NASDAQ Slide Grabs Focus, Dimming Fed Spotlight to Start the Week – Action Forex

As markets gear up for a week dominated by central bank meetings including Fed and ECB, sharp selloff in US tech stocks has stolen the spotlight. NASDAQ futures dropped more than -2%, triggering mild safe-haven flows into Yen, U.S. Dollar, and Swiss franc. Meanwhile, commodity currencies like Aussie and Kiwi suffered as risk sentiment deteriorated.

At the heart of the tech pullback is chipmaker NVIDIA, which fell nearly -7%. This move followed news that a relatively unknown Chinese startup, DeepSeek, released an AI assistant rivaling ChatGPT, claiming to use lower-cost chips and minimal data. The implication is that the current bullish thesis on AI-related infrastructure—ranging from expensive high-performance semiconductors to expanded data center capacity—could face competition from leaner, lower cost solutions.

DeepSeek, operating out of Hangzhou, has generated significant buzz by topping Apple App Store’s free apps chart on Monday, surpassing well-established AI tools. The startup’s potentual remains uncertain, but the very notion that cutting-edge US technology could be challenged in China’s fast-evolving environment has unsettled investors. While it may be too soon to judge DeepSeek’s long-term impact, sentiment has clearly shifted, prompting a recalibration of risk assets and fueling a flight to safer currencies.

The tech rout has also hit the cryptocurrency market, with Bitcoin tumbling back below the 100k mark. Technically, the first line of defense is on rising 55 D EMA (now at 97282). Strong rebound from there will keep retain near term bullish momentum for resumption of long term up trend sooner rather than later. However, firm break of 55 D EMA will set up range trading between 89127/109571 for longer.

China’s PMI manufacturing falls to 49.1, weak start to 2025

China’s manufacturing activity slipped into contraction in January, with NBS Manufacturing PMI falling from 50.1 to 49.1, missing expectations of 50.1. This marks the first contraction since October and the lowest reading since August.

The decline was attributed to Lunar New Year holiday, as workers left early, according to NBS senior statistician Zhao Qinghe. Analysts also noted potential effects from slowing export demand after earlier front-loading tied to trade concerns.

The services sector showed similar weakness, with the Non-Manufacturing PMI dropping from 52.2 to 50.2, below the expected 52.0. Composite PMI, combining manufacturing and services, slipped to 50.1 from 52.2, reflecting a broad deceleration.

While some of this is likely seasonal, the magnitude of the slowdown raises concerns about underlying economic momentum, especially with external pressures like trade tensions still in play.

Three central banks, one busy week: Fed holds, BoC trims, ECB cuts

This week brings a trio of central bank decisions, with Fed, BoC, and ECB all set to reveal their latest policy moves. The consensus is that Fed will hold rates steady, BoC will deliver a smaller 25 bps cut, and ECB will maintain its gradual easing with another 25bps reduction. With a busy data docket also in play—featuring key GDP reports and inflation updates—traders will have a wealth of information to digest in a short span of time.

At Fed, there is a near-certainty of no change to its benchmark rate. Futures markets are pricing in 98% probability that FOMC will keep rates unchanged at 4.25–4.50%, pausing its easing cycle after a string of cuts in 2024. Given these odds, the chance of a surprise is minimal. Instead, the highlight will be the policy statement and Chair Jerome Powell’s press conference, regarding the rationale behind the hold.

Also, any clue regarding the length of this “pause” would likely move markets, especially given lingering questions about another possible cut in the first half of the year. Current pricing suggests around 72% chance that Fed will refrain from cutting at the next meeting in March as well. Still, around 70% chance is priced in for another 25bps reduction may occur during the first half of the year.

Beyond that, it may be too soon for Fed policymakers to give any guidance. More definitive signals about the path for the year might only emerge when the next set of dot plots and forecasts are released in March.

With Canadian inflation dipping to 1.8% in December, there is sufficient room for BoC to continue lowering rates. However, the current policy rate of 3.25%, before the cut, is now at the high end of the estimated neutral range of 2.25–3.25%. With that in mind, BoC should opt to proceed more cautiously with 25bps reduction.

The new Monetary Policy Report from BoC should offer fresh insights into the central bank’s updated economic outlook and rate path. The key questions focus on whether officials see a need to bring the policy rate below neutral to stimulative levels eventually—and if so, how quickly.

Over in Europe, ECB is firmly on track for another 25 bps cut to lower deposit rate to 2.75%. This approach is in line with President Christine Lagarde’s commitment to a “regular, gradual path” toward neutral, which she has previously identified in the 1.75–2.25% zone.

For the moment, ECB policymakers seem in harmony regarding the lack of need for rates to dip into stimulative territory. If the consensus holds, ECB could stop easing once it hits around 2% on the deposit rate, possibly between spring and summer. Nevertheless, the next opportunity for a more detailed forecast—including updated growth and inflation estimates—will likely come in March, which could be a pivotal moment for shaping expectations about future moves.

