ECB Rate Cut Takes Center Stage, as FOMC Hold Triggers Minimal Reaction – Action Forex

FOMC rate decision and press conference yesterday proved to be a non-event. Dollar remained firm following the decision to keep interest rates unchanged at 4.25–4.50%. Fed Chair Jerome Powell reinforced a patient approach to policy adjustments, stating, “we do not need to be in a hurry to adjust our policy stance.” He also emphasized the risks of premature easing, warning that “reducing policy restraint too fast or too much could hinder progress on inflation.” His remarks reaffirmed expectations that Fed is unlikely to cut rates in the near term, with market pricing now assigning an 82% probability of another hold in March, up from 73% last week.

Meanwhile, US President Donald Trump renewed his criticism of Fed, accusing it of failing to manage inflation and misjudging bank regulations. Trump demanded last week that “interest rates drop immediately”. However, markets largely ignored his remarks, as Powell’s measured tone continues to shape expectations for a prolonged hold on interest rates.

Attention now turns to ECB as it concludes this week’s round of major central bank meetings. ECB is widely expected to continue its “regular, gradual” easing path by cutting the deposit rate by 25bps to 2.75%, moving closer to the estimated neutral range of 1.75–2.25%.

Market pricing suggests a terminal rate of around 2.00% by late spring or early summer, but ECB President Christine Lagarde is unlikely to provide a clear roadmap just yet. With uncertainty surrounding US trade policy and potential tariff escalations, Lagarde is expected to maintain a data-dependent stance rather than commit to a specific easing path.

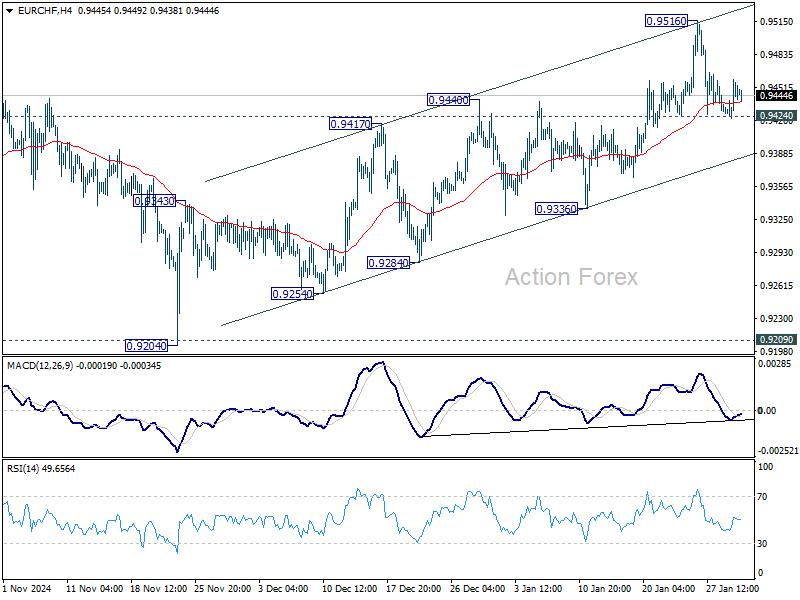

Technically, while EUR/CHF’s choppy rebound from 0.9204 extended last week, momentum continue to be unconvincing. It’s still more likely that not that this rebound is merely a corrective move. Firm break of 0.9242 support will be an early sign that this correction bounce has completed, and bring deeper fall to channel support (now at 0.9398) for more evidence.

Overall for the week so far, Yen is still the strongest, followed by Dollar, and then Swiss Franc. Aussie is staying at the bottom, followed by Kiwi, and then Loonie. Euro and Sterling are stuck in the middle.

Swiss KOF rises to 101.6, led by manufacturing and services

Switzerland’s KOF Economic Barometer climbed to 101.6 in January, up from 99.6 and surpassing market expectations of 100.5. This data suggests modest pickup in economic momentum, particularly in production-side sectors.

According to KOF, “the majority of the production-side indicator bundles included in the KOF Economic Barometer show positive developments.”

The strongest contributions came from manufacturing, financial and insurance services, hospitality, and other service industries, signaling resilience in key sectors of the Swiss economy.

However, the outlook remains uneven. While production indicators strengthened, demand-side indicators showed signs of weakness. KOF noted that both “the indicator bundles for foreign demand as well as for private consumption indicate a downward tendency,” highlighting subdued consumer activity and external trade concerns.

