Tariff Pause for Automakers Soothes Markets, Euro Stands Tall Ahead of ECB Cut – Action Forex

Risk sentiment is mildly positive in Asian session today, as investors digest the latest developments in US trade policy and Chinese economic measures. Markets welcomed the news that the US has granted a one-month exemption for imports from Mexico and Canada for auto makers. The decision came after US President Donald Trump met with executives from Ford, General Motors, and Stellantis, who urged him to delay the levies to avoid disruptions in the industry.

Meanwhile, Hong Kong stocks surged to a three-month high, with optimism fueled by hints from China’s National People’s Congress about looser monetary policies, along with expectations for further stimulus. Adding to the bullish momentum, tech giant Alibaba saw its stock soar after unveiling a new AI model, which it claims is competitive with DeepSeek, a major player in the artificial intelligence race. The rally in Chinese markets is adding to overall risk appetite in Asia, though uncertainties remain around US-China trade tensions.

In the currency markets, Euro continues to lead gains for the week as investors anticipate today’s ECB policy decision. The central bank is widely expected to deliver a 25-basis-point rate cut, but the outlook for further easing is more uncertain than ever. A trade war with the US is adding downside risks to growth, while Europe’s major economies are making historic shifts in fiscal policy, particularly in Germany, where new spending initiatives could support economic expansion. These conflicting factors make it challenging to predict ECB’s path beyond today’s meeting.

ECB President Christine Lagarde’s press conference is unlikely to provide strong forward guidance, as policymakers will want to maintain flexibility amid rising geopolitical and trade uncertainties. However, despite the upcoming rate cut, Euro’s rally looks well-supported in the near term, particularly as markets focus on Europe’s growing fiscal momentum and rearmament plans.

Sterling is the second strongest performer, followed by New Zealand Dollar. In contrast, Dollar remains at the bottom of the performance ladder, looking increasingly vulnerable ahead of tomorrow’s Non-Farm Payrolls report. Canadian Dollar is the second-worst performer of the week and Japanese Yen is also under pressure. Swiss Franc and Australian Dollar are positioned in the middle of the pack.

In Asia, at the time of writing, Nikkei is up 0.82%. Hong Kong HSI is up 3.03%. China Shanghai SSE is up 0.78%. Singapore Strait Times is up 0.72%. Japan 10-year JGB yield is up 0.053 at 1.499, hitting a 16-year high. Overnight, DOW rose 1.14%. S&P 500 rose 1.12%. NASDAQ rose 1.46%. 10-year yield rose 0.055 to 4.265.

ECB to cut rates, but trade war and fiscal shifts cloud outlook

ECB is widely expected to continue its “regular, gradual” easing cycle today, reducing the deposit rate by 25bps to 2.50%. Markets are still pricing in two more cuts this year, but the path forward has become murkier in light of recent geopolitical and economic shifts. Also, interest rates are approaching neutral levels, making further easing a more delicate decision.

On one hand, trade tensions with the US loom large, and the fallout from fresh tariffs and retaliatory measures could weigh on Eurozone’s already fragile economic recovery. On the other hand, the announcement of transformational fiscal changes in both Germany and at the European Commission level—aimed at boosting defense and infrastructure spending—could have a significant long-term impact on growth, partially offsetting the headwinds from a trade war.

ECB’s new economic projections, to be released alongside today’s decision, are expected to show weaker growth and marginally higher inflation. However, data collection for these forecasts took place weeks ago, rendering them less reflective of the rapidly evolving environment. Thus, their usefulness for predicting medium-term policy moves may be limited, with markets keeping an even closer eye on the ECB’s forward guidance instead.

Euro has been exceptionally strong this week, with recent optimism boosted by developments in European fiscal policy. It’s rally is unlikely to be deter by today’s ECB outcome.

