Franc and Euro Falter, Yen Strengthens as Risk-Off Returns – Action Forex

Both Swiss Franc and Euro are under some selling pressure today, especially against Sterling. The Franc suffered after SNB Chair Martin Schlegel signaled the willingness to reintroduce negative interest rates if deflationary risks persist. Meanwhile, Euro came under pressure as fresh political instability emerged in Germany

CDU/CSU leader Friedrich Merz’s failure to secure a parliamentary majority in his bid to become chancellor. Merz’s defeat highlighted cracks within his coalition and prompted concern across Europe. Eighteen coalition lawmakers reportedly broke ranks. European observers warned that Berlin’s political instability could have ramifications for EU-wide cohesion, especially at a time when coordinated responses to US tariffs are essential.

Euro’s fragility was further compounded by European Trade Commissioner Maros Sefcovic’s remarks in the European Parliament. He emphasized that all options remain on the table if US tariff negotiations fail. The EU is preparing contingency measures ahead of the July 8 deadline, with Sefcovic warning that US tariffs now affect 70% of EU exports and could rise to 97%.

Markets will be closely watching the results of the EU’s trade diversion task force due in mid-May, especially given the risk of redirected Chinese exports flooding European markets. While Sefcovic emphasized the EU’s preference for a negotiated settlement with the US, his tone reflected limited optimism for swift progress.

Despite Sterling rally again its European peers, it was Yen that claimed the top spot among major currencies today. The Pound is sitting at the second place, with Kiwi as the third. On the other hand, Swiss Franc is the worst performer, followed by Dollar and then Aussie. Euro and Loonie are positioning in the middle.

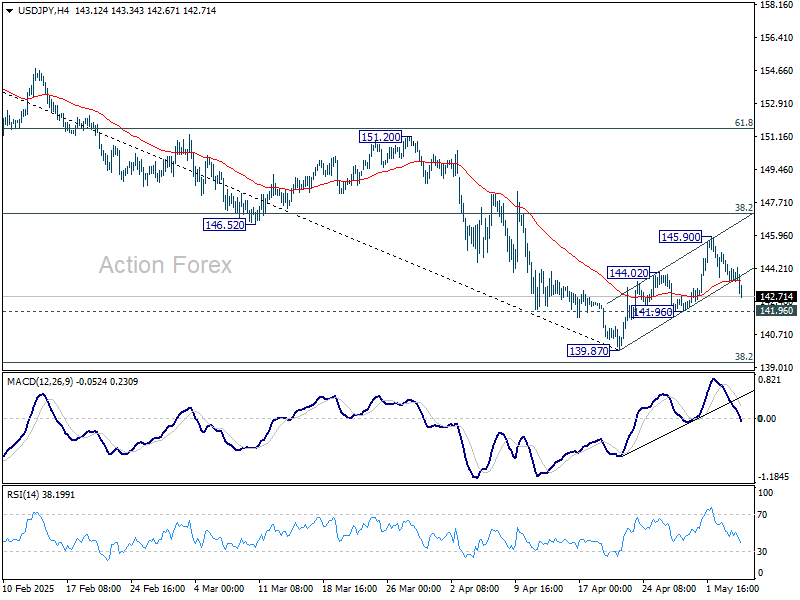

Technically, as USD//JPY’s decline from 145.90 gathers momentum, focus is now on 141.90 support. Firm break there will suggest that recovery from 139.87 has completed as a three-wave corrective move. Larger fall from 158.86 should then be ready to resume to 139.26 key long term fibonacci support.

In Europe, at the time of writing, FTSE is down -0.01%. DAX is down -0.54%. CAC is down -0.23%. UK 10-year yield is flat at 4.524. Germany 10-year yield is up 0.023 at 2.541. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.70%. China Shanghai SSE rose 1.13%. Singapore Strait Times rose 0.19%.

