidating last week’s robust gains, ranks as the third weakest currency. On the other hand, Yen tops the leaderboard, benefiting from renewed risk aversion among investors. Aussie follows, buoyed by upbeat Chinese trade data, while Kiwi ranks third. Swiss Franc and Canadian Dollar are positioning in the middle.

The upcoming week promises significant developments, with key inflation reports from the US, UK, and Australia, alongside UK GDP figures.

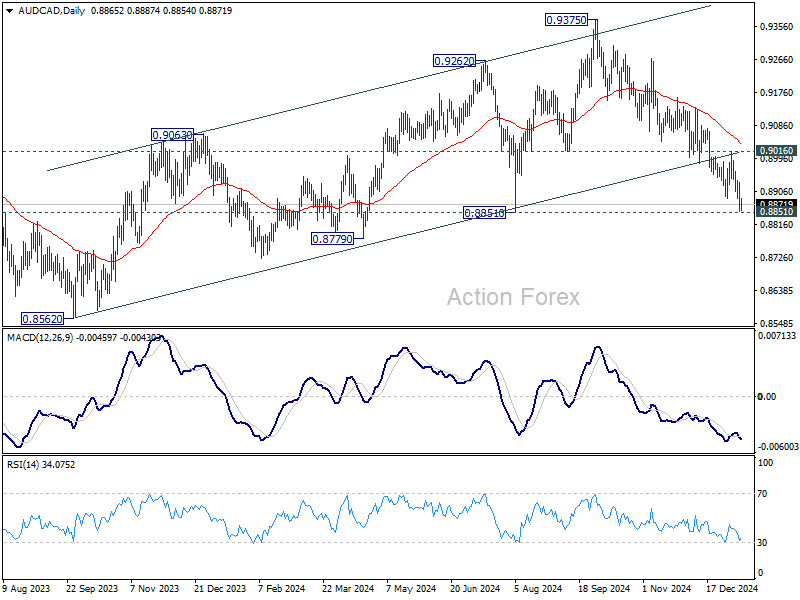

Technically, AUD/CAD’s fall from 0.9375 continued last week and edged closer to 0.8851 structural support. Decisive break there should confirm that whole corrective rebound from 0.8562 (2023 low) has completed, and solidify medium term bearishness for retesting this low. Nevertheless, strong bounce from current level, followed by break of 0.9016 resistance, will keep the rise from 0.8562 alive for another rally through 0.9375 at a later stage.

ECB’s Lane stresses the need for “middle path” on interest rates

ECB Chief Economist Philip Lane, in an interview with Der Standard, highlighted that a “middle path” is essential to achieving the inflation target without stifling economic growth or allowing inflationary pressures to persist.

Lane warned that if interest rates fall too quickly, it could undermine efforts to bring services inflation under control. On the other hand, keeping rates too high for too long risks that inflation could “materially fall below target”.

“We think inflation pressure will continue to ease this year,” Lane stated, while adding that wage increases in 2025 are expected to moderate significantly, which could contribute to a softer inflationary environment.

While acknowledging that the overall direction of monetary policy is clear, Lane underlined the complexities of striking the right balance of “being neither too aggressive nor too cautious.”

China’s monthly trade surplus soars to USD 104.8B as exports jumps 10.7% yoy

China’s trade data for December delivered a solid performance, reflecting resilience in exports and a surprising recovery in imports.

Exports surged 10.7% yoy, significantly outpacing the 7.3% yoy expected growth and accelerating from November’s 6.7%.

Shipments to major markets rose sharply, with exports to the US jumping 18.9% yoy, ASEAN by 15.6% yoy, and the EU by 8.7% yoy. Some analysts highlighted that front-loading ahead of the Lunar New Year and trade policy shifts under Donald Trump’s incoming administration likely bolstered the month’s figures.

Imports grew 1.0% yoy, defying expectations of a -1.5% yoy decline and marking a rebound after consecutive contractions of -3.9% yoy in November and -2.3% yoy in October. This recovery was driven in part by increased purchases of commodities like copper and iron ore, with importers potentially capitalizing on lower prices.

Regionally, imports from the US rose by 2.6% yoy, while ASEAN imports grew 5.4% yoy. However, imports from the EU fell by -4.9% yoy.

Trade surplus widened from USD 97.4B in November to USD 104.8B in December, surpassing expectations of USD 100B.

Looking ahead, markets will closely monitor China’s upcoming GDP figures, due for release on Friday. Expectations are for fourth-quarter growth to clock in at 5.0% yoy.

Market focus on US inflation and UK growth as Sterling and Aussie face risks

Markets are preparing for a critical week with Dollar, Sterling, and Aussie all facing major economic releases.

In the US, upcoming CPI and retail sales reports will command attention, especially following last week’s strong employment data that has rattled expectations about Fed’s next move. With non-farm payrolls far exceeding forecasts, traders have priced out the likelihood of a rate cut in the first quarter, turning their gaze instead to May or even June as the earliest possibility.

Fed officials, who have long noted balanced risks to the dual mandate, could pivot more hawkishly if inflation readings surprise on the upside. Should CPI data reveal resurgence in price pressures, markets may be forced to extend their timeline for a Fed rate cut.

Such a shift would likely offer further support to Dollar, which is already benefiting from the resilience of US labor markets and the potential for sustained higher interest rates.

