Dollar Eases as Trade Boost Fades, Sterling Finds Support on Wages and BoE Rhetoric – Action Forex

Dollar softened slightly in early US trading today, though the move appears more related to a fading post-trade-deal rally than any direct reaction to economic data. While April’s inflation report showed encouraging progress on headline disinflation, the core CPI reading held firm, suggesting underlying price pressures remain sticky. That dynamic should keep Fed cautious, and today’s market reaction suggests the data did little to shift expectations meaningfully. The more optimistic takeaway, however, is that recent tariffs have yet to significantly lift inflation.

In contrast, Sterling is gaining some traction, particularly against Euro, following solid UK wage data. Despite signs of softening in overall employment, wage growth remains robust, with average earnings still running well above levels consistent with BoE’s 2% inflation target. BoE Chief Economist Huw Pill reinforced that concern by warning that more aggressive or sustained policy action may be needed to bring inflation under control. His remarks have helped underpin Sterling sentiment.

Overall in the currency markets, Aussie has overtaken Dollar to become the week’s top performer. Kiwi and Loonie are also firm. At the other end of the spectrum, Yen continues to struggle, while Swiss Franc and Euro are also soft.

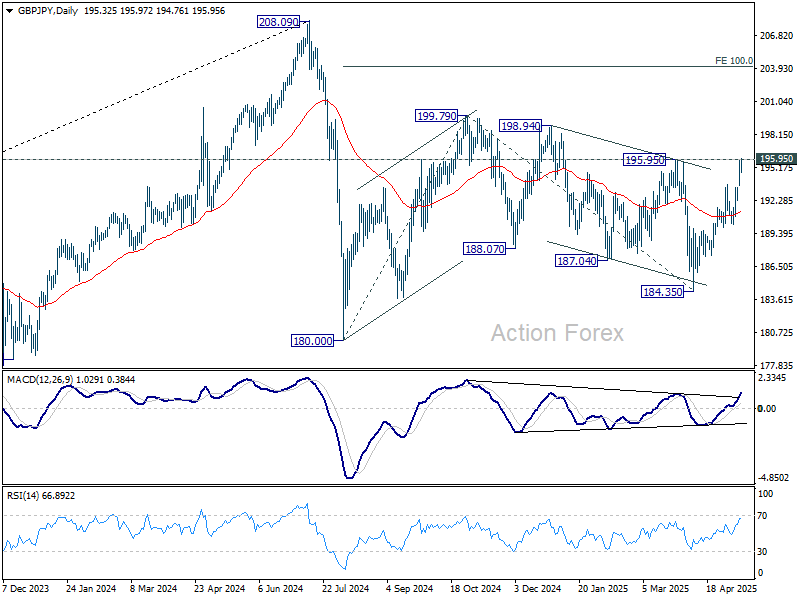

Technically, GBP/JPY is now pressing 195.95 resistance as rise from 184.35 extends. Decisive break of 195.95 will argue that choppy fall from 199.79 has completed at 184.35 already. More importantly, rise from 180.00 might then be ready to resume through 199.79 in this bullish case.

In Europe, at the time of writing, FTSE is up 0.05%. DAX is up 0.17%. CAC is up 0.23%. UK 10-year yield is up 0.021 at 4.671. Germany 10-year yield is up 0.013 at 2.666. Earlier in Asia, Nikkei rose 1.43%. Hong Kong HSI fell -1.87%. China Shanghai SSE rose 0.17%. Singapore Strait Times rose 0.13%. Japan 10-year JGB yield rose 0.06 to 1.449.

US CPI hits four year low at 2.3%, but core inflation holds steady at 2.8%

US headline CPI rose just 0.2% mom, below the expected 0.3% mom. Core CPI, excluding food and energy, also increased by 0.2%, undershooting forecasts of 0.3% mom.

On an annual basis, headline inflation eased to 2.3% yoy from 2.4% yoy, the lowest rate since April 2021. Core inflation held steady at 2.8% yoy, in line with expectations.

