Muted Markets Await ECB Cut, While US-Japan Trade Talks Show Tentative Progress – Action Forex

The forex markets held steady in tight ranges during Asian session, with investors treading cautiously ahead of the Easter long weekend. Market mood has been mildly lifted by signs of progress in US-Japan trade negotiations. In a surprise move, US President Donald Trump joined preliminary talks and later declared “Big Progress!” via social media, injecting some optimism into an otherwise quiet session.

While Trump’s gesture lifted sentiment briefly, Japanese Economy Minister Ryosei Akazawa remained measured, describing the meeting as a first step with a second round planned for later this month. He also confirmed that exchange rates were not part of the discussions, indicating Tokyo’s desire to keep talks focused on trade and investment.

Markets will now turn their attention to the ECB’s policy decision later today, where a 25bps cut in deposit rate to 2.25% is widely anticipated. The focus will be on ECB’s guidance and choice of language. In its last meeting, the Governing Council avoided declaring whether policy was still restrictive, and instead said it had become “meaningfully less restrictive”. This strategy is expected to continue, particularly as internal divisions within the ECB remain over forward guidance amid elevated uncertainty.

While some may hope for clearer signals on the future rate path, ECB is unlikely to oblige. According to the minutes of the previous meeting, several members stressed the need to avoid committing to even any directional bias on future moves. That caution is likely to persist, especially as external risks, including US trade actions and global demand uncertainty, still loom large. As a result, markets should expect a rate cut accompanied by continued strategic ambiguity.

Currency performance this week so far see Kiwi leads after stronger-than-expected CPI figures. Sterling follows as second despite mixed UK employment and inflation miss. Aussie is also holding firm even after weak job data. On the other side, Loonie is the weakest, with the BoC hold overnight failing to inspire confidence. Swiss Franc and Dollar are also underperforming, while Euro and Yen are trading in the middle.

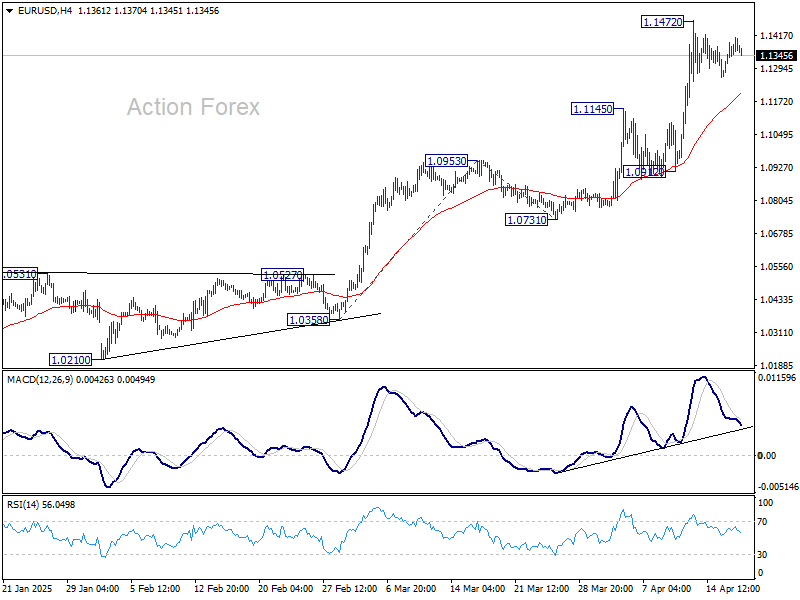

Technically, it looks like EUR/USD’s consolidation from 1.1472 is going to extend with another downleg. A dovish ECB outlook today could fuel some selloff. But downside should be contained by 1.1145 resistance turned support to bring rebound. Break of 1.1472 resistance is expected, to resume the larger up trend, after current consolidation completes.

In Asia, at the time of writing, Nikkei is up 1.01%. Hong Kong HSI is up 1.38%. China Shanghai SSE is down -0.03%. Singapore Strait Times is up 0.93%. Japan 10-year JGB yield is up 0.02 at 1.318. Overnight, DOW fell -1.73%. S&P 500 fell -2.24%. NASDAQ fell -3.07%. 10-year yield fell -0.044 to 4.279.

Fed’s Powell warns of dual-mandate tensions ahead

In a speech overnight, Fed Chair Jerome Powell pointed to substantial changes underway, by US administration, in trade, immigration, fiscal policy, and regulation—all of which are still “evolving” and difficult to assess in terms of economic impact.

In particular, Powell acknowledged that the scale of tariff increases already announced is “significantly larger than anticipated,” and warned that the resulting economic effects will likely include “higher inflation and slower growth.”

Powell noted a clear rise in near-term inflation expectations, with both market-based breakevens and survey indicators moving up in response to the new tariff regime. While long-term expectations remain largely anchored, he cautioned that the inflationary impulse from tariffs could prove “more persistent” than initially thought. In the near term, tariffs are highly likely to generate “at least a temporary rise in inflation” .

Importantly, Powell acknowledged that Fed could face a scenario where its “dual-mandate goals are in tension.” In such a case, policymakers would need to carefully weigh how far the economy is from each objective, and over what time horizons those gaps might close.