Meanwhile, US retail sales report will provide an additional gauge of consumer demand; robust spending could reinforce the notion that Fed has limited room to ease policy in the near term, keeping the Dollar well-bid.

In the UK, Sterling is bracing for GDP, CPI, and retail sales figures. The Pound suffered sharp decline last week amid intensifying concerns over fiscal de-anchoring and stagflation.

Should UK economic data disappoint on growth—particularly GDP or retail sales—the currency could face renewed selling pressure. Although upside surprises in inflation remain possible, investors appear more wary of signs that British growth is faltering in the wake of the Autumn budget measures.

In Australia, markets are closely weighing whether RBA will commence its easing cycle in February or May. Much hinges on labor market developments. If job data continues to weaken, policymakers may have room to act sooner. Attention will then shift to Q4 CPI data, due in about two weeks, as a decisive factor in clarifying RBA’s direction.

Meanwhile, external factors also come into play: China’s upcoming GDP release, along with a host of other indicators, could influence regional sentiment and, by extension, Australian Dollar.

Here are some highlights for the week ahead:

- Monday: China trade balance; Swiss SECO consumer climate.

- Tuesday: Australia Westpac consumer sentiment; Japan current account; US PPI.

- Wednesday: Japan machine tool orders, UK CPI; Eurozone industrial production; Canada manufacturing sales, wholesale sales; US CPI, Empire state manufacturing, Fed’s Beige Book.

- Thursday: Japan PPI; Australia employment; UK GDP, production, trade balance; Eurozone trade balance, ECB accounts; US retail sales, jobless claims, Philly Fed survey, import prices, business inventories, NAHB housing index.

- Friday: New Zealand BNZ manufacturing; China GDP, industrial production, retail sales, fixed asset investment; UK retail sales; Eurozone CPI final; US building permits and housing starts, industrial production and capacity utilization.

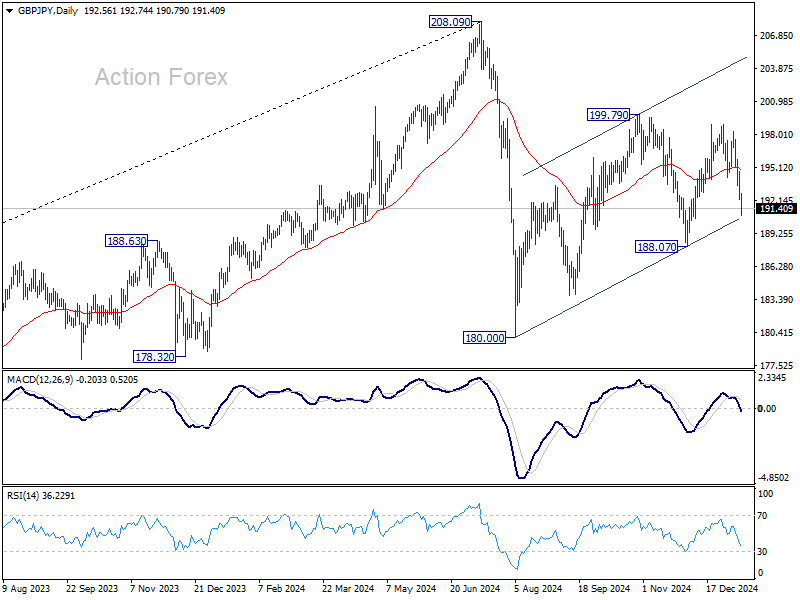

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.61; (P) 193.20; (R1) 194.19; More…

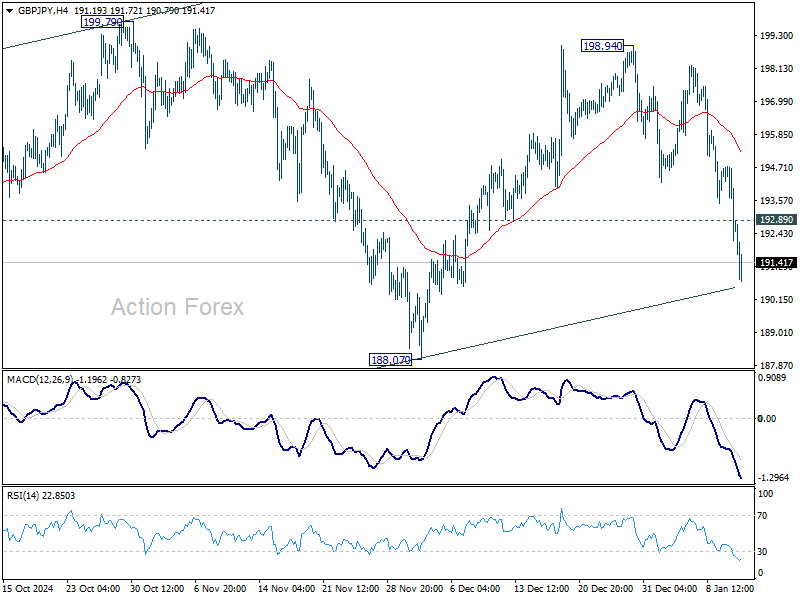

GBP/JPY’s decline from 198.94 continues today and intraday bias remains on the downside. Deeper fall would be seen to 188.07 support. Firm break there will argue that corrective pattern from 180.00 has finished too, and larger decline from 208.09 might be ready to resume. On the upside, above 192.89 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 55 4H EMA (now at 195.22) holds.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.