No Reaction to ECB Cut as Markets Drift in Pre-Holiday Lull – Action Forex

Trading in the forex markets remain calm, with little reaction to ECB’s widely anticipated 25bps rate cut. The move to lower its deposit rate to 2.25% was fully priced in. The central bank acknowledged that Eurozone growth prospects have deteriorated due to escalating global trade tensions, but this has long been embedded in market expectations. The absence of any forward guidance or new policy direction helped reinforce the market’s muted tone.

Indeed, the primary focus for investors remains the intensifying US trade war and its ripple effects on global economic sentiment. As markets break for the Easter weekend, investors are bracing for trade policy to return to center stage next week. The lack of clarity surrounding tariff policy and broader US trade strategy is increasingly weighing on corporate confidence. U.S. firms, in particular, are becoming more hesitant to invest or expand amid the shifting policy environment.

A Reuters poll conducted between April 14–17 illustrates the rising unease. The probability of a US recession within the next 12 months surged to 45%, up sharply from 25% in March and marking the highest reading since December 2023. All 45 economists who responded to a related question said that tariffs have negatively affected business sentiment, with nearly half describing the impact as “very negative.”

At the same time, economists are scaling up their inflation forecasts. Expectations for headline CPI, core CPI, PCE, and core PCE have all been revised higher, with all measures now projected to remain above Fed’s 2% target through at least 2027. A majority of economists—62 out of 101 surveyed—expect the Fed to hold its benchmark interest rate steady at 4.25%-4.50% until at least July.

In terms of currency performance, Kiwi continues to lead the pack this week while Aussie and Sterling follow. At the other end, Swiss Franc is the weakest, trailed by the Euro and Loonie. Dollar and Yen are trading in the middle of the pack.

In Europe at the time of writing, FTSE is down -0.38%. DAX is down -0.44%. CAC is down -0.74%. UK 10-year yield is down -0.03 at 4.579. Germany 10-year yield is down -0.03 at 2.482. Earlier in Asia, Nikkei rose 1.35%. Hong Kong HSI rose 1.61%. China Shanghai SSE rose 0.13%. Singapore Strait Times rose 1.58%. Japan 10-year JGB yield rose 0.015 to 1.312.

US initial jobless claims fall to 215k, vs exp 224k

US initial jobless claims fell -9k to 215k in the week ending April 12, below expectation of 224k. Four-week moving average of initial claims fell -2.5k to 221k.

Continuing claims rose 41k to 1885k in the week ending April 5. Four-week moving average of continuing claims rose 1k to 1867k.

ECB cuts rates to 2.25%, drops “restrictive” language amid mounting uncertainty

ECB cut its deposit rate by 25 bps points to 2.25% as widely expected, but the more notable shift came in the tone of its accompanying statement. ECB completely removed the reference to its policy stance being “restrictive,” a phrase that had previously signaled a bias toward further monetary easing.

This change suggests policymakers believe the easing campaign has brought rates closer to neutral territory. The central bank emphasized that it will maintain a data-dependent, meeting-by-meeting approach and is “not pre-committing to a particular rate path” given the exceptional levels of uncertainty.

ECB noted that disinflation process remains “well on track,” with both headline and core inflation continuing to decline in line with forecasts. Importantly, services inflation—previously a key sticking point—has also “eased markedly” in recent months.

However, the central bank also highlighted growing downside risks to the economic outlook. ECB acknowledged that rising global trade tensions have begun to weigh on business and household confidence. The resulting volatility in financial markets is already tightening financing conditions and could further dampen activity in the Eurozone.

BoJ’s Nakagawa and Ueda highlight US tariff risk, urge vigilance

BoJ board member Junko Nakagawa cited US trade policy as one of the most significant risks to Japan’s economic outlook. In a speech, she noted that higher US tariffs could directly damage Japanese corporate activity, pressuring exports, production, sales, capital expenditure, and profitability.

Nakagawa also noted the potential for broader spillover effects, including weakened business and consumer sentiment and volatility in commodity prices and financial markets.

Echoing these concerns, BoJ Governor Kazuo Ueda told the parliament that uncertainty surrounding US policy, especially tariffs, has “heightened sharply” in recent weeks. Ueda stressed that the central bank will assess trade-related developments at each policy meeting without any pre-conception.