SNB’ Schlegel signals willingness to revisit negative rates

SNB Chairman Martin Schlegel said that while the central bank does not favor negative interest rates, it remains fully prepared to reintroduce them if necessary.

Speaking at an event today, Schlegel said “if we have to do it, the negative interest rates, we’re certainly prepared to do it again”.

“For the last couple of quarters, we have always said we are ready to intervene in the forex market if it’s necessary,” Schlegel said.

The comments come just a day after Swiss CPI data revealed that inflation slowed to 0% in April — the lowest reading in four years. The data has triggered market expectations that SNB will cut its policy rate from the current 0.25% at its upcoming meeting on June 19. Expectations are also mounting that rates could eventually fall back below zero this year.

Eurozone PPI falls -1.6% mom in March on steep energy decline

Eurozone PPI fell -1.6% mom in March, dragged down by a steep -5.8% mom drop in energy costs. Excluding energy, however, PPI ticked up 0.1% mom. Annually, PPI stood at 1.9% yoy, down from prior month’s 3.0% yoy.

Modest monthly gains was seen across most segments — 0.1% mom for capital goods, 0.2% mom for durable consumer goods, and 0.5% mom for non-durable goods. Intermediate goods were unchanged.

In the broader EU, PPI also fell -1.6% m/m and rose 2.1% yoy. The largest monthly decreases in industrial producer prices were recorded in Estonia (-8.0%), Spain (-3.9%) and Italy (-3.3%). The highest increases were observed in Greece (+1.3%), Luxembourg (+0.9%) and Slovenia (+0.6%).

Eurozone PMI services finalized at 50.1, cost pressure easing, hiring hesitant

Eurozone’s PMI Composite was finalized at 50.4 in April, down from 50.9 in March, confirming a sluggish start to Q2. The services sector, a critical growth engine, nearly stalled with a reading of 50.1, down from 51.0.

Nationally, Ireland (54.0) led the bloc in growth, followed by Spain (52.5) and Italy (52.1). Germany (50.1) was in slight expansion, while France (47.8) fell deeper into contraction territory.

Cyrus de la Rubia of Hamburg Commercial Bank noted that cost pressures in services remain “relatively high”, but easing price trends are adding weight to expectations for an ECB rate cut in June.

Employment growth across the Eurozone has stabilized, though businesses remain hesitant to expand their workforce amid continued uncertainty.

Country-level divergence is also growing more apparent. Germany’s growth is fragile but could improve in coming months, supported by its new fiscal stimulus measures.

UK PMI servies finalized at 49.0, tariffs and wage costs hit outlook

UK PMI Services was finalized at 49.0 in April, down from 52.5 in March, its lowest level since January 2023. PMI Composite also dropped into contraction at 48.5, marking the first negative reading in 18 months.

S&P Global’s Tim Moore pointed to heightened business uncertainty as a major drag on activity. Export conditions were the weakest since early 2021. Rising payroll costs linked to National Insurance hikes and increased National Living Wage rates contributed to the sharpest input cost growth since mid-2023. Service providers responded with their steepest price increases in nearly two years.

Business confidence deteriorated significantly as “service sector firms braced for an extended period of global economic turbulence and heightened recession risks.” 22% of firms forecasted a decline in activity over the next 12 months—more than triple the level seen after the 2024 general election.

China’s Caixin PMI composite falls to 51.1, tariff impact to deepen in Q2–Q3

China’s Caixin PMI Services dropped to 50.7 in April, down from 51.9 and missing expectations of 51.7. PMI Composite also slipped from 51.8 to 51.1, signaling weaker momentum across both manufacturing and services.

According to Caixin’s Wang Zhe, the expansion in supply and demand has decelerated amid growing trade friction. Export-driven sectors remain under particular pressure, while job losses and muted pricing power continue to squeeze business margins. The employment component of the composite index also contracted.

Perhaps most concerning, expectations for future activity plunged to the lowest levels on record, reflecting rising uncertainty among firms. “The ripple effects of the ongoing China-US tariff standoff will gradually be felt in the second and third quarter”, Wang added.

