Markets Lifted by US-China Trade Thaw Hopes, But All Eyes on US Jobs Report – Action Forex

Markets trade on a cautiously optimistic in Asian session, supported by fresh signs that US-China trade tensions may be starting to thaw. China’s Commerce Ministry said the US has repeatedly expressed interest in reopening negotiations, adding that Beijing is “evaluating” these overtures. This marks the most constructive public tone from Beijing since the US enacted sweeping tariffs in April, raising hopes that some form of de-escalation could follow.

US Treasury Secretary Scott Bessent and White House adviser Kevin Hassett both echoed this optimism. Hassett told CNBC there have been informal discussions across both governments, and China’s recent move to ease duties on select US goods was interpreted as a possible opening gesture.

Despite the improving geopolitical mood, FX markets remain directionless outside of continued weakness in Yen following BoJ’s dovish posture and downgraded growth forecasts. Kiwi and Euro are also under mild pressure, while commodity currencies like the Aussie and Loonie are faring better, alongside Sterling. Dollar and Swiss Franc are mixed in the middle. This price action hints at budding risk-on sentiment, but conviction is still lacking ahead of today’s key US jobs report.

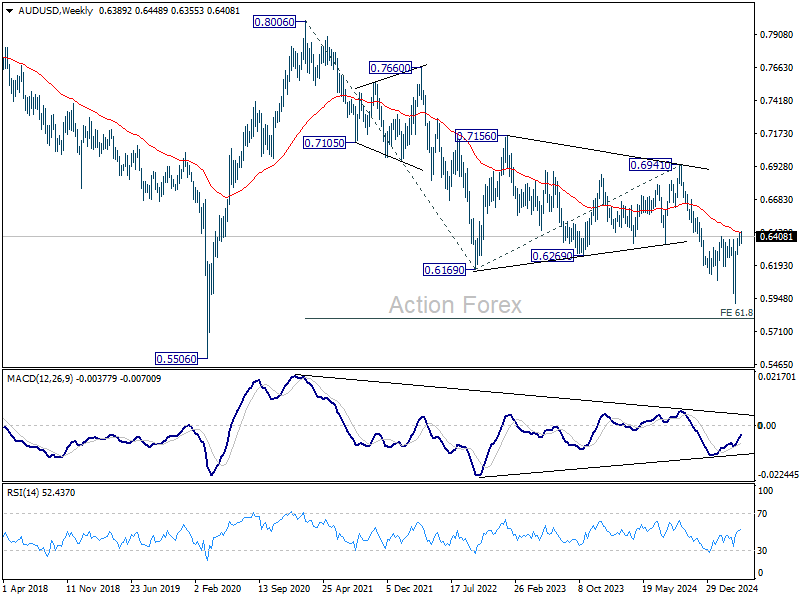

Technically, AUD/USD has been struggling in tight range for nearly two weeks already. The resistance from 55 W EMA is notable. Today’s US job data might finally give a clear direction to AUD/USD. Sustained break of the 55 W EMA should confirm that medium term bottom was already formed at 0.5916 in early April, and stronger rally would then be seen towards 0.6941 resistance even as a corrective move. However, rejection by the 55 W EMA will retain bearishness for a break through 0.5916 sooner rather than later.

In Asia, at the time of writing, Nikkei is up 1.18%. Hong Kong HSI is up 1.72%. China is on holiday. Singapore Strait Times is up 0.36%. Japan 10-year JGB yield is down -0.009 at 1.266. Overnight, DOW rose 0.21%. S&P 500 rose 0.63%. NASDAQ rose 1.52%. 10-year yield rose 0.054 to 4.231.

Looking ahead, Eurozone CPI flash will be the major focus in European session. Eurozone unemployment rate and PMI manufacturing final, Swiss PMI manufacturing will be released. Later in the day, US non-farm payroll employment and factory orders will be published.

Downside risks to NFP after ADP miss and rising Claims

The US April non-farm payroll report today will serve as a critical barometer of the labor market’s resilience amid rising macroeconomic uncertainty. While the recent flip-flopping of reciprocal tariffs may not yet be fully reflected in the data, other indicators suggest growing fragility.

A notable miss in today’s report could reignite concerns about recession, particularly following this week’s Q1 GDP data which showed unexpected contraction. For Fed, a disappointing jobs print would increase pressure to resume easing in June.

Markets expect 130K jobs growth in April, following a much stronger-than-expected 228K gain in March. Average hourly earnings are seen rising 0.3% mom. Unemployment rate likely held steady at 4.2%.

Recent labor market signals, however, lean toward downside risks. Initial jobless claims surged to 241K last week, pushing the 4-week average up to 226K. Meanwhile, ADP Employment report showed private payrolls rising by just 62K, a sharp deceleration from the revised 147K in March. The ISM Manufacturing PMI Employment sub-index also remained in contraction at 46.2, though it did tick up slightly from 44.7.

Australian retail sales grow 0.3% mom in March, but volumes flat in Q1

Australian retail sales rose by 0.3% mom in March to AUD 37.28 billion, slightly below expectations of 0.4% growth.

According to the ABS, food-related spending, particularly in supermarkets and grocery stores, was the main contributor to the uptick, with food and miscellaneous retailing both rising 0.7%. Clothing-related sales also edged higher, but household goods retailing was flat.

However, the broader trend is subdued, with retail sales volumes—adjusted for inflation—essentially flat over Q1. ABS Head of Business Statistics Robert Ewing noted that the lack of growth reflects weaker household appetite for discretionary goods, following a boost in spending late last year due to heavy promotions.

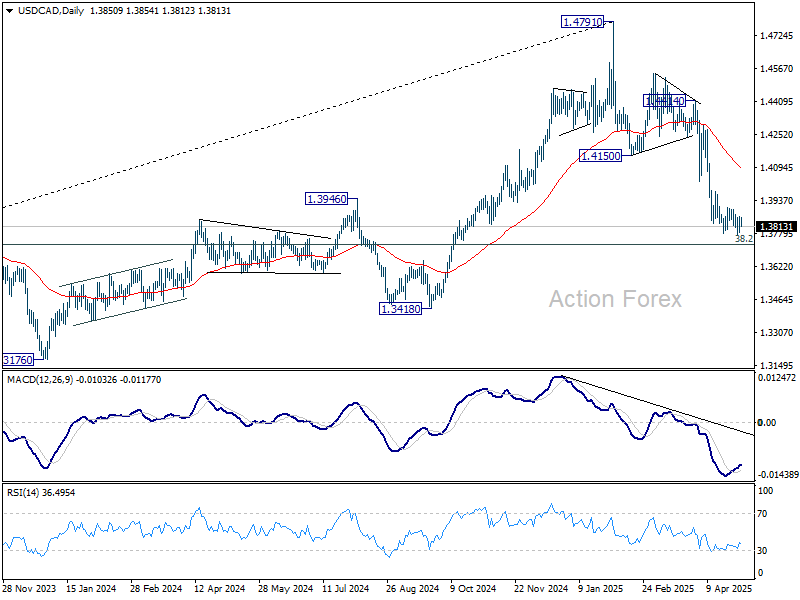

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3804; (P) 1.3834; (R1) 1.3883; More…

Intraday bias in USD/CAD is turned neutral again with current recovery. Deeper fall is expected as long as 1.3903 resistance holds. Below 1.3768 temporary low will resume the decline from 1.4791 to 1.3727 fibonacci level next. However, firm break of 1.3903 will indicate short term bottoming, and turn bias back to the upside for stronger rebound towards 55 D EMA (now at 1.4086).

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.