Markets Ignores Trade News Ahead of Data Barrage; Aussie Outperforms – Action Forex

Global financial markets are largely steady ahead of a packed economic calendar, with traders bracing for volatility as Eurozone and US GDP figures, as well as US PCE inflation data, are due shortly. Despite negative signals from China’s latest PMI reports, and another round of trade headlines, market reactions remain muted.

Risk sentiment is cautiously tilted to the positive side, reflected in the stronger performance of commodity-linked currencies like Australian, New Zealand, and Canadian Dollars. But major moves have yet to materialize. Euro, Sterling, and Yen are on the softer side, while Dollar and Swiss Franc are mixed.

Trade developments, which dominated headlines in recent weeks, offered some positive news but failed to stir markets significantly. US President Donald Trump signed a set of executive orders to ease the impact of automotive tariffs, including provisions for credits and relief on other levies. Commerce Secretary Howard Lutnick hinted at a breakthrough with one country to permanently remove reciprocal tariffs, though withheld specifics.

In Australia, Q1 CPI report slightly exceeded expectations on the headline but failed to derail market conviction on RBA policy. Crucially, the trimmed mean CPI—a preferred core measure—returned to within the RBA’s 2–3% target band for the first time since 2021. Services disinflation has also progressed notably. These trends, coupled with a slowing economic backdrop, have cemented expectations for a 25bps rate cut in May.

Nevertheless, RBA’s path of easing is likely to remain steady and measured. Unless there is a material deterioration in the global or domestic outlook, the central bank is expected to proceed with one cut per quarter.

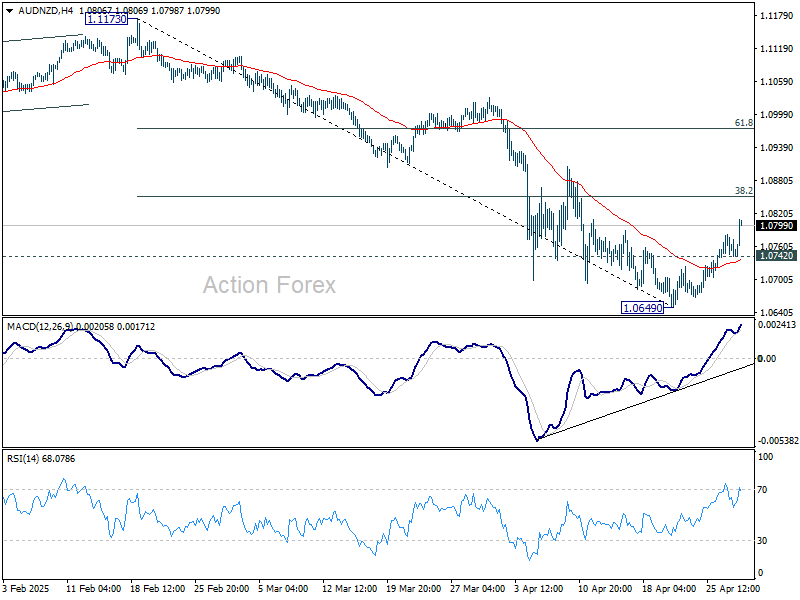

Technically, AUD/NZD is extending the rebound from 1.0649 short term bottom today. Nevertheless, this rally is currently seen as a corrective move only. Hence, upside should be limited by 38.2% retracement of 1.1173 to 1.0649 at 1.0849. Break of 1.0742 minor support will turn bias back to the downside for retesting 1.0649, and possibly resuming larger fall. However, firm break of 1.0849 will raise the chance of near term bullish reversal, and target 61.8% retracement at 1.0973 next.

In Asia, at the time of writing, Nikkei is up 0.30%. Hong Kong HSI is up 0.37%. China Shanghai SSE is down -0.09%. Singapore Strait Times is up 0.44%. Japan 10-year JGB yield is down -0.006 at 1.309. Overnight, DOW rose 0.75%. S&P 500 rose 0.58%. NASDAQ rose 0.55%. 10-year yield fell -0.043 to 4.173.

Looking ahead, Eurozone GDP is the main focus in European session. Later in the day, Canada GDP will be a feature today. But most attention would be on US ADP employment, Q1 GDP dance, March personal income and spending, and PCE inflation.

Australia’s trimmed mean CPI returns to RBA’s target band, services inflation eases further

Australia’s headline CPI was unchanged at 2.4% yoy in Q1, above expectations of a slight decline to 2.2% yoy. On a quarterly basis, CPI rose 0.9% qoq, also exceeding forecast of 0.8% qoq.

The closely watched trimmed mean CPI, a core inflation gauge, slowed from 3.3% yoy to 2.9% yoy , falling back within RBA’s 2–3% target range for the first time since 2021, in line with market expectations. However, the quarterly increase of 0.7% qoq was a touch higher than the anticipated 0.6% qoq.

Annual goods inflation accelerated from 0.8% yoy to 1.3% yoy, driven by a notable rebound in electricity prices. Services inflation eased from 4.3% yoy to 3.7% yoy, its lowest since mid-2022, amid broad-based moderation in rent and insurance costs.

