Cautious Trade Dominates as Dollar Holds Steady, Yen Leads, Gold Jumps – Action Forex

Activity in the forex markets has turned relatively subdued today, with no clear trend emerging as traders shift into a cautious stance. With no top-tier economic data scheduled for the rest of the week, attention is turning to the impending inauguration of US President-elect Donald Trump next Monday. The spotlight is squarely on his anticipated tariff policies, which could have profound implications for global trade and economic stability.

Yen holds its position as the strongest currency of the day, buoyed by increasing speculation of a potential rate hike from the Bank of Japan at its meeting next week. BoJ Governor Kazuo Ueda’s consistent messaging has reinforced market expectations, with traders pricing in a higher likelihood of policy tightening.

Swiss Franc ranks second best, benefiting from decline in European benchmark yields. Dollar is the third-best performer, continuing to consolidate against its peers. The greenback’s movements were unaffected by slightly worse-than-expected US jobless claims and retail sales data.

On the downside, New Zealand Dollar has overtaken Sterling as the weakest currency of the day. Pound remains under pressure following disappointing GDP data but has not faced aggressive selling. Meanwhile, Australian Dollar is the third weakest, while Euro and Canadian Dollar trade in mixed fashion.

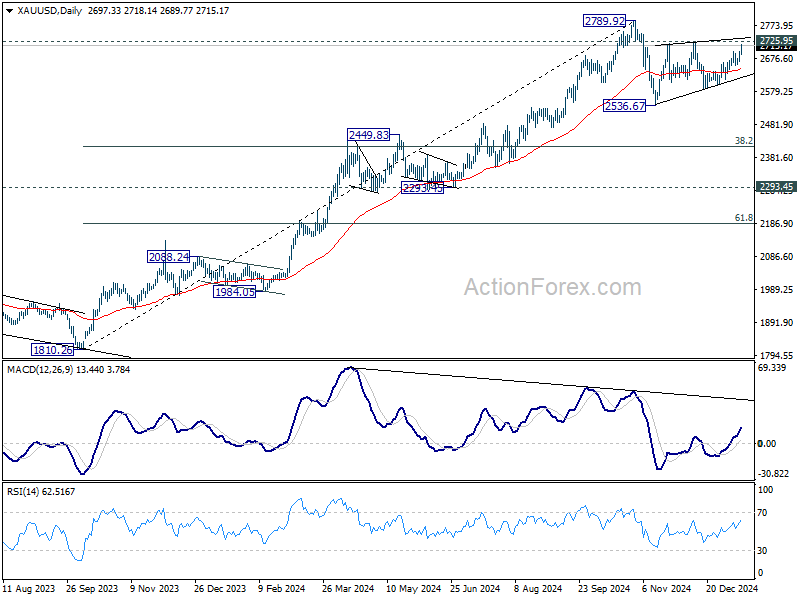

Technically, Gold’s rally this week suggests that choppy rebound from 2536.67 is actually still in progress. Further rise is now in favor through 2725.95 resistance in the near term. However, this rise is seen as the second leg of the corrective pattern from 2789.92. Hence, upside should be below this high. Break of 55 D EMA (now at 2643.87) will argue that the third leg has started to 2536.67 support and below.

US initial jobless claims falls to 217k vs exp 210k

US initial jobless claims rose 14k to 217k in the week ending January 11, above expectation of 210k. Four-week moving average of initial claims fell -750 to 213k.

Continuing claims fell -18k to 1859k in the week ending January 4. Four-week moving average of continuing claims fell -1k to 1867k.

US retail sales rise 0.4% mom in Dec, ex-auto sales up 0.4% mom

US retail sales rose 0.4% mom to USD 729.2B in December, below expectation of 0.5% mom. Ex-auto sales rose 0.4% mom to USD 586.3B, below expectation of 0.5% mom. Ex-gasoline sales rose 0.4% mom to USD 676.8B. Ex-auto & gasoline sales rose 0.4% mom to USD 533.9B.

Total sales for the October through December period were up 3.7% from the same period a year ago.

ECB Minutes: Gradual easing essential to monitor disinflation check points

ECB’s December 11–12 meeting minutes noted that while the 25 bps rate cut decided at the meeting was widely supported, some members argued for a more aggressive 50 bps reduction.

