Loonie on a Rollercoaster on Tariff Threats, Canadian CPI Watched – Action Forex

Canadian Dollar endured a rough ride, heavily influenced by US President Donald Trump’s tariff rhetoric. The Loonie initially gained some ground yesterday, as Dollar weakened broadly after Trump refrained from imposing immediate tariffs during his first day in office. However, optimism was short-lived as Trump warned of 25% tariffs on both Mexico and Canada starting February 1, citing border security concerns and labeling Canada a “very bad abuser.”

Trump’s remarks, made during a press briefing accompanying his wave of executive orders, have brought uncertainty back to the already fragile sentiment. In the background, BoC’s latest business outlook survey highlighted apprehension among Canadian businesses. Conducted during November 2024, the survey revealed that 40% of respondents expected negative effects from the new US administration, while one-third were uncertain about the fallout.

On the horizon, Canada’s December CPI report due today could trigger more volatility in Loonie. Both headline and core inflation are expected to ease further, reinforcing the case for another 25-bps rate cut at BoC’s January 29 meeting. Despite signaling a slower pace of monetary easing this year, BoC appears not ready for a pause yet. At least one more cut is generally expected, especially with inflation hovering near the 2% target.

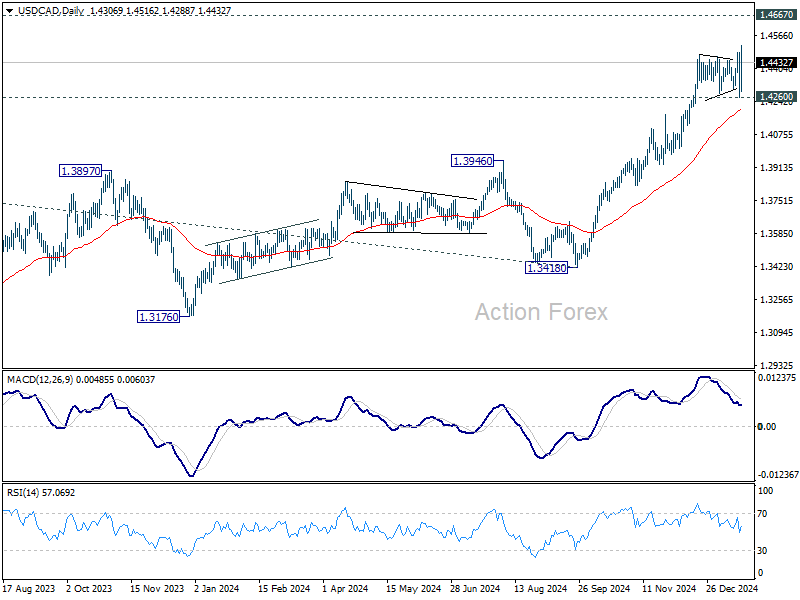

Technically for USD/CAD, near term bullishness was revived after yesterday’s huge volatility. For now, further rise is expected as long as 1.4260 support holds. Current rally should continue towards 1.4667 key long term resistance. Nevertheless, a firm break there might not happen until the tariff picture is cleared. For any dip, through 1.4260, the next level of defense would be 55 D EMA (now at 1.4203).

UK payrolled employment falls -47k in Dec, unemployment rate rises to 4.4% in Nov

UK payrolled employment fell -47k or -0.2% mom in December. Median monthly pay rose 5.6% yoy, down from 6.4% yoy in November and 7.9% yoy in October. Claimant count rose 0.7k, below expectation of 10.3k.

In the three months to November, unemployment rate ticked up to 4.4%, above expectation of 4.3%. Average earnings excluding bonus rose 5.6% yoy, up from 5.2% yoy, and above expectation of 5.5% yoy. Average earnings including bonus rose 5.6% yoy, up from 5.2% yoy, matched expectations.

NZ BNZ services fall to 47.9, contracts for 10th month

New Zealand’s BNZ Performance of Services Index declined from 49.1 to 47.9 in December, well below historical average of 53.1. This also marks the 10th consecutive month of contraction.

The breakdown of the data highlights broad weakness: activity/sales fell from 48.3 to 46.2, and supplier deliveries dropped sharply from 52.5 to 47.7. New orders/business remained stagnant at 49.5, just below the threshold for expansion, while employment showed a marginal improvement, rising from 46.7 to 47.4. Stocks/inventories also slipped into contraction territory, falling from 52.0 to 48.8.