Beyond the trio of central bank meetings, the economic calendar is filled with significant releases. The US is set to unveil advance GDP figures, along with PCE inflation data. Eurozone’s GDP will be scrutinized for signs of stabilization. Germany’s Ifo business climate and GfK consumer sentiment surveys will also be important, as they may show whether Europe’s largest economy is ready to turn a corner. Australia’s CPI could sway RBA’s decision on whether to start cutting rates in February or wait until May. Canada’s own GDP figures round out the week.

Here are some highlights for the week:

- Monday: China NBS PMIs; German Ifo business climate; US new home sales.

- Tuesday: Japan corporate service price index; Australia NAB business confidence; US durable goods orders, house price index, consumer confidence.

- Wednesday: BoJ minutes, Japan consumer confidence; Australia CPI; Germany Gfk consumer sentiment; FOMC rate decision, US goods trade balance; BoC rate decisions.

- Thursday: New Zealand trade balance, ANZ business confidemce; Australia impor prices; Swiss trade balance, KOF economic barometer; Eurozone GDP flash, unemployment rate, ECB rate decision; US GDP advance, jobless claims.

- Friday: Japan Tokyo CPI, industrial production, retail sales, unemployment rate; Australia PPI; Germany CPI flash, unemployment rate; Swiss retail sales; Canada GDP; US personal income and spending, PCE inflation

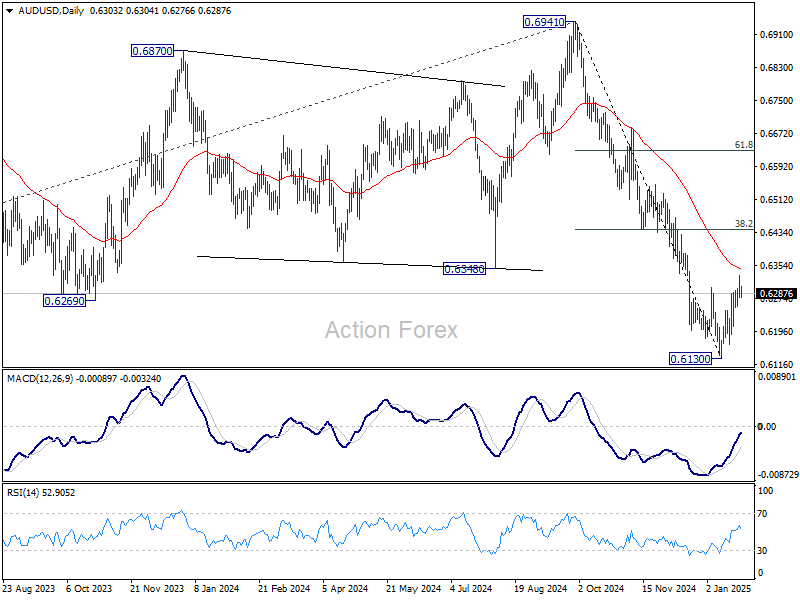

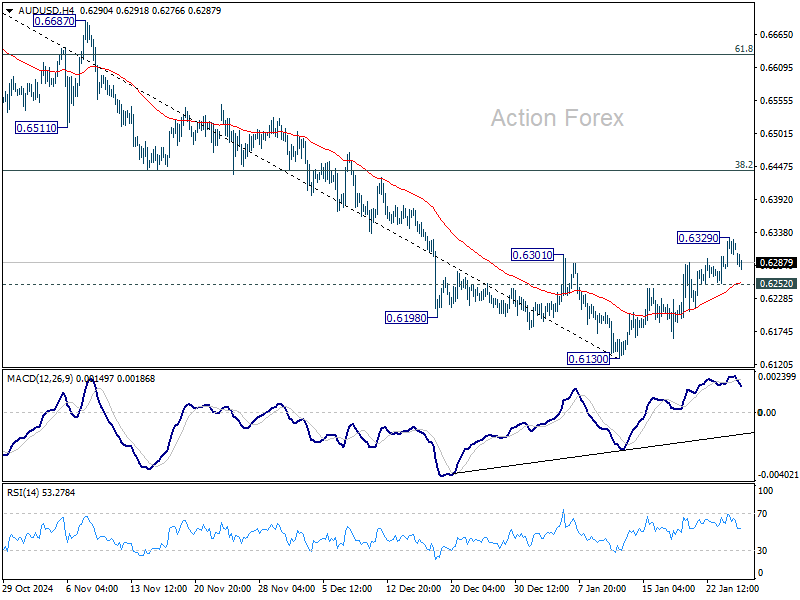

AUD/USD Daily Report

Daily Pivots: (S1) 0.6284; (P) 0.6308; (R1) 0.6336; More...

Intraday bias in AUD/USD is turned neutral first with today’s dip. Corrective rebound from 0.6130 could still extend through 0.6329 and 55 D EMA (now at 0.6347). But strong resistance is expected from 38.2% retracement of 0.6941 to 0.6130 at 0.6440 to limit upside to complete this corrective rebound. On the downside, break of 0.6252 minor support will turn bias back to the downside for retesting 0.6130 low.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6545) holds.