Some policymakers contended that a larger rate cut would have better addressed Eurozone’s weakening economic projections, with one noting that “successive projection exercises have shown increasing downside risks to growth.”

However, the majority concurred that a smaller, measured cut aligned with the “controlled pace of easing” and provided a “sense of the direction” of the path of interest rates.

The minutes emphasize while projections were conditional on a further rate cut in January, the meeting underscored that “data dependency precluded any foregone conclusions.”

The minutes also stated that the “measured pace of interest rate cuts” was essential to ensure that ECB could “pass critical checkpoints to verify disinflation remains on track.” Furthermore, it was highlighted that optionality must be preserved to address risks that could derail inflation stabilization, including geopolitical tensions, global trade disruptions, and energy price volatility.

Nevertheless, “if the baseline projection for inflation is confirmed over the next few months and quarters,” the minutes noted, a “gradual dialing back of policy restrictiveness” would be appropriate.

Eurozone goods exports fall -1.6% yoy in Nov, imports down -1.0% yoy

Eurozone goods exports fell -1.6% yoy to EUR 248.3B in November. Good imports fell -1.0% yoy to EUR 231.9B. Trade balanced showed a EUR 16.4B surplus. Intra-Eurozone trade fell -7.0% yoy to EUR 214.8B.

In seasonally adjusted term, goods exports rose 3.2% mom to EUR 240.6B.Goods imports rose 0.7% mom to EUR 227.8B. Trade balance widened from October’s EUR 7.0B to EUR 12.9B, larger than expectation of EUR 7.2B. Intra-Eurozone trade fell -1.7% mom to EUR 210.4B.

UK GDP grows only 0.1% mom in Nov, with mixed sector performance

UK’s economy posted modest growth in November, with GDP increasing by 0.1% mom, but slightly missing market expectations of 0.2%. Nevertheless, this marked a positive turnaround from the -0.1% mom contraction in October.

Sectoral performance was mixed, with services, the largest contributor to the economy, inching up by 0.1% mom, while production fell by -0.4% mom. Construction activity, however, provided a brighter spot, rising 0.4% mom during the month.

Despite November’s modest gains, the broader economic picture remains subdued. Over the three months to November 2024, real GDP showed no growth compared to the three months to August. Services, which account for a significant portion of the UK’s output, stagnated over this period. Production output contracted by -0.7%, offsetting the 0.2% growth seen in construction.

BoJ’s Ueda reiterates rate hike debate for next week’s policy meeting

BoJ Governor Kazuo Ueda indicated today, for the second time this week, that the central bank will “debate whether to raise interest rates” at its upcoming January 23-24 policy meeting. This marks the second time in this week that Ueda has emphasized

Ueda’s comments come as BoJ prepares its new quarterly economic report, which will serve as the basis for its policy decision. While the Governor has not committed to a specific outcome, the repeated message signals that a rate hike is a plausible scenario, barring any significant market shocks tied to the January 20 inauguration of U.S. President-elect Donald Trump.

Market sentiment, nevertheless, remains divided on the timing of the anticipated hike. A recent poll conducted between January 8-15 shows that 59 out of 61 economists expect BoJ to raise rates to 0.50% by the end of March. Yet, only 20 foresee the move occurring at this month’s meeting.

Japan’s PPI holds steady at 3.8% as import prices turn positive

Japan’s PPI held steady at 3.8% yoy in December, meeting market expectations and maintaining the previous month’s pace. Key drivers included a sharp 31.8% yoy rise in agricultural goods prices, fueled by soaring rice costs.

Energy costs also contributed significantly, with electric power, gas, and water prices climbing 12.9% year-on-year. This uptick comes as the government phases out subsidies designed to mitigate rising utility and gasoline prices.

Yen-based import prices turned positive, rising 1.0% yoy after three months of declines. While modest, this reversal underscores the lingering effects of Yen depreciation, which was recorded at -0.1% mom.

Australia’s employment grows 56.3k in Dec, showing continuous resilience

Australia’s labor market displayed resilience in December as employment surged by 56.3k, significantly exceeding expectations of a 15.0k increase. Number of unemployed people also rose by 10.3k, contributing to a slight uptick in the unemployment rate from 3.9% to 4.0%, in line with forecasts.

