Weak Data Overlooked as Yen Rises on Risk-Off Mood – Action Forex

Mild risk-off mood is helping Yen to extend its near-term rebound, despite fresh signs of economic weakness at home. Japan’s economy was already showing signs of strain even before the impact of US tariffs, with Q1 GDP contracting more sharply than expected. BoJ is left in an increasingly precarious position, wedged between deteriorating growth and persistent inflationary pressures.

A recent Reuters poll taken between May 7 and 13 revealed a significant shift in market expectations, with 67% of economists now projecting that BoJ will hold its policy rate at 0.50% through the third quarter. That’s up sharply from just 36% a month ago, highlighting how tariff-related risks have changed expectations for near-term tightening.

On the trade front, Japan is preparing a third round of negotiations with the US, as it seeks to secure exemptions from tariffs on automobiles and auto parts. In return, Tokyo is reportedly considering a set of concessions, including increased imports of US corn and soybeans, regulatory changes to auto inspection standards, and cooperation in shipbuilding technology.

Chief negotiator Ryosei Akazawa is expected to travel to Washington as early as next week, though the timeline hinges on progress in working-level talks. Meanwhile, Finance Minister Katsunobu Kato will travel to Canada for G7 meetings, where he may hold bilateral discussions with US Treasury Secretary Scott Bessent on foreign exchange matters.

Overall for the week so far, Yen is currently the top performer, followed by Sterling and then Dollar. Kiwi is the weakest, trailed by Euro and Swiss Franc. Loonie and Aussie sit in the middle of the pack. The overall tone in the currency markets remains mixed.

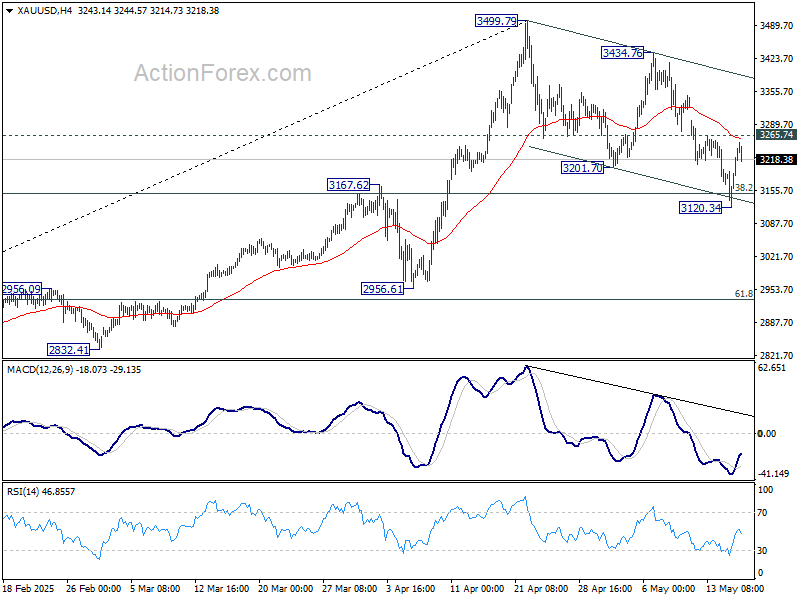

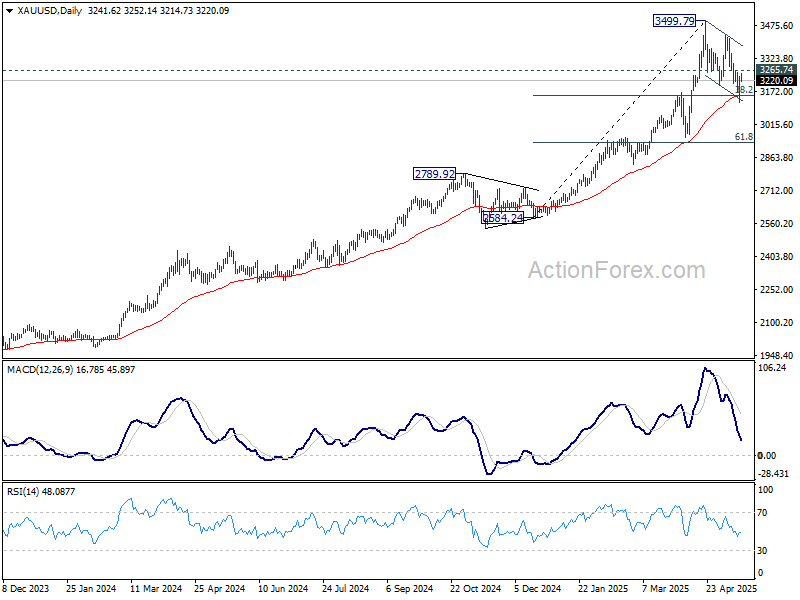

Technically, Gold has bounced from key cluster support around 3150, including 55 D EMA (now at 3151.09) and 38.2% retracement of 2584.24 to 3499.79 at 3150.04. It’s possible that correction from 3499.79 has completed already. Firm of 3265.74 will reinforce this bullish case, and suggest that larger up trend is ready to resume. If realized, that should be accompanied by another round of selloff in Dollar. However, sustained break of 3150 will dampen this view and bring deeper fall to 61.8% retracement at 2933.98.

