Markets Turn Cautious Again Ahead of US-China Talks in Switzerland – Action Forex

The forex markets are quiet today, with major pairs largely consolidating after yesterday’s modest directional movement. Dollar and British Pound remain the strongest performers overall, bolstered earlier in the week by the announcement of the US-UK trade agreement. However, both currencies are now struggling to extend their momentum. Canadian Dollar continues to lag after today’s mixed employment report. European equities are trading slightly higher, and US futures are also edging up, but the broader market mood is subdued.

Attention is now shifting to the upcoming meeting between US and Chinese trade representatives in Switzerland this weekend. Caution is in the air after President Trump suggested in a social media post that tariffs on Chinese goods could be cut from 145% to 80%—a comment that sparked tentative optimism. While some economists are hopeful for at least partial tariff relief, expectations remain low for any immediate breakthrough.

History tempers optimism. The last major US-China trade deal took two years of negotiations following the initial tariff escalation in 2018, and that process was marked by repeated false starts and reversals. As such, the meeting in Switzerland is widely viewed as a tentative first step rather than a venue for concrete outcomes. Any signals of goodwill or further dialogue would be welcome, but markets are unlikely to price in significant progress until more substance materializes.

For the week so far, Dollar remains the top performer, followed by Sterling and Yen. On the weaker end, Kiwi has underperformed, trailed by Loonie and Aussie. Euro and Swiss Franc sit in the middle.

In Europe, at the time of writing, FTSE is up 0.34%. DAX is up 0.74%. CAC is up 0.86%. UK 10-year yield is up 0.024 at 4.576. Germany 10-year yield is up 0.031 at 2.573. Earlier in Asia, Nikkei rose 1.56%. Hong Kong HSI rose 0.40%. China Shanghai SSE fell -0.30%. Singapore Strait Times rose 0.73%. Japan 10-year JGB yield rose 0.029 to 1.354.

Canada’s jobs grow 7.4k, unemployment rate jumps to 6.9%

Canada’s labor market posted a modest gain of 7.4k jobs in April, slightly above expectations of 4.1k, following a sharp loss of -33k positions in March and a flat February. While the headline number suggests some stabilization, broader labor indicators point to underlying weakness.

Unemployment rate rose from 6.7% to 6.9%, above expectations, and is now back at its November 2024 level, the highest since January 2017 excluding the pandemic years.

The employment rate slipped another 0.1 percentage points to 60.8%, matching a recent low seen in October 2024.

Wage growth also showed signs of easing, with average hourly earnings increasing 3.4% yoy, down from 3.6% yoy in March. Meanwhile, total hours worked rose by 0.4% mom and 0.9% yoy.

Fed’s Barr: Tariffs to push inflation higher, job losses also a major concern

In a speech today, Fed Governor Michael Barr acknowledged that the US economy began the current quarter from a “relatively strong position,” describing overall conditions as “resilient.” However, he cautioned that this solid foundation is being increasingly overshadowed by rising trade policy uncertainty, particularly from the recent wave of tariffs.

Barr expected “tariffs to lead to higher inflation” in the US and “lower growth” starting later this year. He explained that the new tariffs—unprecedented in size and scope in the modern era—could disrupt global supply chains and exert lasting upward pressure on prices. At the same time, he is “equally concerned” that the resulting economic drag could lead to job losses.

Despite these risks, he emphasized that monetary policy is in a “good position” to adjust as needed once the full effects of the tariffs become clearer.

Fed’s Kugler: Labor market stable, likely near maximum employment

In a speech today, Fed Governor Adriana Kugler described the U.S. labor market as “stable,” noting that key indicators such as the unemployment rate, currently at 4.2%, have remained within a narrow and consistent range.

She highlighted that temporary layoffs have returned to pre-pandemic levels, and both job vacancies and quit rates have plateaued, indicating a moderation in labor market churn.

Kugler further stated that the economy is likely “close to maximum employment,” referencing model-based estimates of the natural rate of unemployment (u*) that align with the current 4.2% level.

