Dollar Steadies After Early Weakness, Focus Turns to Australia Jobs Data – Action Forex

Dollar faced broad selling pressure throughout the Asian and European sessions but has since found some footing as markets transition into the US trading day. However, direction remains murky, with traders appearing undecided on whether to push the greenback higher or extend the recent pullback. A similar tone of uncertainty is mirrored in equities, as European indexes drift sideways and US futures show little conviction. With no major catalysts in the immediate pipeline, both FX and equity markets are likely to stay range-bound until fresh data offers clearer cues.

Attention now turns to Thursday’s key releases, including Australia’s April employment report and the UK’s GDP figures. While Australia’s stronger-than-expected Q1 wage price index suggested some resilience in pay growth, the detail showed continued moderation in the private sector. This is unlikely to derail RBA’s expected rate cut next week, as the central bank remains focused on cushioning the economy from tariff-related risks. The upcoming April employment data will be more telling—especially if it deviates significantly from the expected 20.9k job growth and 4.1% unemployment rate. A downside surprise could fuel speculation of faster easing later this year.

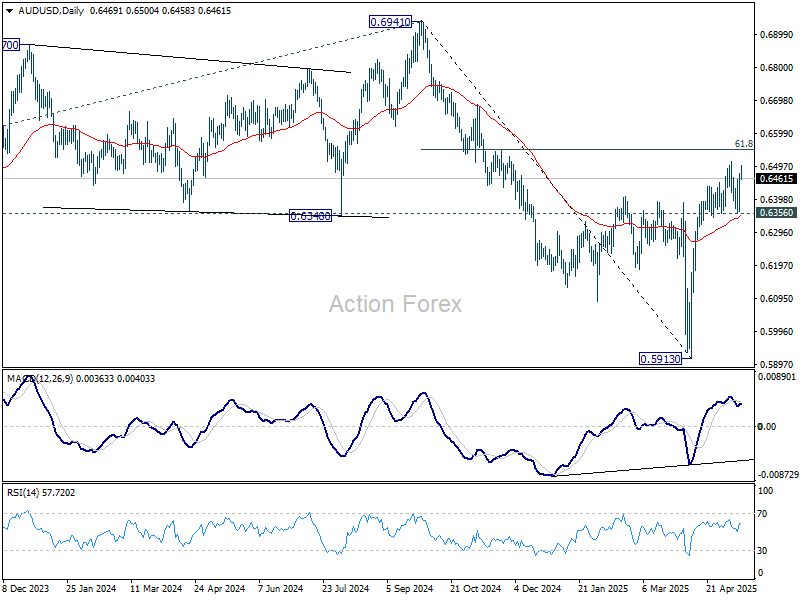

Technically, AUD/USD has struggled to establish momentum, despite a supportive risk-on backdrop. Even if a short-term rally resumes, 61.8% retracement of 0.6941 to 0.5913 at 0.6548 is likely to provide strong resistance to bring at least a near term pullback.

In Europe, at the time of writing, FTSE is up 0.09%. DAX is down -0.18%. CAC is down -0.29%. UK 10-year yield is up 0.039 at 4.715. Germany 10-year yield is up 0.005 at 2.686. Earlier in Asia, Nikkei fell -0.14%. Hong Kong HSI rose 2.30%. China Shanghai SSE rose 0.86%. Singapore Strait Times fell -0.26%. Japan 10-year JGB yield rose 0.008 to 1.457.

Fed’s Goolsbee urges patience amid ‘dusty’ data and tariff uncertainty

Chicago Fed President Austan Goolsbee cautioned against overinterpreting April’s softer inflation data, noting on NPR that it’s still too early to gauge the true impact of rising US import tariffs.

While recent consumer price figures suggest inflation may be easing, Goolsbee stressed that Fed needs more clarity before making firm policy judgments, describing the current environment as one filled with “a lot of dust in the air.”

He acknowledged that the data so far “suggest that it’s going okay,” but emphasized the difficulty of drawing long-term conclusions amid ongoing short-term volatility.

“It’s just not realistic,” he said, “to expect businesses or central banks to be jumping to conclusions” in such an uncertain setting.

ECB’s Nagel stresses Dollar’s global role, cautious on tariff impact ahead of June decision

German ECB Governing Council member Joachim Nagel emphasized the continued importance of the Dollar as a global reserve currency during remarks today. At the same time, he expected that Euro would gradually play a stronger role in the international financial system over the coming years.

Looking ahead to ECB’s June policy meeting, Nagel reiterated that the interest rate decision will be guided by incoming data. He acknowledged the uncertainty surrounding the impact of US tariffs on inflation and growth within the Eurozone.

The updated ECB staff projections, due next month, would be essential in shaping the decision. Nagel also stressed that central banks must increasingly adapt to operating in an environment characterized by persistent geopolitical and policy-driven uncertainty.

BoE hawk Mann: Labor market resilient, and firms yet to lose pricing power

BoE MPC member Catherine Mann explained her notable policy shift during an interview with CNBC, revealing why she moved from backing a 50bps rate cut in February to voting for a hold at last week’s meeting.

Mann cited the UK labor market’s resilience as a key factor in her reassessment. While recent data suggest some moderation “a slowing labor market”, she argued that “it is not a non-linear adjustment.”

