Fed Cut Bets Recede Ahead of US CPI, Dollar Approaches Key Resistance – Action Forex

Global equity markets surged overnight in response to the breakthrough US-China tariff truce, with risk appetite roaring back across the board. DOW jumped more than 1100 points, while S&P 500 and NASDAQ surged 3.26% and 4.35%, respectively. The relief rally extended into Europe, where Germany’s DAX surged to a new record high, reflecting broad optimism that trade tensions have eased significantly—at least for now. In Asia, Japan’s Nikkei jumped nearly 1.8% in early trading as it played catch-up, though the boost faded in Hong Kong where HSI turned lower, signaling some regional caution.

In the currency markets, however, the initial momentum has slowed. Dollar remains the strongest currency for the week so far, supported by rising Treasury yields and expectations that Fed will maintain its high interest rate longer. Commodity currencies like the Australian, Canadian, and New Zealand Dollars are also holding firm, buoyed by improved risk sentiment. Meanwhile, Yen and European majors continue to lag.

The attention now shifts to today’s US April CPI release, which will be the first major inflation print since the April tariff escalation and the subsequent truce. Although the immediate impact of tariffs may not be fully visible yet, any upside surprise could reinforce Fed’s message of caution. While that may further support Dollar, it’s unlikely to significantly dampen the broader risk-on mood, given that markets have already recalibrated expectations following the trade deal.