BoE’s Bailey highlights asymmetric risks: Demand weakness warrants sharper monetary response

In a speech following BoE’s Monetary Policy Report released yesterday, Governor Andrew Bailey elaborated on the two alternative scenarios laid out alongside the baseline forecast.

The first scenario envisions that heightened global and domestic uncertainty could suppress UK demand more than currently expected, “easing inflationary pressures”.

In contrast, the second scenario assumes that recent energy price increases could trigger renewed second-round effects in domestic prices, with tighter supply conditions “increasing inflationary pressures”.

Bailey emphasized that these scenarios are not simply stylized upside or downside risks to inflation but are meant to illustrate the underlying mechanisms that could shift the inflation path.

He stressed, “it matters whether inflation differs from the baseline because of demand or supply”. And, the size of the required monetary policy response might be different.

From a monetary policy standpoint, Bailey explained that a demand-driven downside scenario would likely warrant a stronger policy response than a supply-driven upside shock. That’s “simply because there is more of a trade-off to balance when inflation and activity move in different directions,” he added.

ECB’s Simkus and Rehn warn of growth risks

Comments from ECB Governing Council members today reinforced expectations for a rate cut in June, while also highlighting growing concern over the deteriorating macro environment.

Lithuania’s Gediminas Šimkus acknowledged that geopolitical developments since the start of the year have been negative for the economy, adding that inflation is now under “downward pressure”. He noted that June projections “may be a little bit worse” and warned of the risk the central bank will undershoot its inflation target.

He also pointed to the risk of China re-routing goods to Europe in response to rising US trade barriers—a trend that could weigh on European industry and import prices.

Šimkus indicated that a June rate cut is needed but remained non-committal on the pace of further easing, saying it’s still unclear whether the next move after June would come in July or September.

Separately, Finland’s Olli Rehn struck a similar tone, citing pervasive uncertainty and reaffirming that the Governing Council will retain “full freedom of action” to meet its price stability mandate.

While Rehn noted that progress has been made in bringing inflation toward the 2% target, he cautioned that global trade tensions pose a meaningful downside risk to growth.

Japan wage growth slows while Real incomes shrink, but spending rebounds

Japan’s wage data for March showed a softening trend. Nominal total cash earnings rose 2.1% yoy, below expectations of 2.4% yoy and down from February’s 2.7% yoy. This marked the 39th consecutive month of nominal wage growth, but the pace is clearly losing momentum.

More concerning was the continued decline in inflation-adjusted real wages, which fell -2.1% yoy, down for a third straight month, highlighting the squeeze on household purchasing power as consumer prices remained elevated at 4.2% yoy, particularly for food staples like rice.

Base salaries (regular pay) grew 1.3% yoy, unchanged from February, suggesting underlying wage trends remain stable but not accelerating. However, overtime pay, often viewed as a proxy for labor demand, fell -1.1% yoy, marking its first decline since September and the sharpest drop since April last year.

Despite the income pressures, household spending surprised to the upside. It rose 2.1% yoy, far exceeding the expected 0.2% yoy and marking the first increase in two months. On a seasonally adjusted month-on-month basis, spending climbed 0.4%. The increase was largely driven by higher electricity bills and rising education-related expenses.

China’s exports surge 8.1% yoy in April, ASEAN shipments jump 20.8% yoy, US slide -21% yoy

China’s exports surged 8.1% yoy to USD 315.7B in April, far exceeding expectations of 1.9% yoy. However, the headline strength masks key shifts in trading patterns.

Exports to the US tumbled by -21% yoy, a sharp reversal from March’s 9.1% yoy gain, reflecting the drag from elevated tariffs. In contrast, shipments to the ASEAN bloc jumped 20.8% yoy, with Vietnam, often seen as a transshipment route for Chinese goods, seeing a 22.5% yoy rise.

Yet, with the US now eyeing a steep 46% tariff on Vietnamese imports and imposing a 10% baseline levy, this channel for China could soon come under pressure.

