Dollar and Loonie Soft Ahead of Carney-Trump Meeting – Action Forex

Dollar remains on the soft side today, although losses are so far limited. Currency market activity is subdued as traders remain cautious ahead of the upcoming FOMC rate decision. While no policy changes are expected from the Fed tomorrow, markets are watching closely for any forward guidance. Notably, expectations for a June rate cut have continued to fade, with implied probabilities falling below 30%, reflecting the resilience of recent economic data, particularly on jobs.

However, the bigger driver of sentiment remains progress, or the lack thereof, on the trade front. Canadian Prime Minister Mark Carney is scheduled to meet President Donald Trump in Washington on Tuesday — the first face-to-face since Carney’s April 28 election victory. Trade and security are set to top the agenda. Canada is expected to bring proposals linked to energy and critical minerals, hoping to secure relief from US tariffs. Still, Carney has emphasized that substance will take precedence over speed.

Meanwhile, US Treasury Secretary Scott Bessent hinted on Monday that deals with some trading partners were “very close,” echoing Trump’s remarks over the weekend. Yet no concrete agreements have been announced. A Bloomberg report suggested India is willing to offer zero tariffs on selected goods, but details remain sparse. Overall, market optimism over trade progress exists but is tempered by repeated delays and lack of formal announcements.

So far this week, Dollar is the weakest performer, though still above last week’s lows. Loonie is also under pressure as markets await Carney’s Washington visit. Euro is lagging as well. Yen leads the gainers, followed by Kiwi and Swiss Franc. Sterling and Aussie are holding in the middle of the pack.

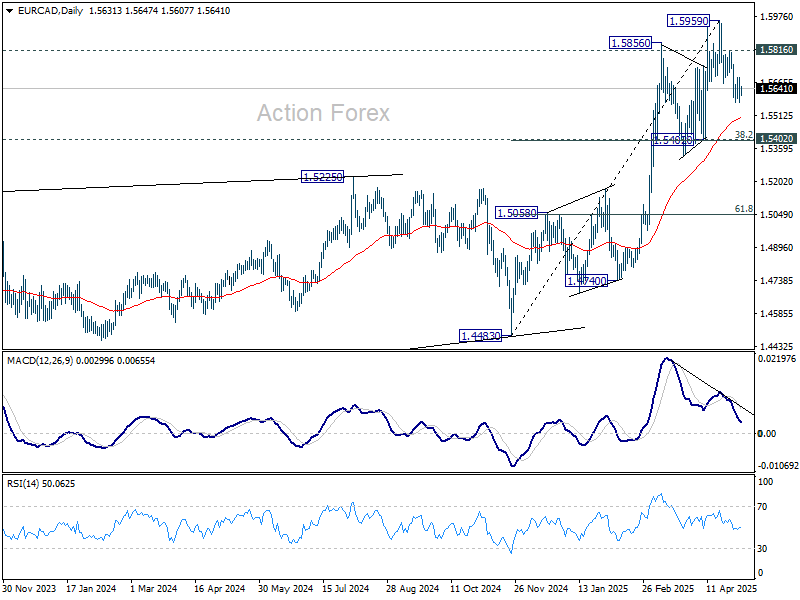

Technically’s EUR/CAD’s decline from 1.5959 is currently seen as part of a corrective pattern to the rally from 1.4483. Deeper fall is expected as long as 1.5816 resistance holds, to 55 D EMA (now at 1.5505) and possibly below. But strong support should be seen from 1.5402 cluster support (38.2% retracement of 1.4483 to 1.5959 at 1.5395) to contain downside.

In Asia, Japan is still on holiday, Hong Kong HSI is up 0.62%. China Shanghai SSE is up 0.93%. Singapore Strait Times is up 0.20%. Overnight, DOW fell -0.24%. S&P 500 fell -0.64%. NASDAQ fell -0.74%. 10-year yield rose 0.021 to 4.343.

Looking ahead, Swiss unemployment rate, France industrial production, Eurozone PMI services final and PPI, and UK PMI services final will be released in European session. Later in the day, Canada and US will publish trade balance.