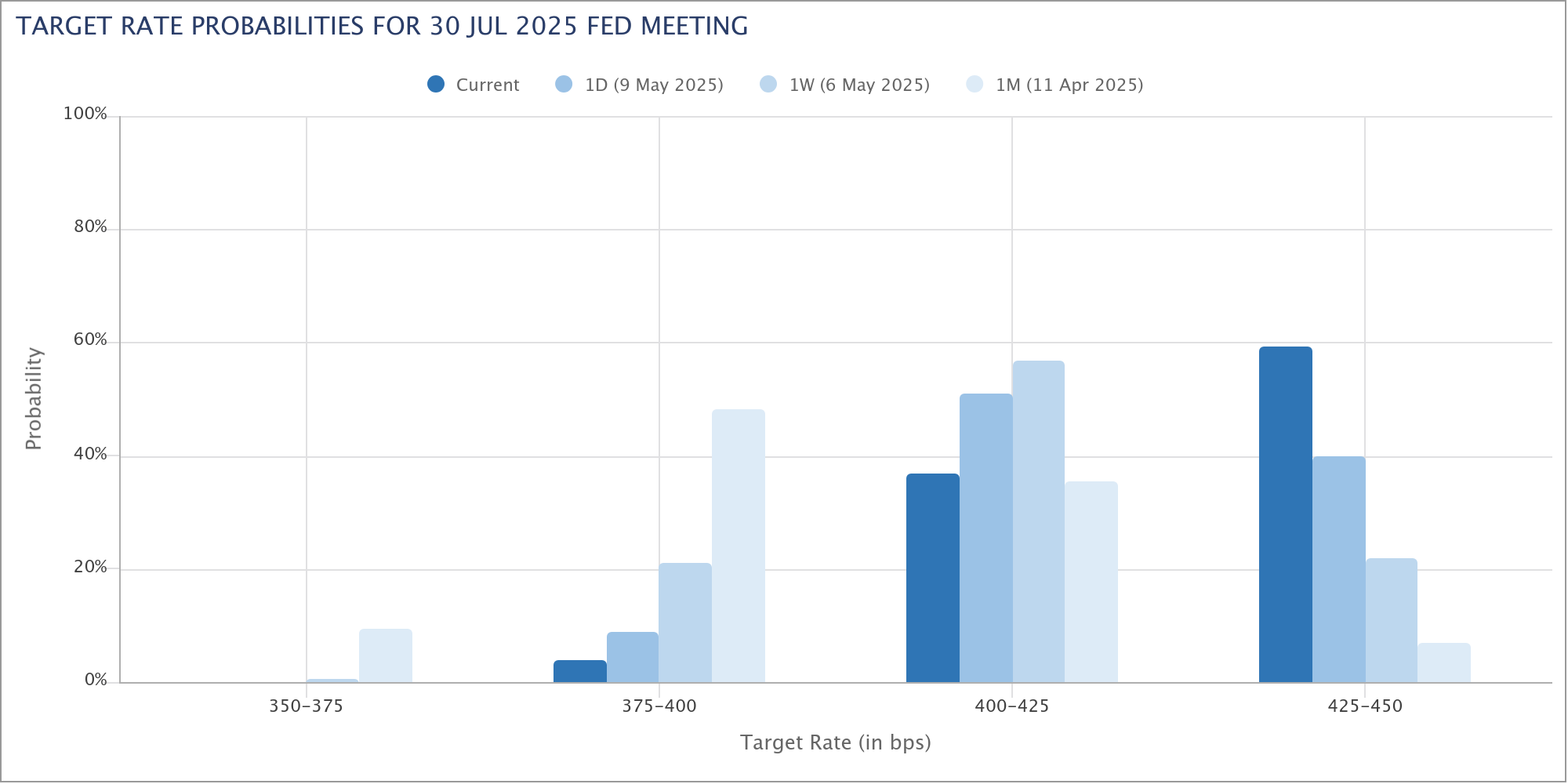

Indeed, Fed fund futures have responded decisively to the latest developments. A week ago, markets were pricing in a 74% chance of a July rate cut. That probability has now dropped sharply to 41% in the wake of the tariff truce. This suggests that traders have already priced in a “higher for longer” Fed policy stance, reducing the likelihood of any sudden repricing unless inflation data comes in meaningfully above expectations.

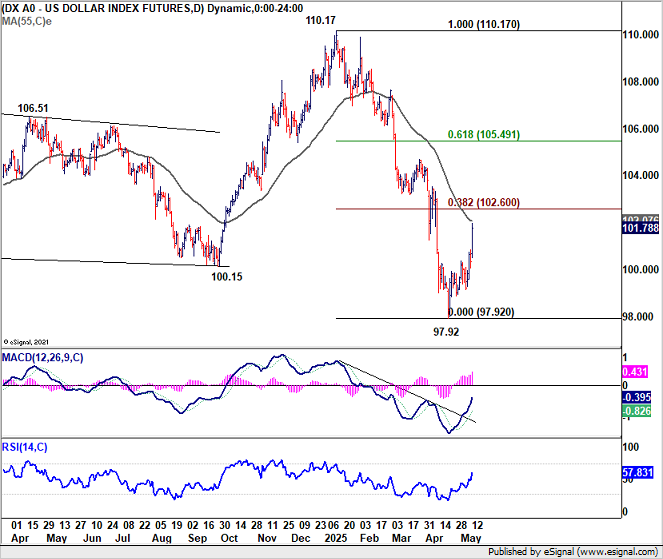

Technically, with yesterday’s strong rally, DXY will enter into a key resistance zone ahead, between 55 D EMA (now at 102.07) and 38.2% retracement of 110.17 to 97.92 at 102.60. For now, rebound from 97.92 is still seen as part of a correction to the fall from 110.17. Hence, strong resistance should be seen from 102.07/60 to limit upside, at least on first attempt. However, sustained break of this zone will raise the chance of reversal, and target 61.8% retracement at 105.49 next.

In Asia, at the time of writing, Nikkei is up 1.79%. Hong Kong HSI is down -1.67%. China Shanghai SSE is up 0.08%. Singapore Strait Times is up 0.43%. Japan 10-year JGB yield is up 0.07 at 1.459. Overnight, DOW rose 2.81%. S&P 500 rose 3.26%. NASDAQ rose 4.35%. 10-year yield rose 0.082 to 4.457.

Looking ahead, UK employment data and German ZEW economic sentiment will be the main feature in European session. Later in the day, US CPI is the center of focus.

Fed’s Goolsbee warns tariff truce still carries stagflation risk

Chicago Fed President Austan Goolsbee welcomed the weekend’s US-China tariff agreement as a step in the right direction but cautioned that its limited scope offers only modest relief.

In an interview with the New York Times, he said the temporary 90-day reduction in tariffs would be “less impactful stagflationarily than the path they were on.”

But that still represents a significant burden on the economy. With tariffs remaining three to five times higher than pre-trade war levels, Goolsbee warned the deal would still “make growth slower and make prices rise”, hallmarks of a stagflationary environment.

