Subdued Start to a Heavy Data Week with Risk Sentiment Holding Steady – Action Forex

Trading was particularly subdued today, even by the quiet standards of a typical Monday in Asia. That’s not surprising, given the near-empty economic calendar offering little to move the markets. Instead, traders are exercising understandable caution ahead of a heavy barrage of important data releases later this week, including US and Eurozone GDP figures, inflation reports from the US, Eurozone, and Australia, and the US non-farm payrolls report.

Now that the peak of the tariff shock appears to have passed, at least for this current wave, the market’s attention is shifting toward how these escalations are starting to materialize in hard economic data. Early indications from global PMIs and corporate earnings have been mixed, but this week’s heavyweight releases will offer more definitive evidence. For now, the overall market mood remains cautiously optimistic, and there is still room for a further rebound in risk assets if the incoming data holds up or surprises to the upside.

Meanwhile, Yen will also be a major focus this week with BoJ’s rate decision and new economic projections due. Yen has softened notably since last week as risk appetite improved globally. Speculation is also building that BoJ might delay its next rate hike in response to tariff-induced uncertainties. Should the BoJ’s updated projections lean dovish, Yen could face another leg of weakness against its major counterparts.

Technically, USD/JPY’s recovery from the short-term bottom at 139.87 remains in favor as long as 142.26 minor support holds. However, the broader near-term outlook stays bearish unless the pair can break decisively above 38.2% retracement of 158.86 to 139.87 at 147.12. Failure to do so, followed by break back below 142.26, would argue that the recovery is a corrective move, and bring retest of 139.87 next.

In Asia, at the time of writing, Nikkei is up 0.43%. Hong Kong HSI is up 0.07%. China Shanghai SSE is down -0.03%. Singapore Strait Times is down -0.43%. Japan 10-year JGB yield is down -0.017 at 1.323.

Japan denies report of US preference for weaker Dollar and stronger Yen

Japanese officials moved swiftly to deny a media report suggesting that US Treasury Secretary Scott Bessent had conveyed a preference for a weaker Dollar and stronger Yen during recent bilateral meetings in Washington last week.

Japan’s top currency diplomat, Atsushi Mimura, emphasized to reporters that “the US side did not touch upon exchange-rate targets” in discussions between Finance Minister Katsunobu Kato and his US counterpart.

Finance Minister Kato also reiterated via social media that exchange-rate frameworks were not discussed, directly refuting the report published by the Yomiuri newspaper.

Meanwhile, Bessent himself described the talks with Japan as “very constructive” in a post on X, noting that they covered reciprocal trade issues and “matters pertaining to exchange rates” without mentioning any explicit preferences.

China reaffirms growth target, holds back on major stimulus

China pledged its full confidence in achieving this year’s growth target of around 5%, vowing to implement timely and multiple support measures as the country is now in full-fledged trade war with the US. However, no major stimulus was announced immediately, giving the impression that Beijing is not in a rush to roll out large-scale interventions. Authorities appear inclined to first monitor the trade shock’s timing and magnitude before deciding on more aggressive measures.

Zhao Chenxin, deputy head of the National Development and Reform Commission, stressed at a press conference today that China retains “ample policy reserves and plenty of policy space,” and highlighted plans to stabilize employment and strengthen public employment services.

At a Politburo meeting chaired by President Xi Jinping last week, officials called for a “timely reduction” in interest rates and reserve requirement ratios to support the economy. Additional measures to aid struggling businesses, boost consumption among middle- and lower-income groups, and promote further development in technology and artificial intelligence were also emphasized.

As a touch of optimism, official data released over the weekend showed China’s industrial profits returning to growth in the first quarter. Cumulative profits rose 0.8% yoy to CNY 1.5T, reversing a -0.3% decline seen in the first two months.

High-stakes week ahead

It’s shaping up to be an extremely busy week for global markets, even though Monday’s economic calendar is near-empty. The action will pick up quickly, with BoJ rate decision and BoC summary of deliberations. Meanwhile, high-profile data releases include US GDP, PCE inflation, non-farm payrolls; Eurozone GDP and CPI’ Australia’s CPI; Canada’s GDP; and China’s PMIs.

Starting with BoJ, the central bank is widely expected to leave its short-term policy rate unchanged at 0.50% during this week’s meeting. According to a recent Reuters poll, only about half of economists still expect a hike to 0.75% in Q3, a notable drop from the 70% figure recorded in March. Market pricing now sees about a 65% chance of a 25bps hike by year-end.

The impact of Trump’s tariffs has made Japan’s economic outlook highly uncertain, particularly with manufacturing earnings expected to deteriorate. As a result, BoJ is likely to delay any further rate hikes, and is set to lower its economic growth forecast in the upcoming quarterly outlook. Nevertheless, BoJ is still expected to signal that rising wages and gradually firming inflation trends remain intact, keeping the door open for tightening when conditions allow.

