Markets Soar on Tariff Truce, Reentry Signal or Perfect Exit Opportunity? – Action Forex

US stocks staged a powerful relief rally overnight, snapping back from the recent tariff-induced collapse. All three major indexes posted gains not seen in years, marking a dramatic reversal in sentiment. Yet, despite the scale of the rebound, it remains unclear whether this marks the beginning of genuine investor re-entry—or simply a massive short-covering rally triggered by a temporary policy U-turn.

What markets need now isn’t just a pause, but clarity and consistency. If the 90-day negotiation window devolves into more confusion, or if tariffs on China continue to escalate, the gains seen today could vanish just as quickly as they arrived.

The crux of the matter is whether yesterday’s rally represents just a reflexive bounce driven by short-covering and algorithmic momentum? With the market having been stretched to deeply oversold levels after recent collapse, the slightest spark was bound to trigger a sharp relief jump.

More improtantly, it is uncertain if long-term investors view this bounce as a reason to re-engage with US assets, or merely as an opportunity to exit at better levels. If the latter proves true, this rally could quickly fade into yet another bear market trap.

The catalyst behind the surge came from US President Donald Trump’s abrupt announcement that new 10% tariffs on most US trade partners—technically in effect just hours earlier—would be paused for 90 days to facilitate negotiations.

In contrast, the administration simultaneously escalated its economic conflict with China, announcing an immediate increase in tariffs on Chinese imports to 125%. The White House reinforced the pressure with a warning: “Do not retaliate and you will be rewarded.”

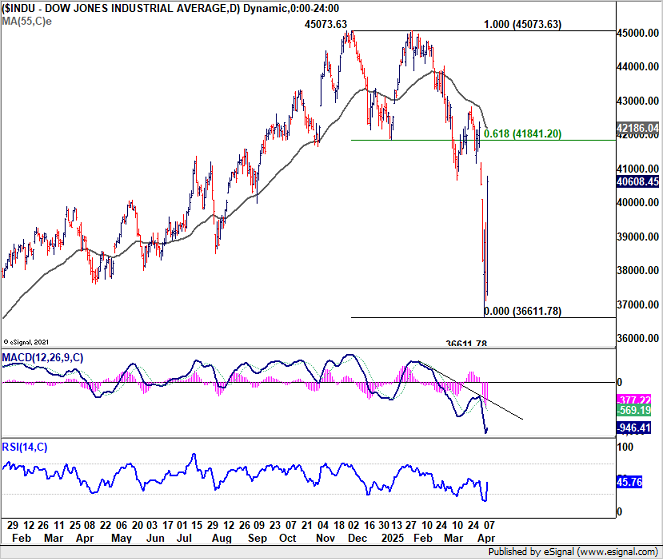

Technically, for DOW, this week’s low at 36,611.78 offers a potential base for near-term consolidation, especially given its proximity to 55 M EMA (now at 35595.76). However, any upside is likely to be capped by 61.8% retracement of 45073.63 to 36611.78 at 41841.20 to set the range for near term consolidations, well, probably for 90 days? Sustained break of 41841.20 is needed before declaring that this tariff crisis is over.

In the currency markets, after all the volatility, Aussie is currently the strongest one for the week so far, followed by Kiwi, and then Loonie. Sterling is the worst performer, followed by Dollar, and then Euro. Swiss Franc and Yen are positioning in the middle.

In Asia, at the time of writing, Nikkei is up 8.01%. Hong Kong HSI is up 1.96%. China Shanghai SSE is up 0.93%. Singapore Strait Times is up 5.73%. Japan 10-year JGB yield is up 0.045 at 1.327. Overnight, DOW rose 7.87%. S&P 500 rose 9.52%. NASDAQ rose 12.16%. 10-year yield rose 0.138 to 4.400.

Fed minutes highlight pre-tariff caution, hint at tough tradeoffs ahead

The minutes from the FOMC’s March meeting revealed growing concern among policymakers about the economic outlook, particularly amid rising uncertainty. While these discussions occurred before the dramatic escalation of the US tariff war in April, the insights remain valuable.

“Almost all” participants viewed inflation risks as tilted to the “upside”, while “downside” risks to employment and growth were also flagged—setting the stage for a policy dilemma.

Some officials highlighted that the Fed could soon face “difficult tradeoffs,” especially if inflation remains elevated while job and growth prospects deteriorate.

Notably, a few participants also warned that an “abrupt repricing of risk in financial markets” could magnify the impact of any negative economic shocks. Given what has since transpired with global markets in April, these comments seem prescient.

While the minutes may now appear somewhat outdated, they nonetheless provide a crucial baseline for understanding how the Fed might react in an increasingly fragile environment.

Japan’s PPI accelerates to 4.2% while import costs ease

Japan’s PPI rose 4.2% yoy in March, a slight acceleration from February’s 4.1% yoy and topping expectations of 3.9% yoy rise. The increase was broad-based, with notable gains in food prices, which rose 3.1% yoy, and energy costs, with petroleum and coal prices surging by 8.6% yoy.