In Asia, at the time of writing, Nikkei is down -0.06%. Hong Kong HSI is down -0.40%. China Shanghai SSE is down -0.34%. Singapore Strait Times is down -0.20%. Japan 10-year JGB yield is down -0.016 at 1.463. Overnight, DOW rose 0.65%. S&P 500 rose 0.41%. NASDAQ fell -0.18%. 10-year yield fell -0.073 to 4.455.

Looking ahead, Eurozone trade balance in the main feature in European session. Later in the day, US will release housing starts and building permits, and import prices. But attention will be on U of Michigan consumer sentiment and inflation expectations.

Japan’s GDP contracts -0.2% qoq in Q1, export drag offsets capex gains

Japan’s economy shrank by -0.2% qoq in Q1, marking its first contraction in a year and falling short of the -0.1% qoq consensus. On an annualized basis, GDP contracted by -0.7%, a sharp disappointment compared to expectations for -0.2%.

The weakness was largely driven by external demand, which subtracted -0.8 percentage points from growth as exports declined -0.6% qoq while imports jumped 2.9% qoq.

Domestically, the picture was mixed. Private consumption, comprising more than half of Japan’s output, was flat on the quarter. However, capital expenditure provided some support, rising by a solid 1.4% qoq.

Meanwhile, inflation pressures showed no sign of easing, with the GDP deflator accelerating from 2.9% yoy to 3.3% yoy, above expectations of 3.2% yoy.

RBNZ inflation expectations rise to 2.41%, further easing seen ahead

RBNZ’s latest Survey of Expectations for May revealed a notable uptick in inflation forecasts across all time horizons.

One-year-ahead inflation expectations climbed from 2.15% to 2.41%, while two-year expectations rose from 2.06% to 2.29%. Even long-term projections edged higher, with five- and ten-year-ahead expectations increasing to 2.18% and 2.15% respectively.

Despite the upward revisions in inflation outlook, expectations for monetary policy point clearly toward easing.

With the Official Cash Rate currently at 3.50%, most respondents anticipate a 25 bps cut by the end of Q2. Looking further ahead, the one-year-ahead OCR expectation also declined from 3.23% to 2.91%.

NZ BNZ manufacturing rises to 53.9, recovery gains ground

New Zealand’s BusinessNZ Performance of Manufacturing Index edged up from 53.2 to 53.9 in April. The gain was driven by improvements in employment and new orders, up to 55.0 and 51.4 respectively, with employment reaching its highest level since July 2021. However, production eased slightly to 53.8.

BNZ Senior Economist Doug Steel noted that while the sector isn’t booming, the recovery is clear, with the PMI rebounding sharply from a low of 41.4 last June.

Still, he cautioned, “there remain questions around how sustainable it is given uncertainty stemming from offshore”.

Fed’s Barr: Solid economy faces threats from tariff-driven supply disruptions

Fed Governor Michael Barr highlighted solid growth, low unemployment, and continued progress on disinflation in the US economy. However, he flagged growing concern over rising trade-related uncertainty, which has begun to weigh on consumer and business sentiment.

In a speech overnight, Barr specifically pointed to the vulnerability of small businesses, which are more exposed to “disruptions to supply chains and distribution networks”.

These firms are integral to broader production networks, and failures in this segment could trigger cascading effects across the economy.

Drawing a parallel to the pandemic, Barr noted that “disruptions can have large and lasting effects on prices, as well as output,” leading to lower growth and higher inflation ahead.

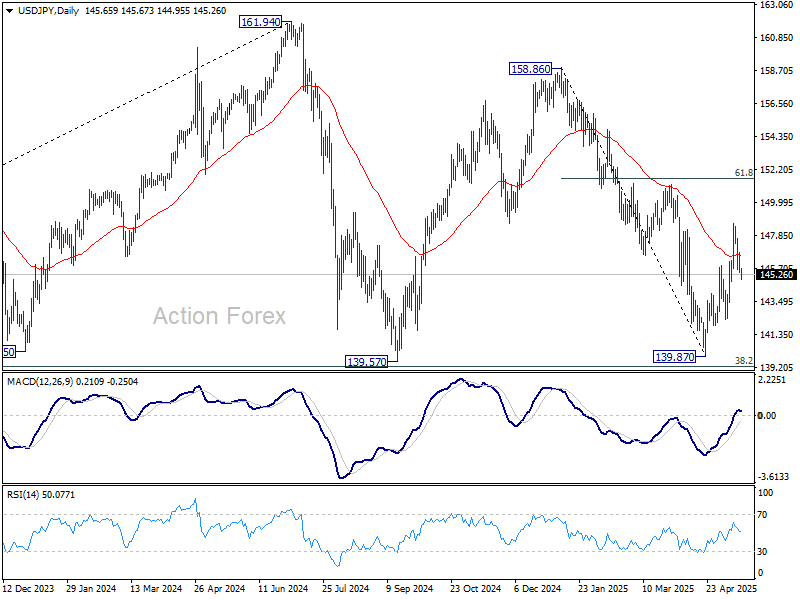

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.13; (P) 145.97; (R1) 146.53; More…

Intraday bias in USD/JPY remains neutral and more consolidations could be seen below 148.64. . Further rally is expected as long as 144.02 resistance turned support holds. As noted before, fall from 158.86 could have completed 139.87 already. Above 148.64 will target 61.8% retracement of 158.86 to 139.87 at 151.60 next. However, firm break of 144.02 will bring retest of 139.87 low instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.