Calm in Currency Markets Ahead of Fed’s Fourth Straight Hold – Action Forex

The forex markets are treading water ahead of today’s FOMC decision. While the announcement typically acts as a volatility trigger, the lack of suspense surrounding this meeting could mean muted price action even after Chair Jerome Powell’s press conference. Markets are pricing in a near-certainty, 99% probability, that Fed will hold the policy rate steady at 4.25–4.50% for a fourth straight meeting, leaving little room for surprise. Adding to the quiet is the absence of updated economic projections and dot plot guidance, which are only due at the June meeting.

Last week’s stronger-than-expected non-farm payrolls cooled expectations for near-term easing, with the chance of a June rate cut falling to around 30%. Traders will be closely watching Powell’s tone for any nuanced shift, particularly regarding the timing of the next rate cut. However, officials are likely to maintain their cautious, data-dependent posture given persistent economic uncertainty, especially around the evolving US tariff policies.

Indeed, Powell is expected to reiterate that the Fed is not in a hurry to adjust rates. The ongoing tariff truce and upcoming negotiations—such as this weekend’s Geneva meeting between U.S. and Chinese trade officials—introduce substantial geopolitical risks that could influence inflation, growth, and financial conditions. With so many moving parts, Fed is unlikely to make any forward commitments. For now, the market still leans toward three rate cuts by year-end, which would bring the target range down to 3.50–3.75%, but policymakers are not ready to validate that path.

In terms of price action so far this week, the Dollar has underperformed, joined by Loonie and Swiss Franc near the bottom of the board. Yen has led gains, followed by Kiwi and Sterling. Euro and Aussie are positioned in the middle. But with ranges tightly held, these relative standings could shift quickly depending on today’s Fed tone and incoming trade headlines.

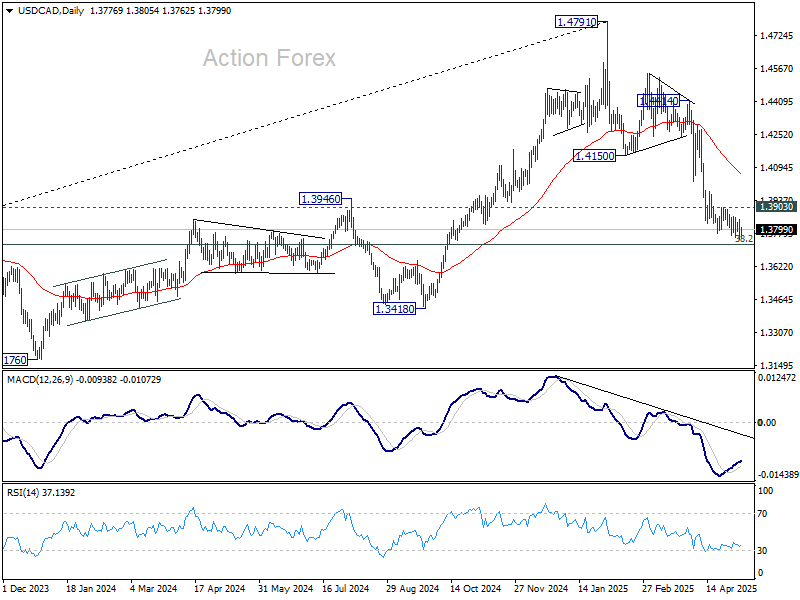

Technically, USD/CAD has clearly lost must momentum, as seen in D MACD, as it approaches 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727. Break of 1.3903 resistance should indicate short term bottoming, and bring stronger rebound back to 55 D EMA (now at 1.4057). However, firm break of 1.3727 could then bring deeper fall to 1.3418 support before USD/CAD tries to bottom again.

In Europe, at the time of writing, FTSE is down -0.53%. DAX is down -0.24%. CAC is down -0.68%. UK 10-year yield is down -0.049 at 4.471. Germany 10-year yield is down -0.04 at 2.503. Earlier in Asia, Nikkei fell -0.14%. Hong Kong HSI rose 0.13%. China Shanghai SSE rose 0.80%. Singapore Strait Times rose 0.13%. Japan 10-year JGB yield rose 0.038 to 1.300.

Eurozone retail sales fall -0.1% mom in March

Eurozone retail sales slipped by -0.1% mom in March, in line with expectations. The breakdown shows marginal declines across key categories, with food, drinks, and tobacco sales down -0.1%, and non-food products (excluding fuel) also falling -0.1%. Only automotive fuel recorded a modest rise, up 0.4%.

Across the broader EU, retail trade also declined -0.1% mom. Notable contractions were seen in Slovenia (-2.0%), Estonia (-1.3%), and Slovakia (-0.9%). Malta led the gainers with a 2.0% increase, followed by Belgium, Croatia (both +1.4%), and Bulgaria (+1.1%).

Japan’s PMI composite finalized at 51.2, input inflation jumps to 2-year high

Japan’s private sector returned to expansion in April, as the final PMI Composite rose to 51.2 from March’s 48.9. The improvement was driven entirely by the services sector, with its PMI climbing to 52.4, while manufacturing remained in contraction.