Mann also flagged a new risk emerging from tariffs. She warned that rising US tariffs on countries like China could lead to an influx of diverted exports into markets such as the UK. While this could temporarily ease goods prices at the border, she cautioned that domestic retailers may use the opportunity to rebuild profit margins, keeping upward pressure on consumer price inflation rather than alleviating it.

Crucially, Mann emphasized the need to see a broad-based “loss of pricing power” in firms. “I need to see that firms are starting to be much more moderate in setting their prices across a broad range of products,” she added. “Goods price inflation is actually going up, not down.”

Japan’s PPI rises 4% yoy in April, record high for 8th straight month

Japan’s PPI rose 4.0% year-on-year in April, easing slightly from 4.3% yoy in March and matching market expectations. Despite the modest slowdown, the index climbed to a fresh record high of 126.3, marking the eighth consecutive month of new highs, highlighting persistent cost pressures at the wholesale level.

However, the data also showed little immediate impact from the sweeping US tariffs announced in early April, thanks in part to the 90-day suspension.

Japan’s Yen-based import price index fell sharply by -7.2% yoy in April, following a -2.4% yoy decline in March. The drop suggests that Yen’s appreciation during the market turmoil have helped shield Japanese importers from some of the price shocks, at least for now.

Australian wage growth accelerates to 3.4% yoy in Q1, led by public sector

Australia’s Wage Price Index rose by 0.9% qoq in Q1, slightly above market expectations of 0.8% qoq. Public sector saw a stronger 1.0% qoq gain, outpacing the 0.9% qoq rise in private sector.

On an annual basis, wages grew by 3.4%, up from 3.2% in the previous quarter, marking the first uptick in annual wage growth since mid-2024.

The uptick in annual wage growth was driven primarily by the public sector, which saw a notable increase to 3.6% yoy from 2.9% yoy in Q4. Private sector wage growth was steady at 3.3% yoy.

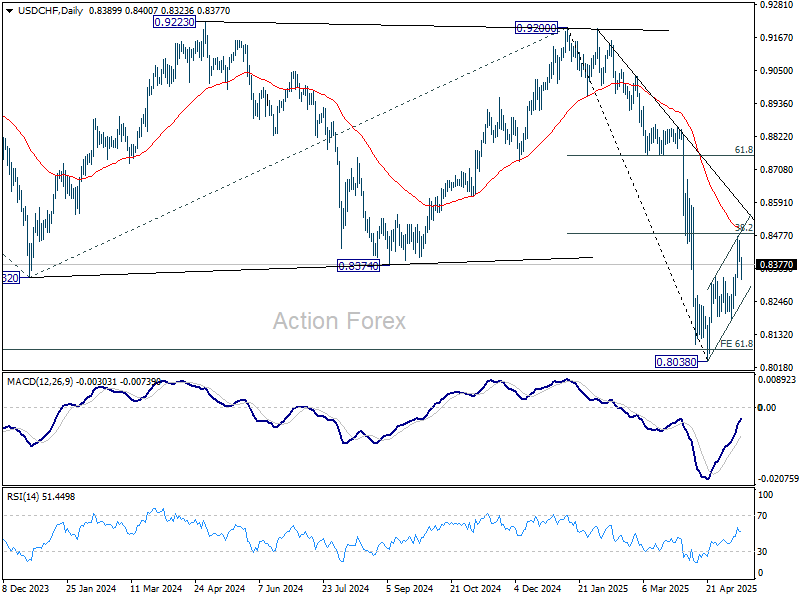

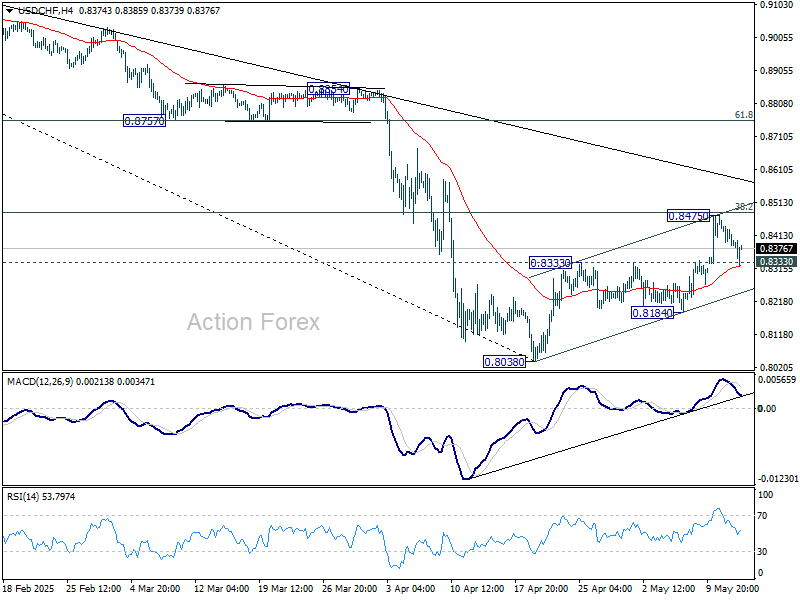

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8367; (P) 0.8415; (R1) 0.8442; More….

Intraday bias in USD/CHF remains neutral for the moment. On the downside, firm break of 0.8333 resistance turned support will argue that corrective rebound from 0.8038 has completed at 0.8475, after rejection by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. Intraday bias will be back on the downside for 0.8184, and then retest of 0.8038 low. However, sustained trading above 0.8482 will dampen this bearish view and target 61.8% retracement at 0.8756 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8750) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.