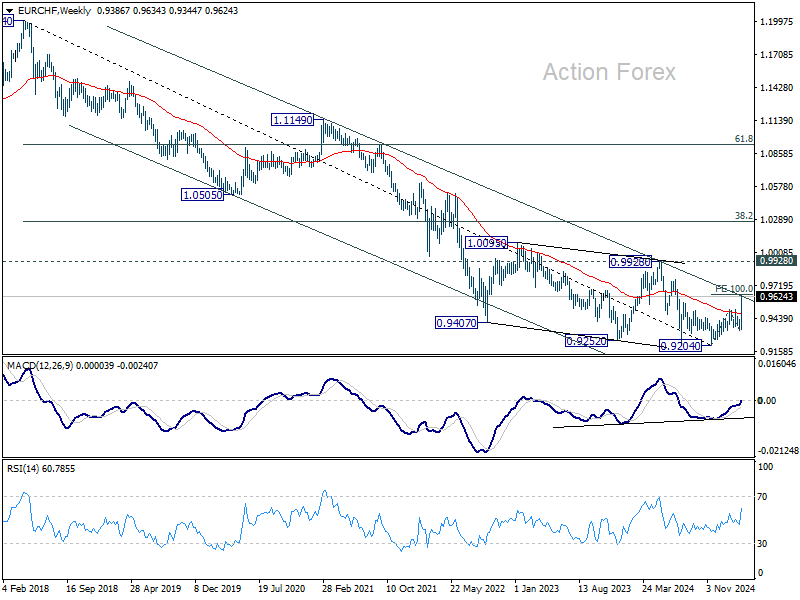

Technically, EUR/CHF has surged aggressively, now pressing long-term falling channel resistance (at around 0.9620), after decisively breaking above 55 W EMA. Sustained break above this resistance would suggest that the downtrend from 1.2004 (2018 high) has finally bottomed at 0.9204.

Sustained trading above the channel resistance will be argue that whole down trend from 1.2004 (2018 high) has completed at 0.9204, on bullish convergence condition in W MACD.

In this bullish case, further rise should be seen to 0.9928 structural resistance at least, with prospect of stronger rally, even still as a medium term corrective move.

Fed’s Beige Book: Modest growth, rising price pressures, and tariff concerns

Fed’s Beige Book report indicated that “economic activity rose slightly” since mid-January, with mixed regional performances. While four Districts saw modest or moderate growth, six reported no change, and two experienced slight contractions.

Consumer spending was generally lower, with essential goods seeing steady demand but discretionary spending weakening, particularly among lower-income consumers. However, business expectations remained “slightly optimistic” for the coming months.

On the labor front, employment “nudged slightly higher” overall, though wage growth slowed modestly compared to the previous report.

While price pressures remained moderate, several Districts noted an uptick in the pace of increase, particularly in manufacturing and construction. Many firms struggled to pass higher input costs onto customers, but expectations of tariffs on imports were already prompting preemptive price hikes in some sectors.

On the data front

Swiss unemployment rate, UK PMI construction and Eurozone retail sales will be released in European session. Later in the day, Canada will release trade balance and Ivey PMI. US will publish jobless claims, trade balance, and non-farm productivity.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0662; (P) 1.0729; (R1) 1.0857; More…

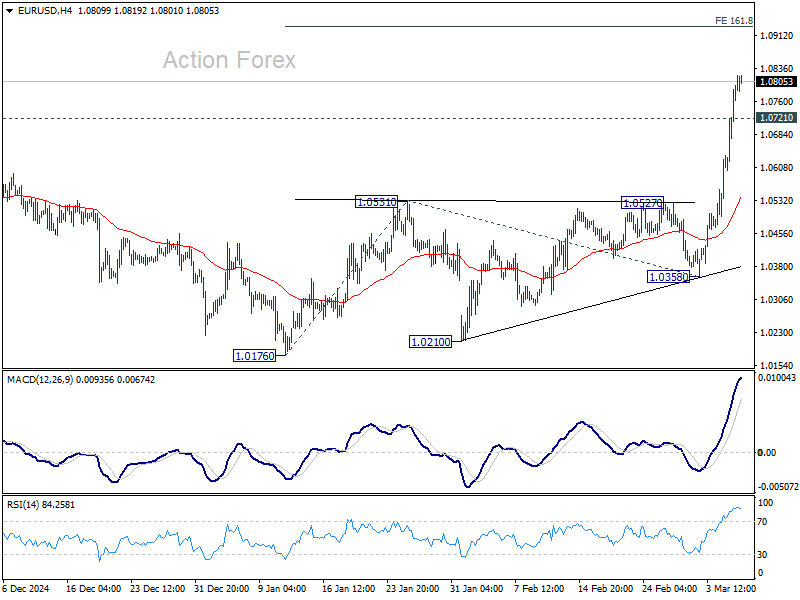

Intraday bias in EUR/USD remains on the upside as current rally from 1.0176 is still in progress. Next target is 161.8% projection of 1.0176 to 1.0531 from 1.0358 at 1.0932 On the downside, below 1.0721 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, the strong break of 55 W EMA (now at 1.0668) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. That came after drawing support from 0.9534 (2022 low) to 1.1274 at 1.0199. Rise from 0.9534 is still intact, and might be ready to resume through 1.1274. This will now be the favored case as long as 1.0531 resistance turned support holds.