BoJ’s Nakagawa and Ueda highlight US tariff risk, urge vigilance

BoJ board member Junko Nakagawa cited US trade policy as one of the most significant risks to Japan’s economic outlook. In a speech, she noted that higher US tariffs could directly damage Japanese corporate activity, pressuring exports, production, sales, capital expenditure, and profitability.

Nakagawa also noted the potential for broader spillover effects, including weakened business and consumer sentiment and volatility in commodity prices and financial markets.

Echoing these concerns, BoJ Governor Kazuo Ueda told the parliament that uncertainty surrounding US policy, especially tariffs, has “heightened sharply” in recent weeks. Ueda stressed that the central bank will assess trade-related developments at each policy meeting without any pre-conception.

While reaffirming BoJ’s intention to raise interest rates if economic and price conditions align with projections, Ueda emphasized, “we must be vigilant to the fact uncertainty surrounding each country’s trade policy is heightening.”

Japan’s exports grow 3.9% yoy in March, imports up 2.0% yoy

Japan’s exports rose 3.9% yoy in March to JPY 9.85T, below the expected 4.5% yoy gain. Shipments to the US rose 3.1% yoy overall, boosted by strong gains in electronic parts (+35.8%), pharmaceuticals (+29.7%), and autos (+4.1%). However, this was offset by weakness in China, where exports fell -4.8% yoy.

On the import side, inbound shipments rose 2.0% yoy to JPY 9.30T , also falling short of the forecast 3.1% yoy. That resulted in trade surplus of JPY 544B.

In seasonally adjusted term, exports dropped -3.8% mom to JPY 9.31 trillion, while imports ticked up 0.6% mom, bringing the adjusted trade balance into a JPY -234B deficit.

Australia jobs rise 32.2k in March, misses expectations

Australia added 32.2k jobs in March, falling short of expectations for a 41.2k increase. The composition of gains was relatively balanced with 15k full-time and 17.2k part-time positions added.

Unemployment rate ticked up slightly to 4.1% from 4.0%, coming in better than the expected 4.2%. The modest rise in the jobless rate was largely due to a higher participation rate, which increased from 66.7 to 66.8%.

A potential sign of underlying weakness came from a -0.3% mom decline in total monthly hours worked, the second consecutive monthly drop. But that could be attributed partly to weather disruptions linked to ex-Tropical Cyclone Alfred.

NZ CPI surprises to the upside at 2.5% in Q1, domestic pressures driving

New Zealand’s consumer prices rose more than expected in the first quarter, with CPI climbing 0.9% qoq and accelerating from 2.2% yoy to 2.5% yoy, above forecasts of 0.7% qoq and 2.3% yoy.

Nevertheless, this still marks the third consecutive quarter that annual inflation has stayed within RBNZ’s 1–3% target band.

Tradeable inflation, reflecting imported price dynamics, rose 0.8% qoq and just 0.3% yoy, indicating limited external pricing pressure. In contrast, non-tradeable inflation, a proxy for domestic conditions, surged 1.1% qoq and 4.0% yoy.

The strength in non-tradeables points to robust local demand and ongoing cost pressures within the domestic economy.

Looking ahead

ECB rate decision is the main focus in European session. Later in the day, US will release jobless claims, Philly Fed survey, housing starts and building permits.

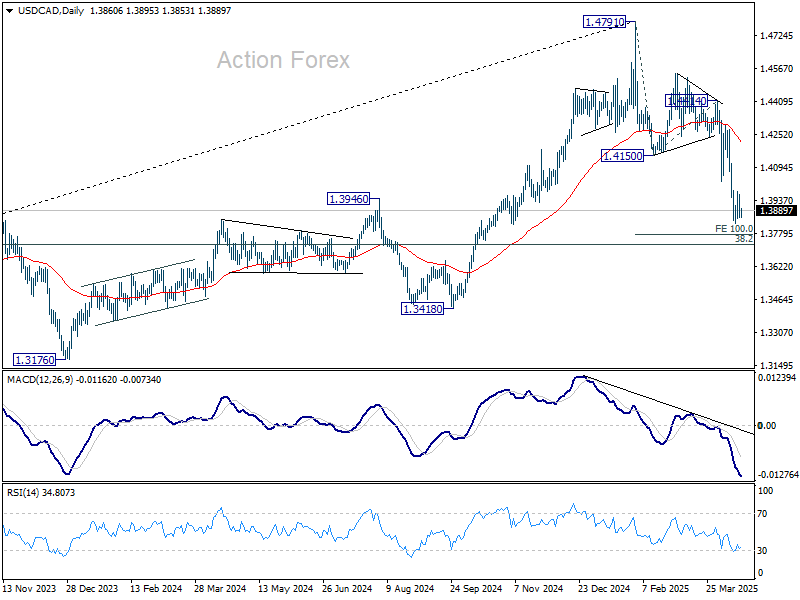

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3817; (P) 1.3896; (R1) 1.3936; More…

USD/CAD is still bounded in consolidations above 1.3827 and intraday bias remains neutral. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 1.4150 support turned resistance holds. On the downside, break of 1.3827 will resume the fall from 1.4791 to 100% projection of 1.4791 to 1.4150 from 1.4414 at 1.3773.

In the bigger picture, the break of 1.3976 resistance turned support (2022 high) and 55 W EMA (now at 1.3983) indicates that a medium term top is already in place at 1.4791. Fall from there would either be a correction to rise from 1.2005, or trend reversal. In either case, firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.