Negative sentiment among respondents increased to 57.5% in December, up from 53.6% in November, with cost-of-living pressures and concerns about the general economic climate dominating feedback.

BNZ’s Senior Economist Doug Steel remarked, “Comparing across our key trading partners, New Zealand has the only PSI in contraction. Our neighbour Australia is the closest comparison, but their equivalent PSI is sitting more comfortably at 50.8.”

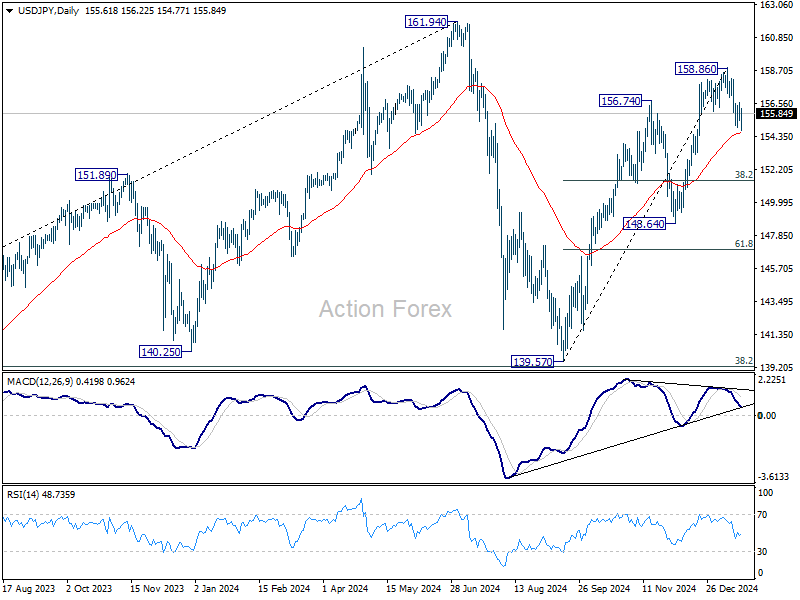

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.17; (P) 155.88; (R1) 156.33; More…

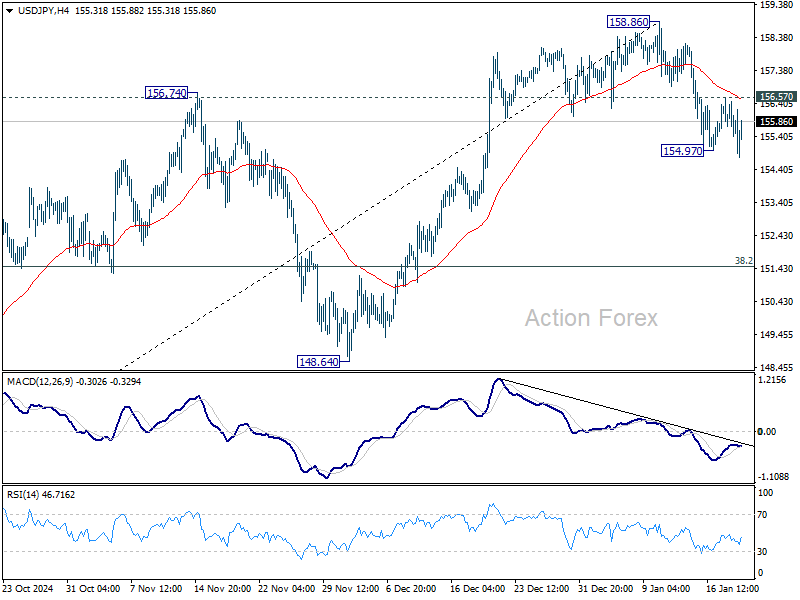

Intraday bias in USD/JPY is back on the downside with breach of 154.97 temporary low. Sustained break of 55 D EMA (now at 154.61) will extend the fall from 158.86 to 38.2% retracement of 139.57 to 158.86 at 151.49 next. Nevertheless, firm break of 156.67 resistance will argue that the pull back has completed, and turn bias back to the upside for retesting 158.86 high instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.