Markets Steady as Trade Headlines Stir Little Reaction – Action Forex

Global trading remains subdued, with Japanese markets closed for Showa holiday and investors showing little urgency to take new positions. Canadian dollar saw some choppiness following election results, where the ruling Liberal Party retained power but fell short of a parliamentary majority. Despite the initial volatility, Loonie remained largely range-bound. Broader price action across currency markets has been lackluster, with traders largely holding off on bold moves ahead of major economic data releases later in the week.

Trade tensions continue to dominate headlines, though markets appear largely desensitized for now. Even news that the Trump administration is preparing to soften the impact of auto tariffs generated minimal reaction. According to reports, the White House plans to reduce the burden on domestic automakers by easing tariffs on imported parts and preventing overlapping duties on finished vehicles, particularly steel and aluminum. Refunds for tariffs already paid are also expected. A White House official confirmed the details, saying a formal announcement would come Tuesday.

The geopolitical side of trade is also evolving. Foreign ministers from the BRICS countries met to discuss a coordinated response to the latest wave of US tariffs. China, having faced the most severe hit with 145% tariffs on its exports to the US, pushed for a more confrontational stance. However, the final communique is expected to strike a critical yet restrained tone, signaling frustration without escalating tensions further.

Markets will keep an eye on today’s consumer sentiment releases from Germany and the US, although any impact may be fleeting. The next focus is on tomorrow’s releases of Eurozone and US GDP figures. With recession concerns resurfacing globally, these numbers could shape expectations for the next moves Fed and ECB.

In terms of currency performance so far this week, Yen leads the pack, followed by Sterling and Swiss Franc. At the other end, Kiwi has reversed to become the weakest performer, trailed by Loonie and Dollar. Euro and Aussie are holding to middle ground.

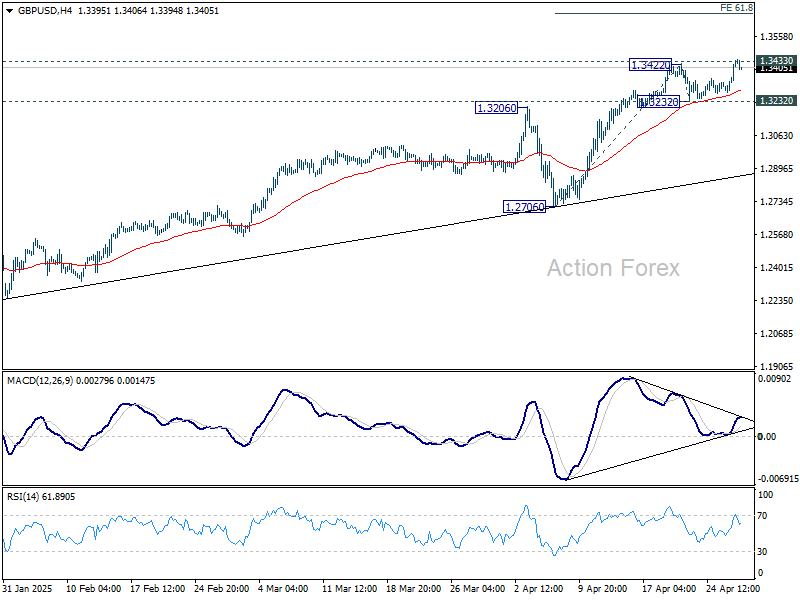

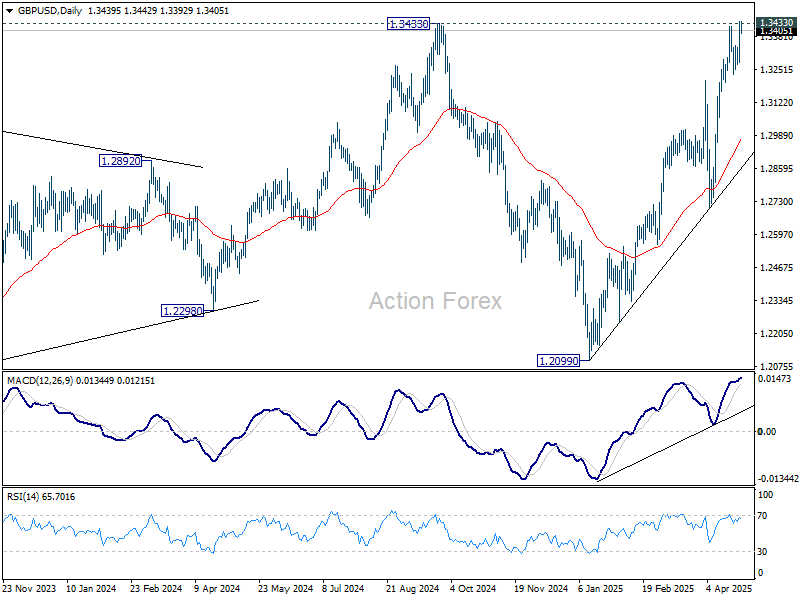

Technically, GBP/USD’s breach of 1.3433 (2024 high) suggests that up trend from 1.0351 (2022 low) is trying to resume. Sustained trading above 1.3433 will confirm this bullish case. Next near term target will be 61.8% projection of 1.2706 to 1.3422 from 1.3232 at 1.3674. However, break of 1.3232 support will indicate rejection from 1.3433, and bring deeper decline back to 55 D EMA (now at 1.2978) and possibly below.

In Asia, Japan is on holiday. At the time of writing, Hong Kong HSI is up 0.11%. China Shanghai SSE is down -0.13%. Singapore Strait Times is up 0.20%. Overnight, DOW rose 0.28%. S&P 500 rose 0.06%. NASDAQ fell -0.10%. 10-year yield fell -0.050 to 4.216.