Elsewhere, exports to the European Union also improved, rising 8.3% yoy.

Imports dipped just -0.2% yoy, a much smaller contraction than the expected -5.9% yoy. As a result, trade surplus narrowed from USD 102.6B to USD 96.2B, above the expected USD 94.3B.

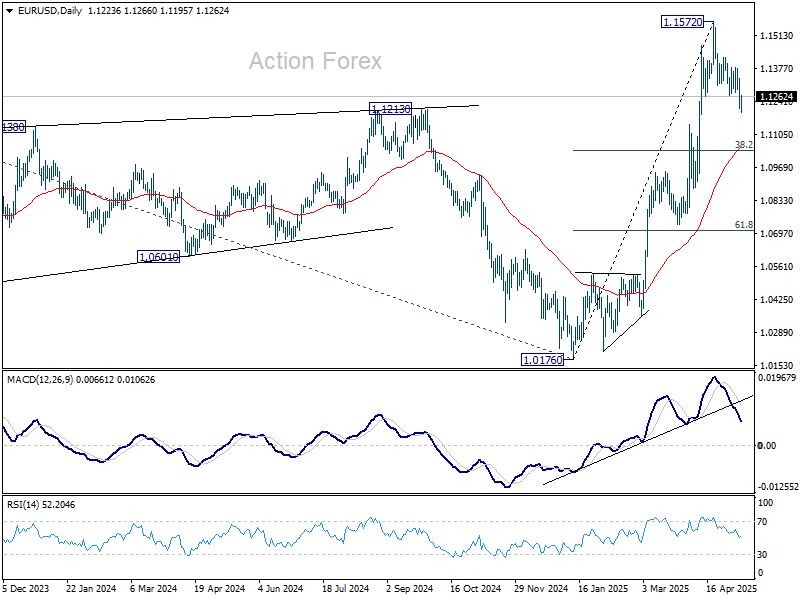

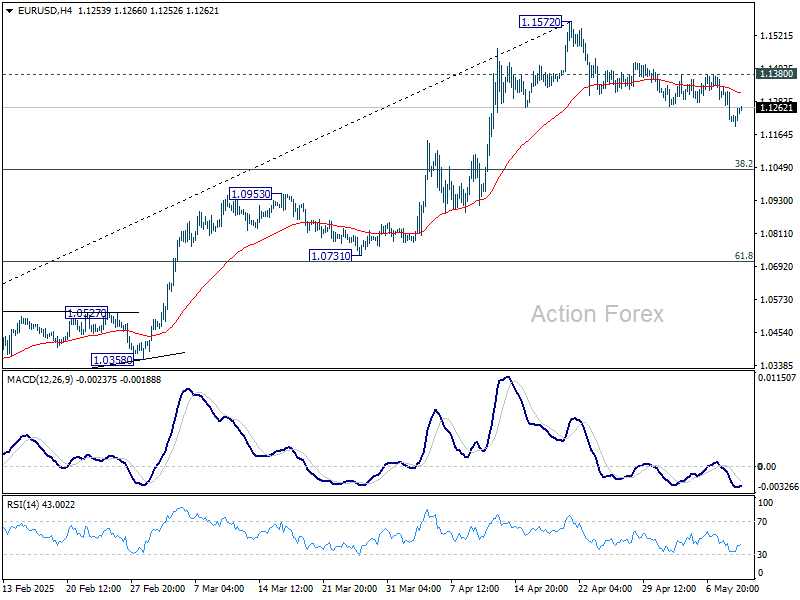

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1181; (P) 1.1259; (R1) 1.1305; More…

Intraday bias in EUR/USD remains mildly on the downside for the moment. Corrective fall from 1.1572 is still in progress to 38.2% retracement of 1.0176 to 1.1572 at 1.1039. But strong support should be seen there to bring rebound. On the upside, break of 1.1380 will suggest that the correction has completed, and bring retest of 1.1572.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0808) holds.