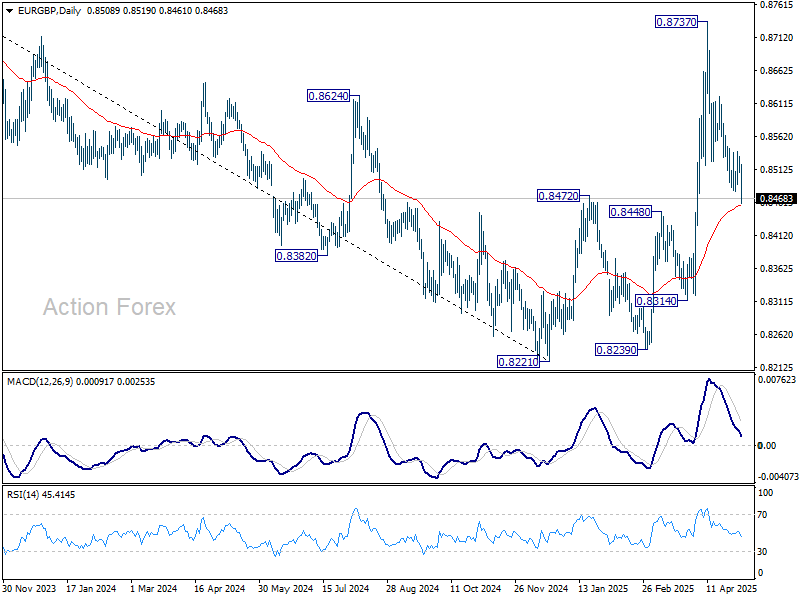

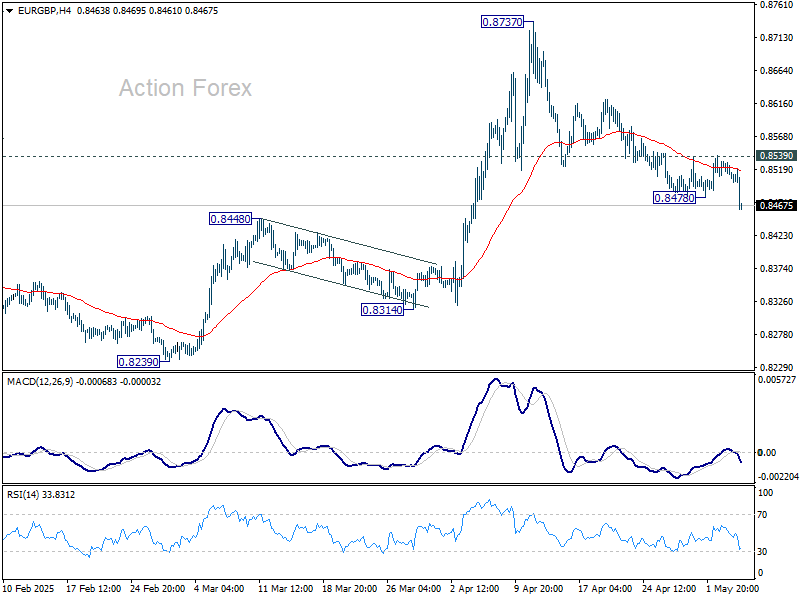

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8504; (P) 0.8518; (R1) 0.8527; More…

EUR/GBP’s fall from 0.8737 resumed after brief consolidations and intraday bias is back on the downside. Sustained trading below 55 D EMA (now at 0.8457) will suggest that whole rise from 0.8221 has already complete and turn outlook bearish. Nevertheless, rebound from current level, followed by break of 0.8539 resistance, will suggest that the correction from 0.8737 has completed, and retain near term bullishness.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will remain the favored case as long as 0.8472 resistance turned support holds. However, firm break of 0.8472 will argue that the down trend hasn’t completed yet.