Given the persistent uncertainty surrounding US trade policy, Goolsbee reiterated his support for a wait-and-see approach on interest rates. He noted that the Trump administration’s statements acknowledge the temporary nature of the current truce. “It’s going to be revisited in the near future,” he said.

BoE’s Taylor defends 50bps cut, cites perilous trade climate and weak demand

BoE MPC member Alan Taylor explained his decision to vote for a 50bps rate cut last week, warning that both global and domestic conditions have deteriorated significantly.

He pointed to a “quite perilous” international trade environment, driven in large part by broader-than-expected US tariffs. Also, “the erosion of confidence that we saw has continued”, he added, with low readings in business surveys like the PMI and REC, along with signs of increased precautionary saving and delayed investment.

Taylor also called the recent UK-US trade deal “quite slender,” noting that most British exports will still face a 10% tariff, offering little near-term relief for exporters.

Taylor warned that waiting for complete confirmation that all inflation pressures had eased before easing policy further could leave BoE behind the curve.

ECB officials signal cautious path to June cut

Latvian ECB Governing Council member Martins Kazaks indicated overnight that a rate cut in June remains a “pretty possible step,” aligning with market expectations, provided upcoming data confirms progress toward anchoring inflation around the 2% target.

Kazaks added that “gradual cautious cuts could come upon the anchoring of inflation to around the 2% target.”

Meanwhile, German and Spanish ECB members Joachim Nagel and Jose Luis Escriva added a note of caution in a joint interview, warning that US President Donald Trump’s aggressive tariff policies have clouded the economic outlook.

“Regarding monetary-policy decisions, it is important to be cautious and not to overreact by overemphasizing specific announcements that could change shortly afterwards,” Nagel emphasized.

BoJ’s Uchida sees temporary inflation pause, but wage growth to persist

BoJ Deputy Governor Shinichi Uchida said today that while Japan’s underlying inflation and medium- to long-term inflation expectations may “temporarily stagnate”, wage growth is expected to remain firm as “Japan’s job market is very tight.”

He added that companies are likely to continue “passing on rising labour and transportation costs by increasing prices”.

Uchida also stressed that BoJ will assess the economic impact of US trade policy “without pre-conception,” acknowledging the high degree of uncertainty surrounding the global outlook.

BoJ opinions: Sees tariff risks but maintains flexible rate-hike stance

BoJ’s Summary of Opinions from its April 30–May 1 meeting revealed a generally cautious view on the impact of US tariffs, with board members acknowledging the potential economic damage but not seeing it as enough to derail the pursuit of the 2% inflation target.

One member noted that BoJ may enter a “temporary pause” in rate hikes due to weaker US growth. But it’s emphasized that “it shouldn’t be too pessimistic”.

The member emphasized that rate hikes could resume if conditions improve or US policy shifts.

Other opinions highlighted the high level of uncertainty facing Japan’s economic and price outlook, driven largely by global trade tensions. One board member noted the policy path “may change at any time.”

Another reaffirmed that there has been “no change to the BoJ’s rate-hike stance”, as projections continue to show inflation reaching the 2% target and real interest rates remain deeply negative.

Australian Westpac consumer sentiment rises to 92.1, weak confidence supports RBA cut

Australia’s Westpac Consumer Sentiment Index rose 2.2% to 92.1 in May, partially recovering from April’s sharp decline triggered by trade-related uncertainty.

Westpac attributed the modest rebound to stronger financial markets and a decisive outcome in the Federal election. However, sentiment remains subdued, with the index still 3.9% below its March level and firmly in pessimistic territory.

With all key inflation measures now back within the 2–3% target range, Westpac expects RBA to cut the cash rate by another 25bps to 3.85%. The combination of soft domestic sentiment and a more “unsettled and threatening global backdrop” strengthens the case for further easing.

Australia’s NAB business conditions weaken to 2, profit pressures mount

Australia’s NAB Business Confidence Index edged up from -3 to -1 in April. However, the underlying Business Conditions Index slipped from 3 to 2. Trading conditions eased from 6 to 5, while profitability dropped sharply from 0 to -4, highlighting the ongoing strain on margins.

