Euro and Pound Rally on UK-EU Pact, Dollar Wobbles – Action Forex

Euro and Sterling surged today after the UK and EU unveiled a sweeping new agreement resetting their defence and trade relationship, the most substantial since Brexit in 2020. The comprehensive deal spans key sectors including security, energy, travel, trade, and fisheries. UK Prime Minister Keir Starmer hosted European Commission President Ursula von der Leyen in London for the high-stakes summit, highlighting the UK’s shift toward pragmatic diplomacy while respecting key post-Brexit red lines.

The UK Labour government was quick to clarify that this reset does not mark a reversal of Brexit. Officials emphasized that the agreement avoids returning to the EU single market, customs union, or freedom of movement. Still, the new deal is being hailed as a boost to corporate confidence and may pave the way for fresh investment flows into the UK, especially following other trade breakthroughs this month with the US and India.

While optimism lifted the Euro and Pound, US assets are under renewed pressure following last week’s credit downgrade by Moody’s. Dollar weakness was notable, with the greenback falling to the bottom of the major currency pack. Treasury yields, however, surged as bond markets reeled from the implications of a swelling fiscal deficit. 10-year yield broke through the key 4.5% level, while 30-year yield topped 5% for the first time in months.

Part of the angst stems from fresh momentum behind President Donald Trump’s multitrillion-dollar domestic policy package. Passed by the House Budget Committee on Sunday, the bill includes major increases in immigration and defense spending, along with an extension of the 2017 tax cuts. It’s now headed for floor debate later this week. Markets are interpreting this as a structural shift toward higher deficits, particularly as tariff revenue is unlikely to fully compensate for lost tax income.

In the currency markets, Euro leads the day’s gains, followed by Sterling and Aussie. Dollar is the weakest performer, trailed by Loonie and Swiss Franc. The Japanese Yen and New Zealand Dollar are trading more mixed.

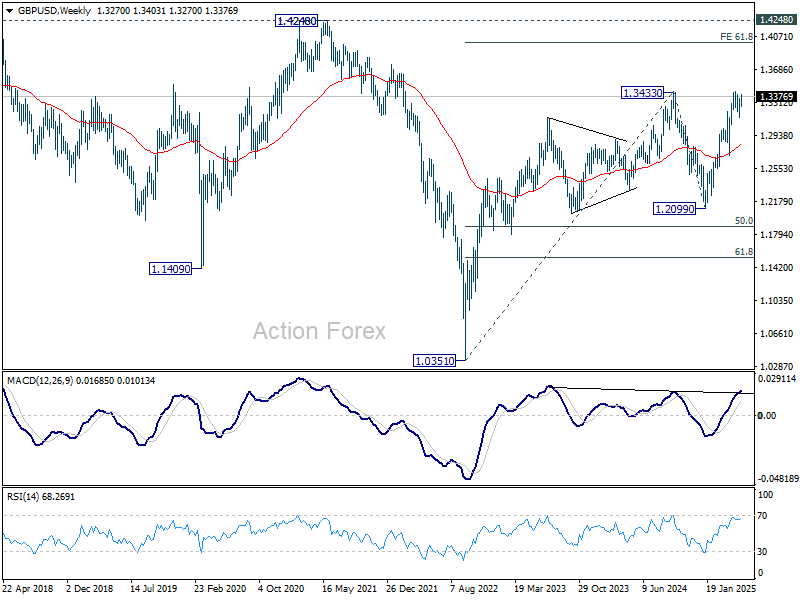

Technically, GBP/USD is now in focus as it approaches key resistance level at 1.3433 (2024 high) again. Decisive break of 1.3433 will confirm resumption of whole up trend from 1.0351 (2022 low). Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004.

In Europe, at the time of writing, FTSE is down 0.44%. DAX is down -0.09%. CAD is down -0.74%. UK 10-year yield is up 0.059 at 4.706. Germany 10-year yield is up 0.057 at 2.645. Earlier in Asia, Nikkei fell -0.68%. Hong Kong HSI fell -0.05%. China Shanghai SSE closed flat. Singapore Strait Times fell -0.56%. Japan 10-year JGB yield rose 0.033 to 1.488.

Fed’s Bostic leans toward one rut in 2025 as inflation expectations turn concerning

Atlanta Fed President Raphael Bostic said on CNBC today that he currently favors just one interest rate cut this year, citing persistent inflation pressures and growing concern over shifting inflation expectations.

