Yen Gains BoJ Hike Speculations, Sterling Steady after Inflation Data, Dollar Awaits CPI – Action Forex

Yen’s recovery gained some momentum today on as speculation over an imminent BoJ rate hike. Governor Kazuo Ueda reinforced Deputy Governor Ryozo Himino’s earlier comments, suggesting that next week’s policy meeting could bring a shift in monetary policy. The unified tone from BoJ’s leadership is seen a calculated effort to prime markets for potential action.

Overnight index swaps now indicate a 68% probability of a BoJ rate hike in January, rising to 86% by March. Positive observations by BoJ’s regional branch managers on wages growth should have bolstered the confidence in BoJ’s readiness to act.

Despite this, uncertainty still lingers as BoJ policymakers await US President-elect Donald Trump’s inauguration speech early next week, which may provide more concrete insights into his trade and economic policies.

Meanwhile, Sterling is showing little reaction to inflation data released today. UK CPI reported revealed a marked slowdown in services inflation to 4.4%, its lowest level since March 2022. This has raised speculation of a BoE rate cut at its February meeting.

However, any optimism in the UK is tempered by lingering concerns over fiscal health and rising government borrowing costs. Market sentiment could deteriorate further if Thursday’s GDP data disappoints, compounding fears of a broader economic slowdown.

Overall in currency markets, Dollar has taken a step back, consolidating last week’s gains. Risk sentiment is somewhat buoyed by the absence of firm denial from Trump regarding proposals for gradual tariffs. Additionally, traders are awaiting today’s US CPI data, which could significantly impact expectations of Fed’s monetary policy over the course of 2025. For now, Dollar is the worst-performing currency this week, followed by Sterling and Swiss Franc. Conversely, New Zealand Dollar leads gains, followed by Australian Dollar and Euro. Canadian Dollar and Yen are trading in middle positions.

Technically, as Dollar is retreating, there are some support levels to pay attention to. The levels include 1.0435 resistance in EUR/USD, 1.2486 resistance in GBP/USD, 0.6301 resistance in AUD/USD and 0.9007 support in USD/CHF. As long as these levels hold, Dollar’s near term bullishness should be maintained in case of deeper pull back. As for USD/JPY, however, it’s likely moving on its own course based on expectations on BoJ rate hike next week.

UK CPI slows to 2.5% in Dec, services inflation down to 4.4%

UK CPI slowed from 2.6% yoy to 2.5% yoy in December, below expectation of 2.7% yoy. Core CPI slowed from 3.5% yoy to 3.2% yoy, below expectation of 3.4% yoy.

CPI goods annual rate rose from 0.4% yoy to 0.7% yoy, while CPI services annual rate fell from 5.0% yoy to 4.4% yoy.

On a monthly basis, CPI rose by 0.3% mom, below expectation of 0.4% mom.

ECB’s Lane expects service inflation to ease

ECB Chief Economist Philip Lane noted during an event today that services inflation will “come down quite a bit” in the coming months. He attributed much of the anticipated moderation to a slowdown in wage growth. Additionally, firms are reportedly experiencing reduced cost pressures, which should also contribute to easing price increases.

Lane highlighted the challenges of providing a definitive future path for interest rates, citing significant uncertainties in the global economic environment, including escalating trade tensions.

“From our point of view, saying here’s where we think the future rate path is going to be conveys a sense of certainty that we don’t feel,” Lane said, reinforcing the ECB’s cautious stance.

On the topic of exchange rates and their influence on prices, Lane pointed out that while movements in the euro-dollar exchange rate can impact European prices over time, the short-term relationship is less predictable. He noted that in the early stages of a significant currency shift, much of the impact is “absorbed by firms.

“The exchange rate, I think, over time plays a role,” Lane said. “But in terms of the month-by-month, quarter-by-quarter correlation between the exchange rate and import prices is not that stable.”

BoJ’s Ueda signals rate hike on the table next week

BoJ Governor Kazuo Ueda today provided further hints that the central bank may be considering a rate hike at its upcoming policy meeting.

Ueda noted, “We are currently analyzing data thoroughly and will compile the findings in our quarterly outlook report. Based on that, we will discuss whether to raise interest rates at next week’s policy meeting and would like to reach a decision.”