Purchase cost growth accelerated to 1.7% in quarterly equivalent terms, up from 1.4%. Labor cost growth remained elevated at 1.6%. Rising input costs appear to be eroding profitability, with businesses struggling to pass through the full extent of these increases. This was reflected in modest increases in final product and retail price growth, which rose to 0.8% and 1.4% respectively—still below the pace of input cost growth.

NAB Chief Economist Sally Auld noted that weaker profitability was at the core of the drop in business conditions, aligning with the uptick in purchase costs and softer trading performance.

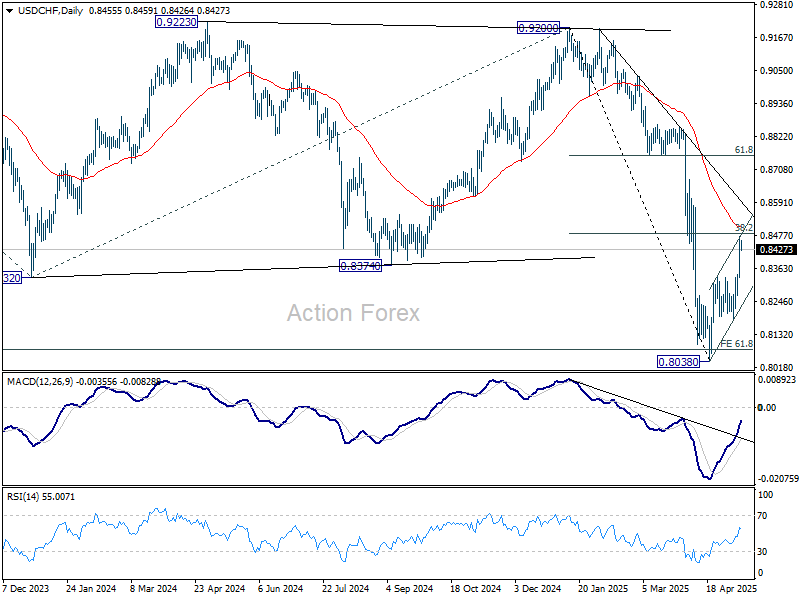

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8367; (P) 0.8421; (R1) 0.8512; More….

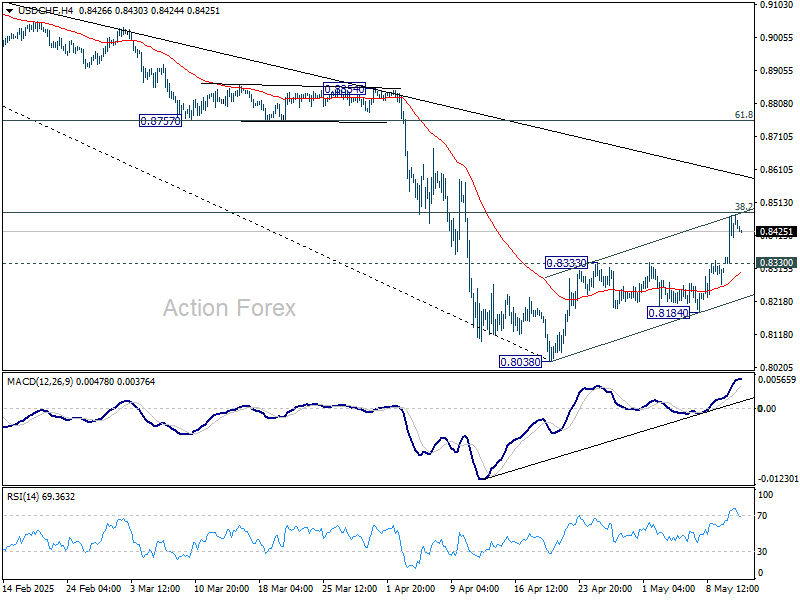

USD/CHF’s rebound from 0.8038 is still seen as a corrective move. Strong resistance is expected from 38.2% retracement of 0.9200 to 0.8038 at 0.8482 to limit upside. Break of 0.8330 resistance turned support will turn intraday bias will turn bias back to the downside. Further break of 0.8184 will bring retest of 0.8038 low. However, sustained trading above 0.8482 will dampen this bearish view and target 61.8% retracement at 0.8756 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8750) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.