Participation rate climbed to a record high of 67.1%, up from 67.0%, reflecting an expanding labor force. Additionally, employment-to-population ratio rose by 0.1 percentage point to a new peak of 64.5%, showcasing the labor market’s capacity to absorb more workers. Monthly hours worked increased by 0.5% mom, equivalent to 10 million additional hours.

This data supports the view that the labor market’s earlier signs of easing have stabilized in the second half of 2024. Robust employment growth, consistent levels of average hours worked, and unchanged or lower levels of labor underutilization compared to a year ago affirm the ongoing strength of the job market.

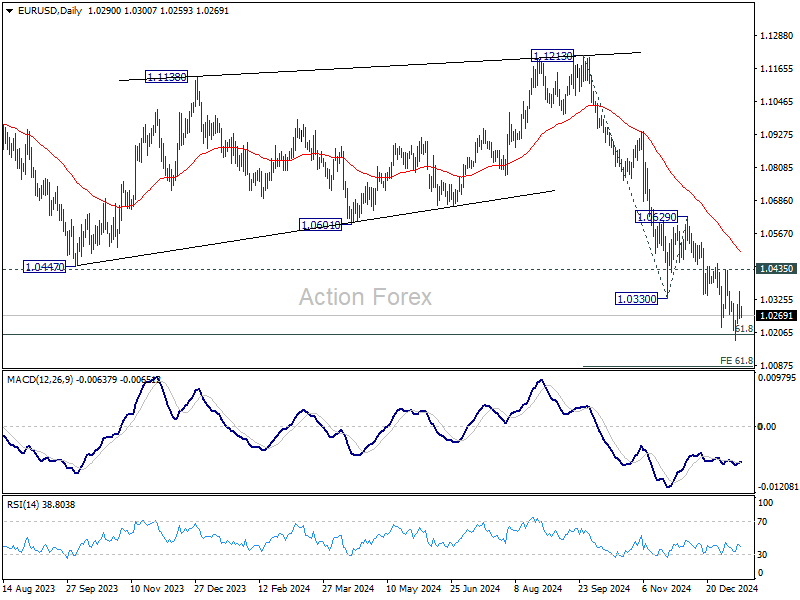

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0248; (P) 1.0302; (R1) 1.0344; More…

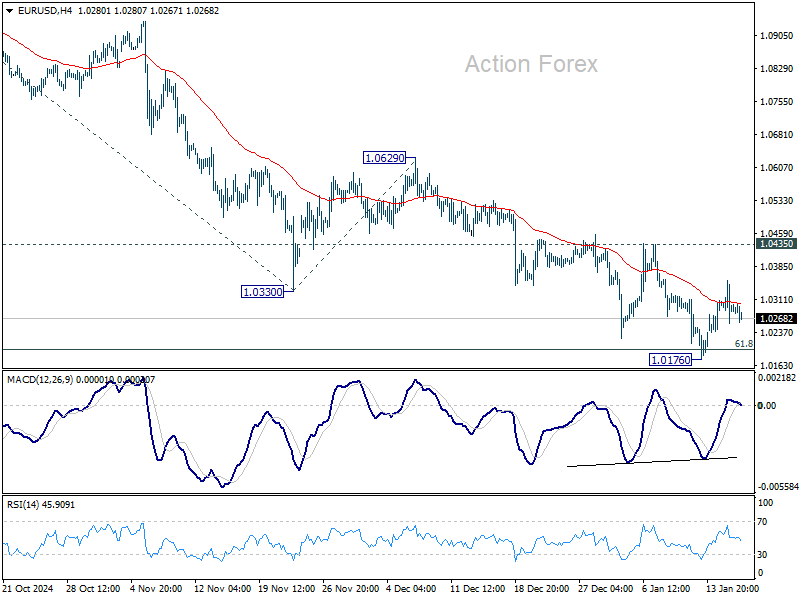

EUR/USD is still engaged in consolidations above 1.0176 and intraday bias stays neutral. With 1.0435 resistance intact, outlook remains bearish and further decline is expected. On the downside, break of 1.0176 will resume the fall from 1.1213 and target 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083. However, considering bullish convergence condition in 4H MACD, firm break of 1.0435 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.