NZ ANZ business confidence falls to 49.3, inflation expectations steady

New Zealand’s ANZ Business Confidence fell sharply in April, dropping from 57.5 to 49.3. The own activity outlook also edged lower from 48.6 to 47.7.

ANZ noted the decline may reflect growing apprehension over the global economic outlook, particularly uncertainty stemming from the escalating US-China trade war and broader policy unpredictability from the US administration.

Cost expectations three months ahead surged from 74.1 to 77.9, the highest level since September 2023. This contrasts with a slight dip in pricing intentions, which eased from 51.3 to 49.4. Inflation expectations one year out remained largely steady at 2.65%.

Japan’s industrial output slides -1.1% mom on auto weakness

Japan’s industrial production fell by -1.1% mom in March, significantly worse than the anticipated -0.7% mom decline.

According to the Ministry of Economy, Trade and Industry, the sharp drop was led by a -5.9% mom fall in motor vehicle output. Notably, regular passenger car production slipped -4.1% mom due to weaker export demand, while small vehicle output plunged -23.2% mom, reflecting disruptions in auto parts supply chains.

The slump in production comes against the backdrop of rising trade tensions, with US President Donald Trump imposing a 25% tariff on car and truck imports and a sweeping 24% tariff on all Japanese goods, later temporarily reduced to 10%.

Japanese manufacturers surveyed by METI project a recovery ahead, with output expected to rise 1.3% mom in April and 3.9% mom in May. But ministry officials remain cautious. “The environment surrounding production remains highly uncertain,” a METI representative warned, adding that manufacturers are clearly worried about the impact of US tariffs, though no changes to production plans have been formally announced yet.

Also released, retail sales rose 3.1% yoy in March, below expectations of 3.6%. Still, the result marks the 37th consecutive month of gains, indicating that domestic consumption has yet to show significant signs of stress.

China’s factory activity slumps on trade conflicts, optimism near record lows

China’s factory activity slumped sharply in April as official NBS Manufacturing PMI dropped from 50.5 to 49.0, its lowest level since December 2023 and below expectations of 49.9. Non-manufacturing PMI also weakened from 50.8 to 50.4.

The decline points to early signs of strain from escalating trade tensions, with NBS citing “sharp changes in the external environment” as a key driver.

Private-sector data painted a similarly cautious picture. Caixin Manufacturing PMI dropped to 50.4, its lowest in three months and just narrowly remaining in expansion.

Caixin’s Senior Economist Wang Zhe noted that while production and demand grew modestly, the pace has slowed and forward-looking optimism weakened significantly—plunging to the third-lowest level ever recorded. Trade-related uncertainty was a key concern for firms, weighing heavily on sentiment despite hopes for more policy support.

The April PMIs point to early-stage fallout from the China-US tariff standoff. Businesses are already reporting shrinking employment, delayed logistics, and inventory drawdowns. With both consumer and business confidence faltering, the government faces growing pressure to deploy stimulus measures. Unless domestic demand recovers and external risks subside, China’s economy could face more headwinds in Q2 and beyond.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.39; (P) 190.87; (R1) 191.34; More…

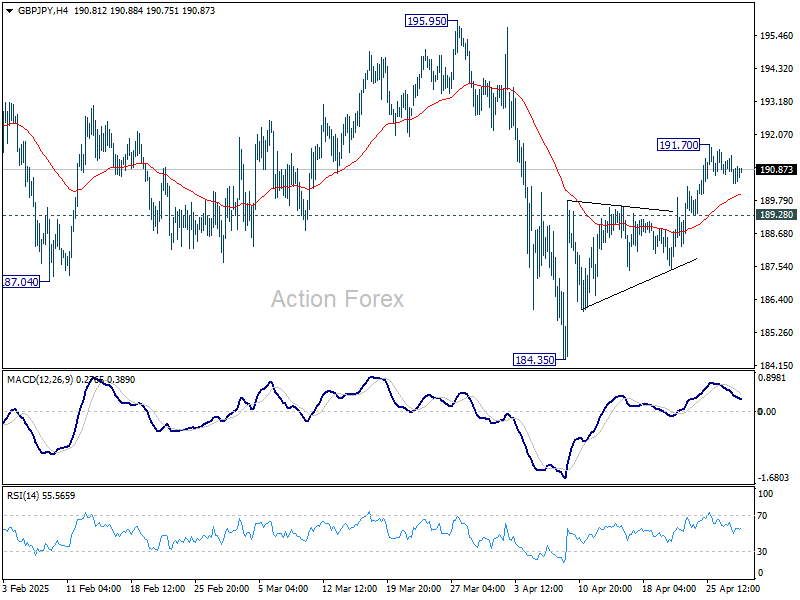

Intraday bias in GBP/JPY is turned neutral first with current retreat. Rebound from 184.35 is in favor to continue as long as 189.28 minor support holds. Above 191.70 will target 195.95 resistance next. However, break of 189.28 will suggest that the rebound has completed and turn bias back to the downside.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.