Shelter remained the key driver of monthly inflation, rising 0.3% mom and accounting for over half of the total increase.

Energy prices also ticked higher by 0.7% mom, while food prices declined slightly by -0.1% mom. On a year-over-year basis, energy costs dropped by -3.7%, helping to keep overall inflation in check, while food prices rose 2.8%.

BoE’s Pill: May require more aggressive and persistent effort to bring down inflation

Speaking at a press conference today, BoE Chief Economist Huw Pill warned that returning inflation to the BoE’s 2% target may prove more difficult than anticipated. Hence, Pill said the central bank may need to respond in a “somewhat more aggressive or more persistent” way to ensure inflation is brought under control within a reasonable time frame.

He raised concerns that recent shifts in wage and price-setting behavior might reflect a more “structural change”, drawing parallels with inflation dynamics of the 1970s and 1980s.

Pill emphasized that investors should not interpret BoE’s latest forecast, showing inflation returning to target by early 2027 based on market-implied rates, as a clear endorsement of future rate cuts.

Instead, he pointed to the Bank’s more inflationary risk scenario, which assumed persistently weak productivity and stronger wage pressures. These conditions, he said, echo past inflation crises, where elevated price levels triggered repeated and entrenched pay demands.

Last week, Pill voted against the BoE’s quarter-point rate cut, aligning with fellow hawk Catherine Mann in preferring to keep rates unchanged.

UK payrolled employment falls -33k, wage growth remains elevated

UK labor market data for April showed signs of softening in employment but continued strength in wage growth. Payrolled employment fell by -33k (-0.1% mom), while the claimant count rose by 5.2k. Median monthly pay rose by 6.4% yoy in April, accelerating from 5.9% yoy in the previous month.

In the three months to March, unemployment rate in the three months to March edged up from 4.4% to 4.5%, in line with expectations and marking the highest level since late 2021.

Average earnings including bonuses rose 5.5% yoy, beating expectations of 5.2% yoy. Earnings excluding bonuses rose 5.6% yoy, slightly below forecast of 5.7% yoy.

German ZEW economic sentiment surges on stabilizing domestic politics and trade progress

Investor sentiment in Germany and the wider Eurozone improved sharply in May, with ZEW Economic Sentiment Index for Germany jumping from -14.0 to 25.2, well above the expected 9.8. Eurozone sentiment followed suit, rising from -18.5 to 11.6, also beating expectations.

According to ZEW President Achim Wambach, the rebound reflects growing optimism tied to easing trade tensions, a new German government, and stabilizing inflation, helping to offset last month’s sharp deterioration.

However, views on current conditions remain deeply negative. Germany’s Current Situation Index edged down further from -81.2 to -82.0, missing forecasts. Eurozone’s improved modestly but still stood at -42.2. This divergence suggests that while expectations for the months ahead are improving, near-term economic conditions remain fragile, particularly in Germany.

BoJ’s Uchida sees temporary inflation pause, but wage growth to persist

BoJ Deputy Governor Shinichi Uchida said today that while Japan’s underlying inflation and medium- to long-term inflation expectations may “temporarily stagnate”, wage growth is expected to remain firm as “Japan’s job market is very tight.”

He added that companies are likely to continue “passing on rising labour and transportation costs by increasing prices”.

Uchida also stressed that BoJ will assess the economic impact of US trade policy “without pre-conception,” acknowledging the high degree of uncertainty surrounding the global outlook.

BoJ opinions: Sees tariff risks but maintains flexible rate-hike stance

BoJ’s Summary of Opinions from its April 30–May 1 meeting revealed a generally cautious view on the impact of US tariffs, with board members acknowledging the potential economic damage but not seeing it as enough to derail the pursuit of the 2% inflation target.

One member noted that BoJ may enter a “temporary pause” in rate hikes due to weaker US growth. But it’s emphasized that “it shouldn’t be too pessimistic”.