While reaffirming BoJ’s intention to raise interest rates if economic and price conditions align with projections, Ueda emphasized, “we must be vigilant to the fact uncertainty surrounding each country’s trade policy is heightening.”

Japan’s exports grow 3.9% yoy in March, imports up 2.0% yoy

Japan’s exports rose 3.9% yoy in March to JPY 9.85T, below the expected 4.5% yoy gain. Shipments to the US rose 3.1% yoy overall, boosted by strong gains in electronic parts (+35.8%), pharmaceuticals (+29.7%), and autos (+4.1%). However, this was offset by weakness in China, where exports fell -4.8% yoy.

On the import side, inbound shipments rose 2.0% yoy to JPY 9.30T , also falling short of the forecast 3.1% yoy. That resulted in trade surplus of JPY 544B.

In seasonally adjusted term, exports dropped -3.8% mom to JPY 9.31 trillion, while imports ticked up 0.6% mom, bringing the adjusted trade balance into a JPY -234B deficit.

Australia jobs rise 32.2k in March, misses expectations

Australia added 32.2k jobs in March, falling short of expectations for a 41.2k increase. The composition of gains was relatively balanced with 15k full-time and 17.2k part-time positions added.

Unemployment rate ticked up slightly to 4.1% from 4.0%, coming in better than the expected 4.2%. The modest rise in the jobless rate was largely due to a higher participation rate, which increased from 66.7 to 66.8%.

A potential sign of underlying weakness came from a -0.3% mom decline in total monthly hours worked, the second consecutive monthly drop. But that could be attributed partly to weather disruptions linked to ex-Tropical Cyclone Alfred.

NZ CPI surprises to the upside at 2.5% in Q1, domestic pressures driving

New Zealand’s consumer prices rose more than expected in the first quarter, with CPI climbing 0.9% qoq and accelerating from 2.2% yoy to 2.5% yoy, above forecasts of 0.7% qoq and 2.3% yoy.

Nevertheless, this still marks the third consecutive quarter that annual inflation has stayed within RBNZ’s 1–3% target band.

Tradeable inflation, reflecting imported price dynamics, rose 0.8% qoq and just 0.3% yoy, indicating limited external pricing pressure. In contrast, non-tradeable inflation, a proxy for domestic conditions, surged 1.1% qoq and 4.0% yoy.

The strength in non-tradeables points to robust local demand and ongoing cost pressures within the domestic economy.

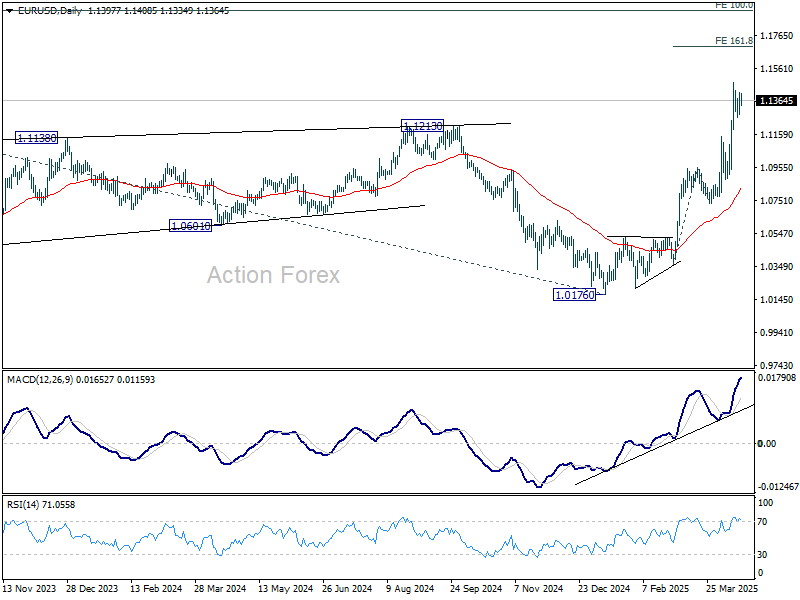

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1314; (P) 1.1363; (R1) 1.1449; More…

EUR/USD is still bounded in consolidation below 1.1472 and intraday bias remains neutral. Deeper retreat cannot be ruled out. But downside should be contained by 1.1145 resistance turned support to bring another rally. On the upside, break of 1.1472 will target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0745) holds.