Despite the uptick in domestic producer prices, import costs in Yen terms fell -2.2% yoy in March, extending the -0.9% decline in February. Export prices, however, rose a modest 0.3% yoy, slowing sharply from February’s 1.7% yoy growth.

China’s CPI falls -0.1% yoy in March, PPI highlights persistent deflationary pressures

China’s consumer inflation remained in negative territory for a second straight month in March, with CPI falling -0.1% yoy, missing expectations of 0.1% yoy increase. While the decline was narrower than February’s -0.7% yoy, it still reflects subdued demand pressures across the economy.

Food prices was a drag, down -1.4% yoy, while service prices provided only modest support, rising 0.3% yoy. Core CPI, which excludes volatile food and energy prices, edged up to 0.5% yoy from 0.3% previously, offering a slight glimmer of resilience.

However, with headline inflation still hovering around zero and signs of consumer caution persisting, the broader disinflation trend appears entrenched.

On a monthly basis, CPI dropped -0.4% mom, following February’s -0.2% mom decline, suggesting continued weakness in household spending momentum.

Meanwhile, producer prices extended their decline for a 30th straight month, with PPI dropping -2.5% yoy, deeper than the expected -2.3%.

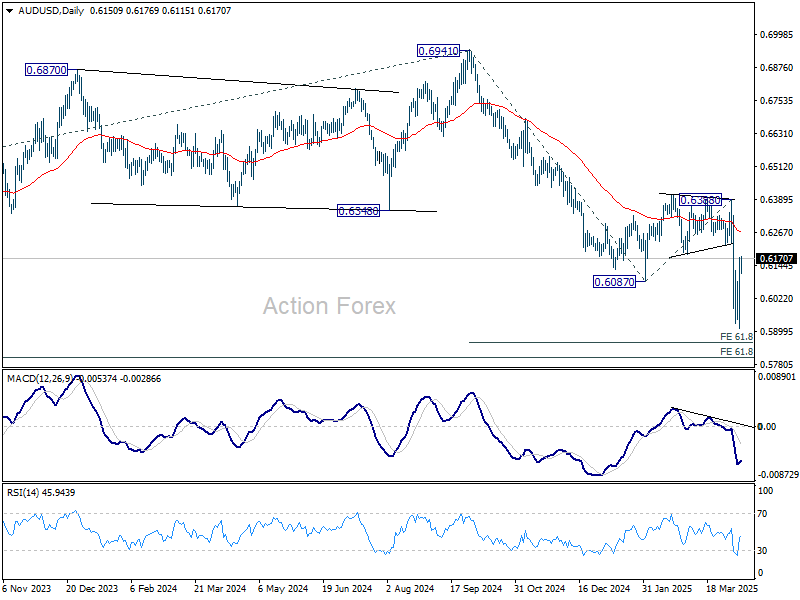

AUD/USD Daily Report

Daily Pivots: (S1) 0.5987; (P) 0.6081; (R1) 0.6249; More...

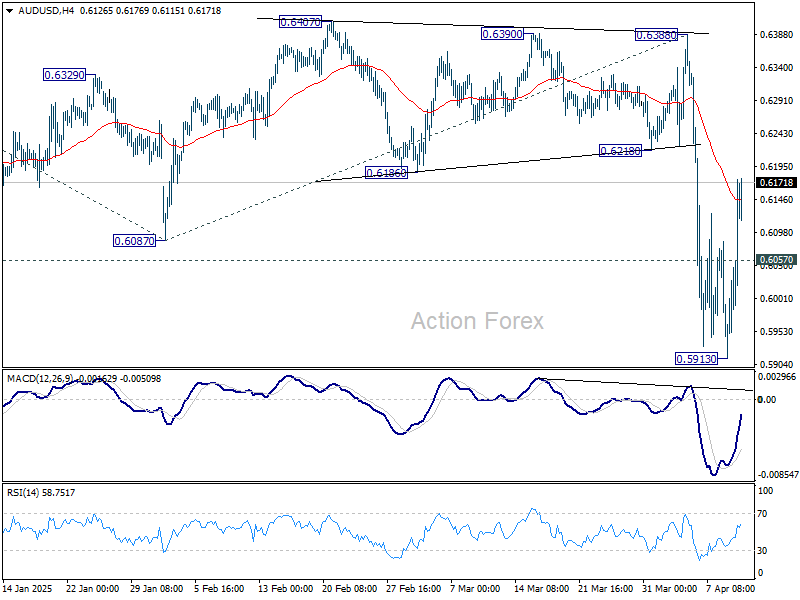

AUD/USD’s rebound from 0.5913 extended higher, and it’s now pressing 55 4H EMA (now at 0.6146). Sustained trading above there will should confirm short term bottoming,and bring stronger rebound towards 0.6388 resistance. Nevertheless, rejection by the EMA, followed by break of 0.6057 minor support will bring retest of 0.5913 low, and resumption of larger fall from 0.6941 at a later stage.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 0.6388 resistance holds.