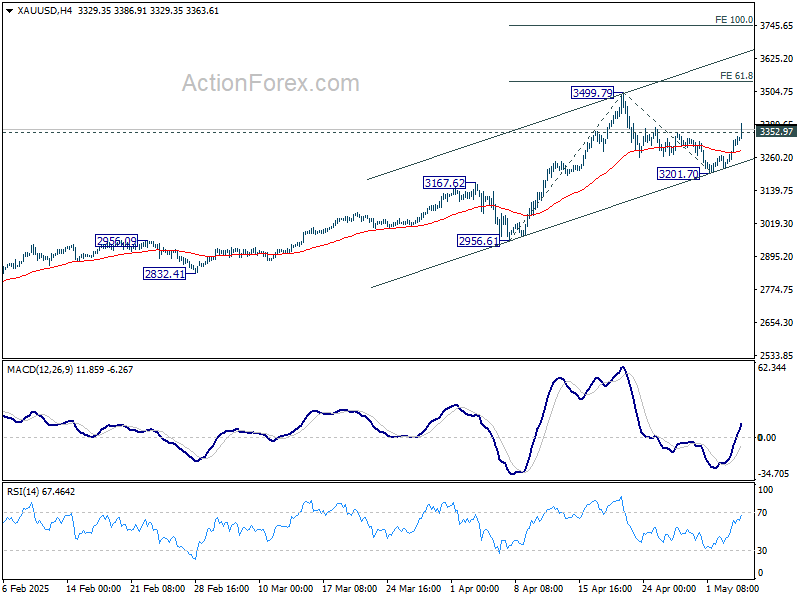

Gold breaks higher, eyes on 3500 and beyond

Gold’s extended rebound and break of 3352.97 resistance argues that correction from 3449.79 has already completed at 3201.70. Further rise is now expected to 3499.79 and then 61.8% projection of 2956.61 to 3449.70 from 3201.70 at 3537.38. Decisive break of 3537.38 could prompt upside acceleration towards 100% projection at 3744.88. However, break of 55 4H EMA (now at 3287.46) will resume the corrective fall from 3499.79 with another downleg.

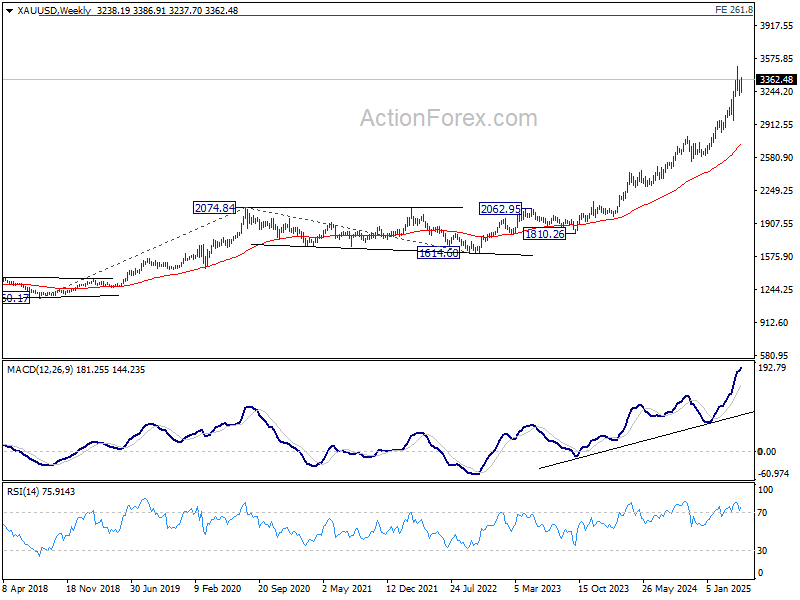

In the bigger picture, the long term up trend remains intact and there is no sign of loss of momentum in W MACD, despite overbought condition in W RSI. Next medium term target remains at 261.8% projection of 1160.17 to 2074.84 from 1614.60 at 4009.20, which is close to 4000 psychological level.

China’s Caixin PMI composite falls to 51.1, tariff impact to deepen in Q2–Q3

China’s Caixin PMI Services dropped to 50.7 in April, down from 51.9 and missing expectations of 51.7. PMI Composite also slipped from 51.8 to 51.1, signaling weaker momentum across both manufacturing and services.