The member emphasized that rate hikes could resume if conditions improve or US policy shifts.

Other opinions highlighted the high level of uncertainty facing Japan’s economic and price outlook, driven largely by global trade tensions. One board member noted the policy path “may change at any time.”

Another reaffirmed that there has been “no change to the BoJ’s rate-hike stance”, as projections continue to show inflation reaching the 2% target and real interest rates remain deeply negative.

Australian Westpac consumer sentiment rises to 92.1, weak confidence supports RBA cut

Australia’s Westpac Consumer Sentiment Index rose 2.2% to 92.1 in May, partially recovering from April’s sharp decline triggered by trade-related uncertainty.

Westpac attributed the modest rebound to stronger financial markets and a decisive outcome in the Federal election. However, sentiment remains subdued, with the index still 3.9% below its March level and firmly in pessimistic territory.

With all key inflation measures now back within the 2–3% target range, Westpac expects RBA to cut the cash rate by another 25bps to 3.85%. The combination of soft domestic sentiment and a more “unsettled and threatening global backdrop” strengthens the case for further easing.

Australia’s NAB business conditions weaken to 2, profit pressures mount

Australia’s NAB Business Confidence Index edged up from -3 to -1 in April. However, the underlying Business Conditions Index slipped from 3 to 2. Trading conditions eased from 6 to 5, while profitability dropped sharply from 0 to -4, highlighting the ongoing strain on margins.

Purchase cost growth accelerated to 1.7% in quarterly equivalent terms, up from 1.4%. Labor cost growth remained elevated at 1.6%. Rising input costs appear to be eroding profitability, with businesses struggling to pass through the full extent of these increases. This was reflected in modest increases in final product and retail price growth, which rose to 0.8% and 1.4% respectively—still below the pace of input cost growth.

NAB Chief Economist Sally Auld noted that weaker profitability was at the core of the drop in business conditions, aligning with the uptick in purchase costs and softer trading performance.

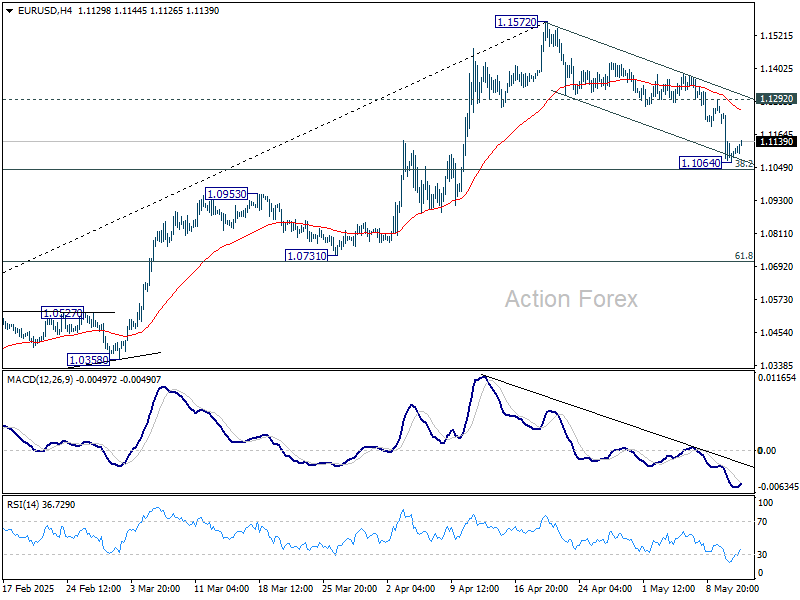

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1022; (P) 1.1132; (R1) 1.1199; More…

Intraday bias in EUR/USD is turned neutral first with current recovery. Overall, strong support should be seen from 38.2% retracement of 1.0176 to 1.1572 at 1.1039 to bring rebound. On the upside, break of 1.1380 will suggest that the correction from 1.1572 has completed, and bring retest of 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.