Ueda emphasized the significance of Japan’s wage outlook, which has recently been a key focus for policymakers. He pointed to encouraging signals from wage negotiations, which could bolster consumer spending and support BoJ’s inflation target.

Additionally, Ueda remarked that the economic policies of the incoming US administration, coupled with domestic wage trends, would play a pivotal role in determining the timing of any rate adjustment.

The governor’s remarks align closely with those of BoJ Deputy Governor Ryozo Himino, who earlier this week suggested that a rate hike was on the table.

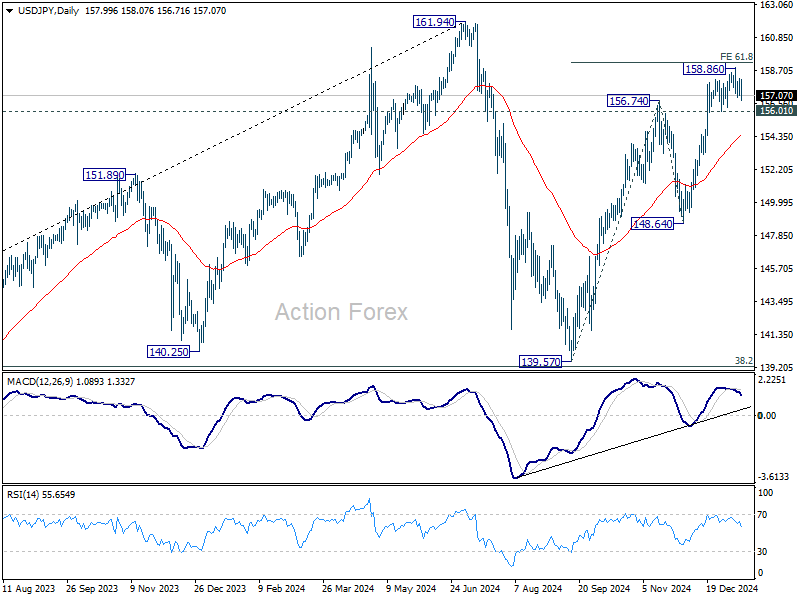

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.33; (P) 157.76; (R1) 158.41; More…

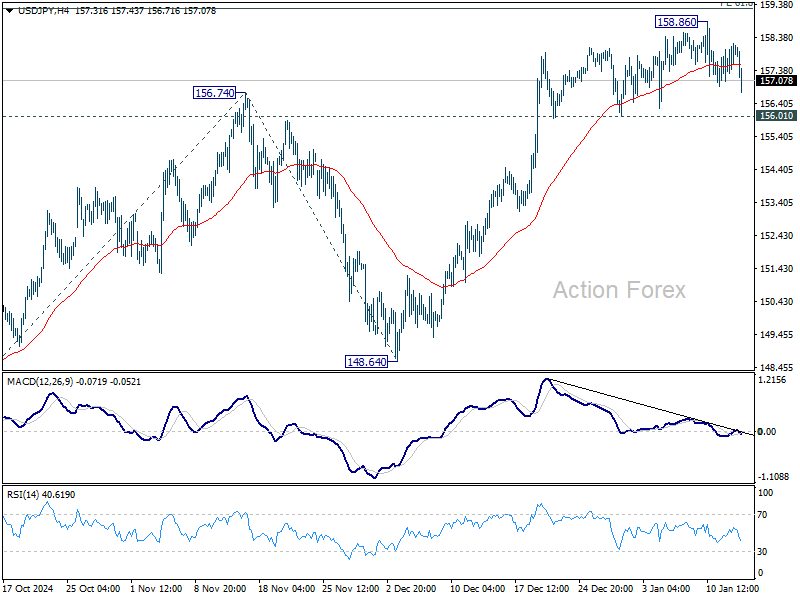

Intraday bias in USD/JPY remains neutral for the moment as sideway trading continues. Further rally is in favor as long as 156.0 support holds. On the upside, decisive break of 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 will extend the rally from 139.57 to retest 161.94 high. However, considering bearish divergence condition in 4H MACD, firm break of 156.01 support will confirm short term topping. Intraday bias will then be back on the downside for 55 D EMA (now at 154.46) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.