BoJ’s Himino reiterates further hike possible if economic forecasts hold

BoJ Deputy Governor Ryozo Himino reinforced expectations that the central bank could raise interest rates further if its economic and price projections are met.

Speaking today, Himino stated, “If our economic and price forecasts are achieved, we will raise our policy rate accordingly and adjust the degree of monetary support.”

Himino also highlighted concerns about Japan’s prolonged period of negative real interest rates, describing the situation as “not normal.”

He explained that an ideal economic scenario for Japan would involve rising wages and corporate profits, fueling stronger consumption and investment, which would then support moderate and stable inflation. In such a case, Japan could see real interest rates turn positive.

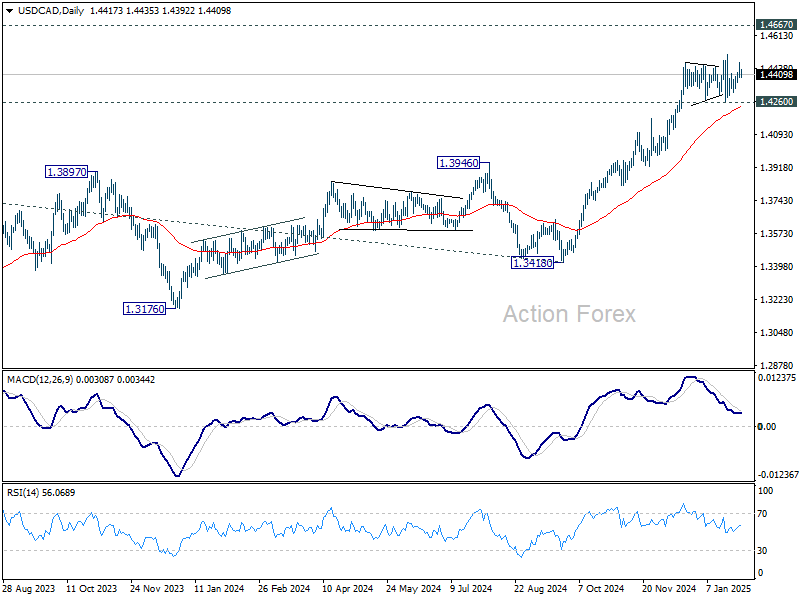

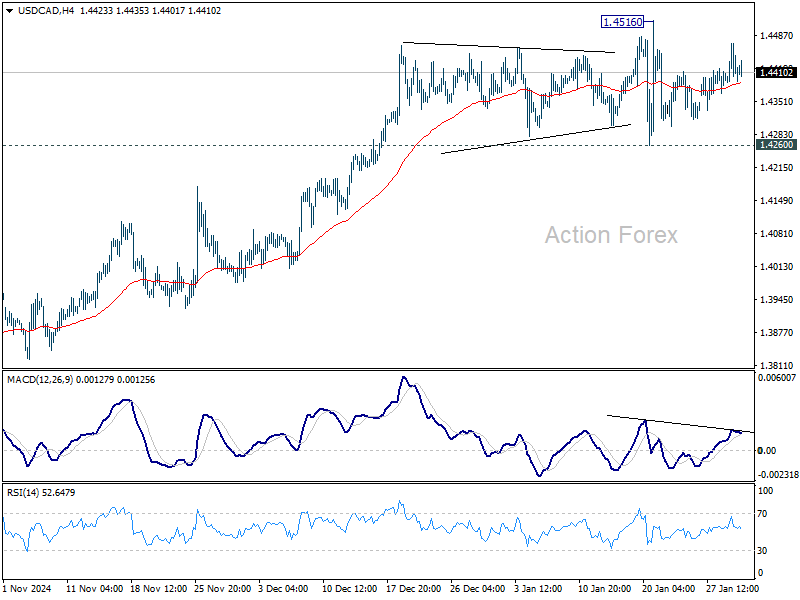

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4383; (P) 1.4427; (R1) 1.4465; More…

USD/CAD is still bounded in range trading below 1.4516 and intraday bias stays neutral. More consolidations would be seen, but further rally is expected as long as 1.4260 support holds. On the upside, firm break of 1.4516 will resume larger up trend to 1.4667/89 key resistance zone. Nevertheless, firm break of 1.4260 will turn bias to the downside for deeper pullback through 55 D EMA (now at 1.4241).

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Decisive break there will confirm long term up trend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.