RBA’s Kent highlights surge in FX volatility, stresses importance of market standards

In a speech today, RBA Assistant Governor Christopher Kent noted that early April saw some of the most extreme movements outside of the global financial crisis. He highlighted that Australian Dollar fluctuated within a range of 4 US cents and at one point suffered a 4.5% daily decline against the greenback — an unusually large move.

Kent also pointed out that broader measures of FX volatility, such as those derived from options markets, spiked to levels last seen during the pandemic, with liquidity conditions deteriorating noticeably.

While market conditions have calmed somewhat in recent days, Kent emphasized that such episodes serve as a reminder of the crucial role played by the Foreign Exchange Global Code.

He stressed that in periods of heightened uncertainty, the Code’s standardized practices and commitment to transparency help maintain trust between participants and ensure smoother market functioning even amid significant economic shocks.

Canadian Dollar steady as Liberals projected to retain power, but lack majority

Canadian Dollar remained steady following the country’s general election, with only a brief uptick in volatility as early results began to unfold. The ruling Liberal Party, led by Prime Minister Mark Carney, is projected to retain power. But the lack of clarity over whether they will secure a majority quickly tempered any bullish reaction in the Loonie.

With the Liberals leading in 156 districts versus the Conservatives’ 145, the party still falls short of the 172 seats needed for a majority in the 343-seat House of Commons.

Carney’s leadership, a former head of both BoC and BoE, is seen as a sign of stability for the country, offering some reassurance to investors. However, his tougher stance toward the US over tariffs suggests that trade relationship could face renewed challenges in the months ahead, with more difficult negotiations expected.

Technically, USD/CAD is still extending the consolidations from 1.3780 short term bottom. Another bounce could be seen through 1.3903 minor resistance. But upside should be limited by 1.4150 support turned resistance (38.2% retracement of 1.4791 to 1.3780 at 1.4166). Fall from 1.4791 is expected to resume at a later stage.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6389; (P) 0.6412; (R1) 0.6456; More...

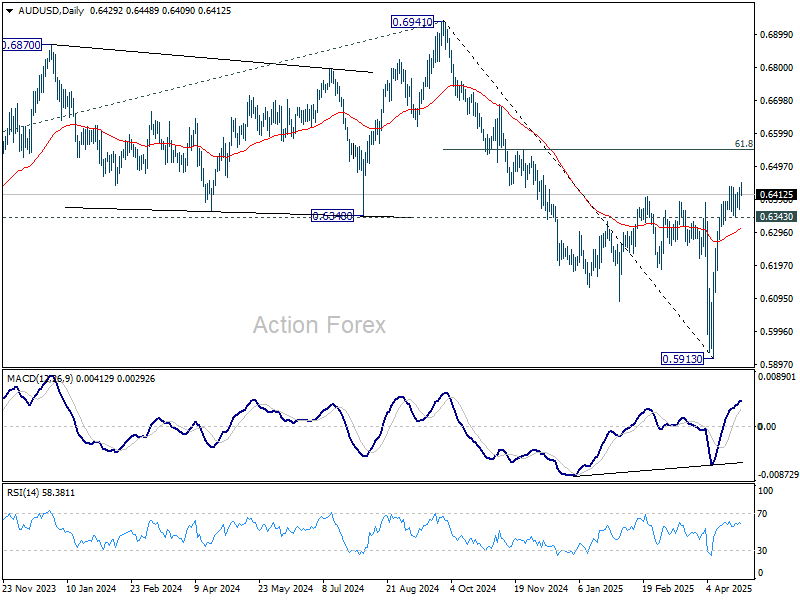

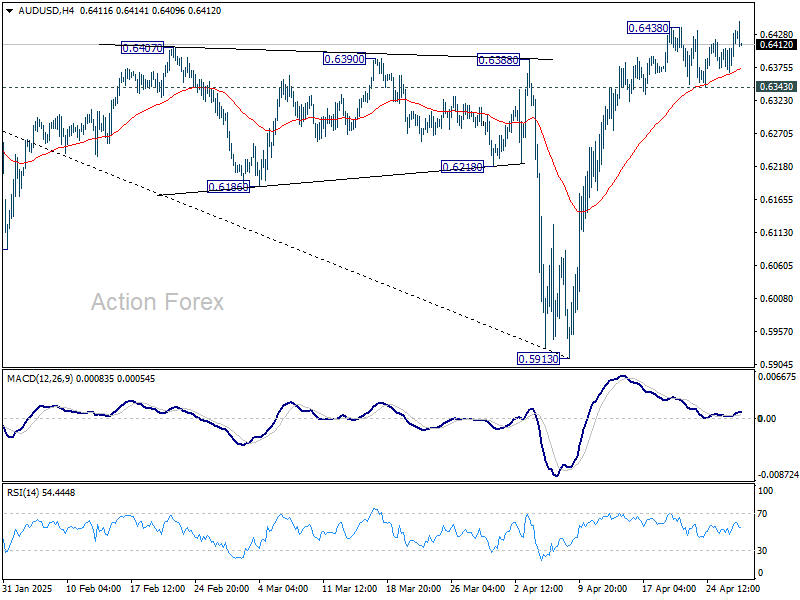

Intraday bias in AUD/USD is back on the upside with breach of 0.6438. Rise from 0.5913 should be resuming for 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, firm break of 0.6343 support will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 0.6310) and below.

In the bigger picture, as long as 55 W EMA (now at 0.6440) holds, the down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.