According to Caixin’s Wang Zhe, the expansion in supply and demand has decelerated amid growing trade friction. Export-driven sectors remain under particular pressure, while job losses and muted pricing power continue to squeeze business margins. The employment component of the composite index also contracted.

Perhaps most concerning, expectations for future activity plunged to the lowest levels on record, reflecting rising uncertainty among firms. “The ripple effects of the ongoing China-US tariff standoff will gradually be felt in the second and third quarter”, Wang added.

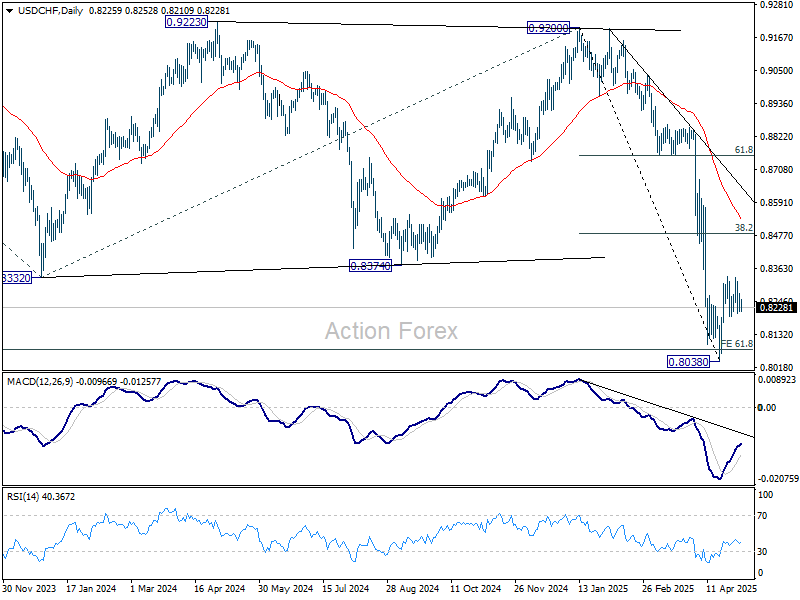

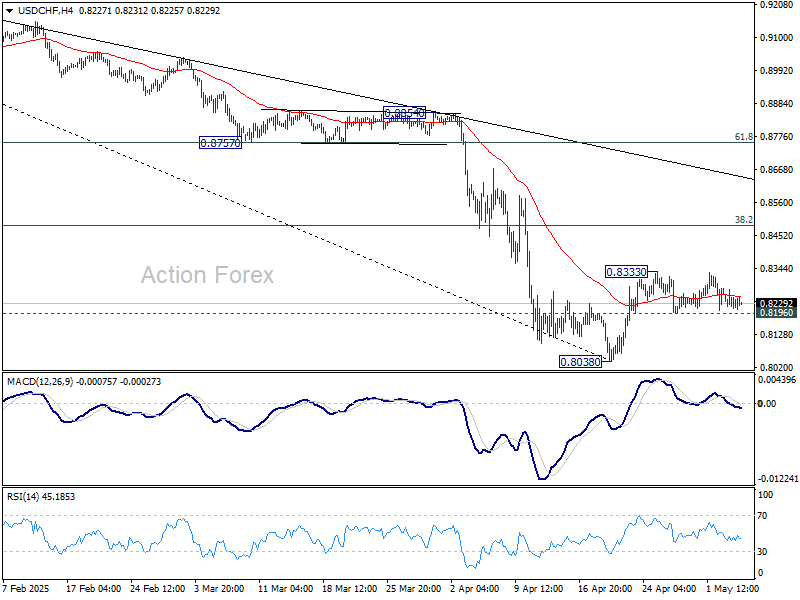

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8200; (P) 0.8237; (R1) 0.8261; More….

USD/CHF is still bounded in range below 0.8333 and intraday bias stays neutral at this point. On the upside, above 0.8333 will resume the rebound from 0.8038. However, upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, below 0.8196 minor support will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8763) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.