According to S&P Global’s Annabel Fiddes, stronger services activity helped offset the drag from factories, where new orders fell sharply in response to the global tariff environment.

While services firms reported stronger demand, confidence among both services and manufacturing sectors deteriorated. Businesses expressed concern about the broader global outlook and the negative implications of recent US tariff moves on growth potential.

Adding to the pressure, input price inflation accelerated to a two-year high, prompting firms to raise selling prices to protect margins.

NZ employment grow 0.1% in Q1, wages growth cool

New Zealand’s employment grew just 0.1% qoq as expected, while the unemployment rate held steady at 5.1%, better than forecast of 5.3%.

However, the quality of employment deteriorated, with a notable shift from full-time to part-time roles. Over the year, full-time employment dropped by -45k while part-time roles increased by 25k.

Participation rate edged down to 70.8% and the employment rate slipped to 67.2%, both suggesting a gradual loss in labor market momentum.

Wage growth also moderated, with the labour cost index rising 2.9% annually, down from 3.3% in the previous quarter.

PBoC unleashes broad-based monetary easing including rate and RRR cuts

China’s central bank has announced a sweeping set of monetary policy measures to support its economy, starting with a 10bps cut in the seven-day reverse repo rate to 1.40%, effective May 8. In a more aggressive move, the PBoC will also slash the reserve requirement ratio by 50bps, releasing approximately CNY 1T into the banking system.

The new package is structured into three categories: quantitative, price-based, and structural tools. The quantitative arm focuses on long-term liquidity via the RRR cut. The price-based measures involve lowering benchmark and structural policy rates. The structural component aims to channel credit into strategic areas such as technological innovation, consumption, and inclusive finance.

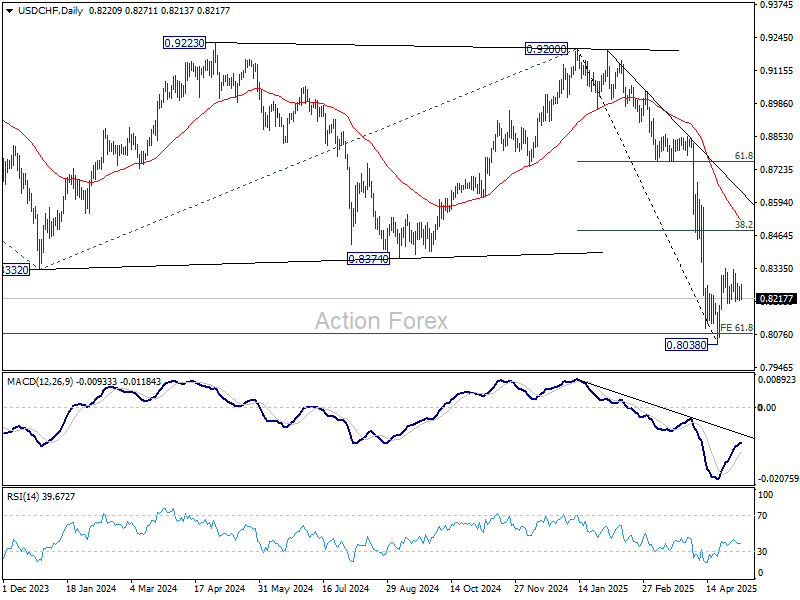

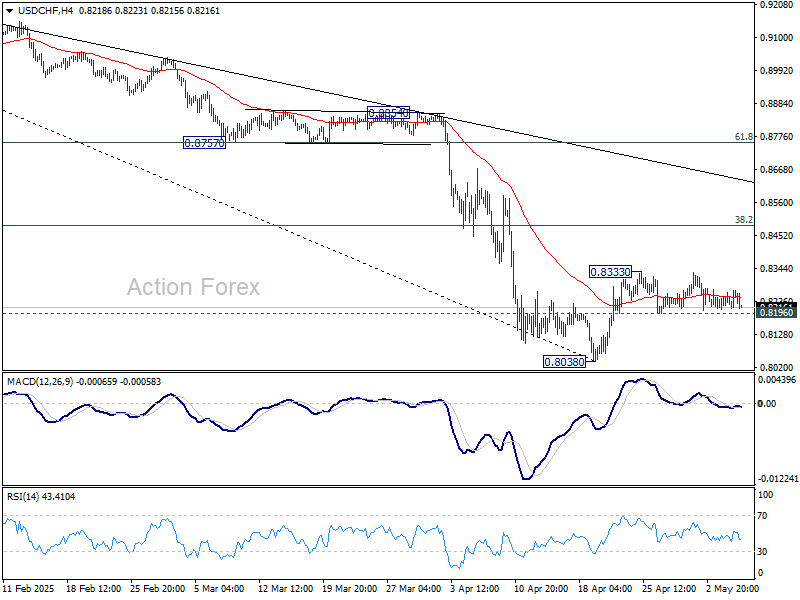

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8201; (P) 0.8233; (R1) 0.8254; More….

USD/CHF is still bounded in right range below 0.8333 and intraday bias remains neutral for the moment. On the upside, above 0.8333 will resume the rebound from 0.8038. However, upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, below 0.8196 minor support will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8763) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.