From the US, a barrage of key releases will take center stage: the advance estimate of Q1 GDP, PCE inflation report, ISM manufacturing, and the all-important April non-farm payrolls. Fed officials have recently made it clear that May is too early for any rate cut, but there are increasing signs that attention is shifting back toward the employment side of the dual mandate. Should the labor market show signs of unexpected weakness, the probability of a Fed rate cut in June — currently hovering around 65% — could firm up sharply.

Turning to the Eurozone, flash GDP and CPI figures will be pivotal. Reports suggest a growing consensus within the ECB for another rate cut in June. Relief comes from the observation that the inflationary shock from US tariffs has been relatively muted, with Euro’s appreciation and weakening growth dynamics exerting deflationary pressure.

However, the durability of this trend is still in question. If Eurozone core inflation shows signs of re-acceleration, it could complicate ECB’s easing plans. Hence, this week’s CPI data will be crucial in either validating or challenging the market’s current expectation for further ECB easing.

In Australia, sentiment is shifting toward an imminent rate cut by RBA. Recent data have underwhelmed, with wage growth missing RBA’s own projections and consumption proving softer than expected. Coupled with lingering global trade uncertainties, particularly between the US and China, the case for another RBA rate cut to cushion the economy has strengthened considerably. Unless Australia’s Q1 CPI report delivers a major upside surprise this week, the market is likely to fully price in a rate cut at the May meeting.

Here are some highlights for the week:

- Tuesday: Germany Gfk consumer sentiment; Eurozone M3 money supply; US goods trade balance, house price index, consumer confidence.

- Tuesday: Japan industrial production, retail sales, housing starts; New Zealand ANZ business confidence; Australia quarterly CPI; China officials PMIs, Caixin PMI manufacturing; Eurozone GDP flash; Swiss KOF economic barometer; US ADP employment, GDP advance, Chicago PMI; personal income and spending, PCE inflation; Canada GDP, BoC summary of deliberations.

- Thursday: Japan PMI manufacturing final, consumer confidence, BoJ rate decision; Australia trade balance, import prices; Swiss retail sales; UK PMI manufacturing final, M4 money supply, mortgage approvals; US jobless claims, PMI manufacturing final, ISM manufacturing, construction spending; Canada PMI manufacturing.

- Friday: Japan unemployment rate, monetary base; Australia retail sales, PPI; Swiss PMI manufacturing; Eurozone PMI manufacturing final, CPI flash, unemployment rate; US non-farm payroll, factory orders.

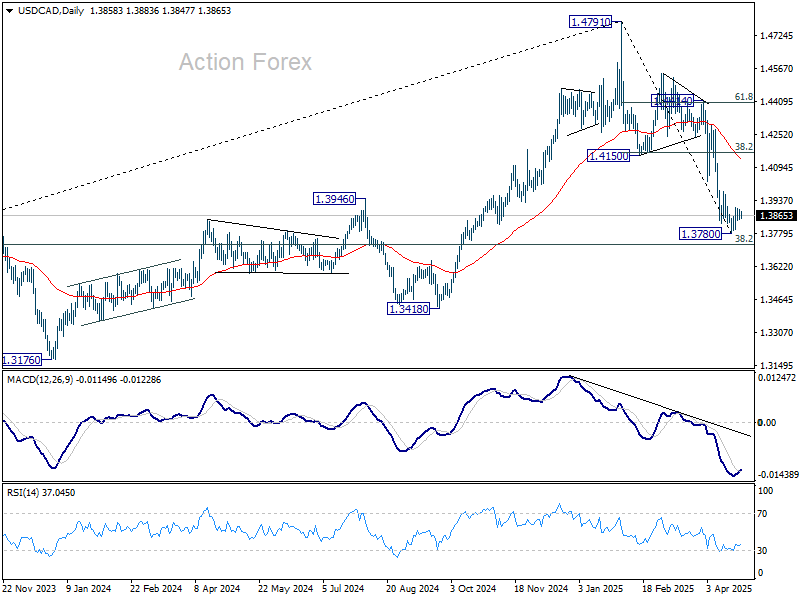

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3833; (P) 1.3863; (R1) 1.3883; More…

Further recovery remains mildly in favor in USD/CAD despite some loss of upside momentum as seen in 4H MACD. Still, even in case of another rise, upside should be limited by 1.4150 support turned resistance (38.2% retracement of 1.4791 to 1.3780 at 1.4166). On the downside, firm break of 1.3780 short term bottom will resume the whole fall from 1.4791.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.