“I worry a lot about the inflation side,” Bostic said, noting that recent data shows expectations are beginning to drift upward again “in a troublesome way”, which “will make our job harder.”

Eurozone CPI finalized at 2.2% in April, core at 2.7%

Eurozone headline CPI was finalized at 2.2% yoy in April. CPI core, which excludes energy, food, alcohol, and tobacco, accelerated, to 2.7%, up from 2.4% previously.

Services remained the primary driver of inflation, contributing 1.80 percentage points to the overall figure, followed by food, alcohol and tobacco at 0.57 pp. Energy continued to exert a dampening effect, subtracting -0.35 pp.

At the EU level, annual inflation was slightly higher at 2.4% yoy. Inflation disparities remained wide across the bloc, with France posting the lowest annual rate at 0.9% and Romania the highest at 4.9%.

BoJ’s Uchida notes strain on consumers as food and import costs climb

BoJ Deputy Governor Shinichi Uchida noted in parliamentary remarks that recent inflation has been driven primarily by higher import and food costs, particularly staples like rice.

He acknowledged the burden on households, saying the price increases are “having a negative impact on people’s livelihood and consumption”. The bank remains prepared to continue raising rates if its current forecast holds.

However, Uchida stressed the “extremely high uncertainty” around global trade policies and their economic consequences. Given these risks, he emphasized that the BoJ would assess whether the economy and inflation align with projections before taking further steps.

China’s retail sales growth slows to 5.1% in April, misses expectations

China’s economic data for April revealed a patchy recovery, with retail sales rising by 5.1% yoy, falling short of the 6.0% yoy forecast and slowing from March’s 5.9% yoy. Stripping out automobiles, consumer goods sales rose 5.6% yoy.

National Bureau of Statistics spokesperson Fu Linghui remained upbeat, saying that consumption momentum continues to build and will remain a key driver of economic growth.

On the production side, industrial output grew by 6.1% yoy, exceeding expectations of 5.7% yoy but decelerating from March’s robust 7.7% expansion. Meanwhile, fixed asset investment came in at 4.0% year-to-date, below the expected 4.4%.

NZ BNZ services slips to 48.5, sector remains under pressure

New Zealand’s services sector showed further signs of strain in April, with the BusinessNZ Performance of Services Index dipping from 48.9 to 48.5, well below the long-term average of 53.0.

Key components of the survey highlighted persistent weakness: activity/sales was stagnant at 47.3. Employment slipped back into contraction territory at 48.2. New orders showed only marginal improvement, rising from 50.8 to 50.9.

BNZ Senior Economist Doug Steel noted the PSI paints a more sobering picture than broader recovery narratives might suggest, highlighting that New Zealand’s services sector is underperforming relative to key global peers.

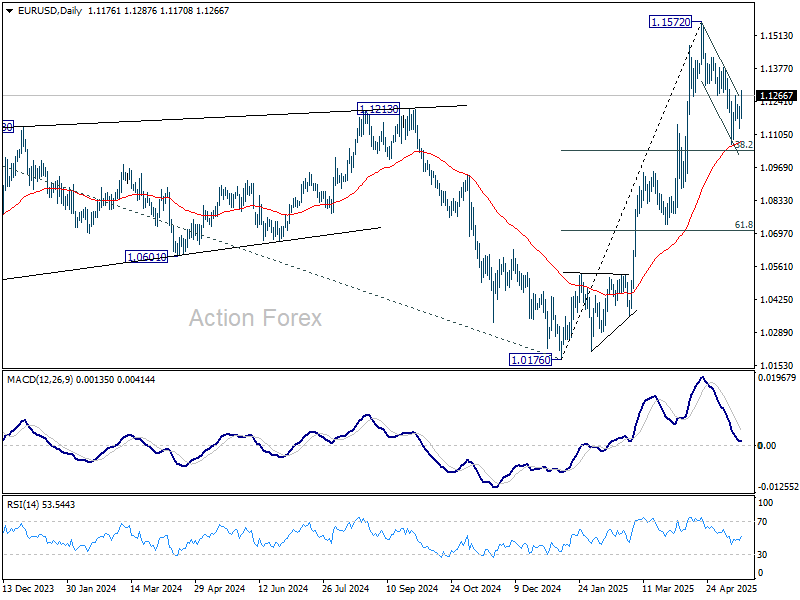

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1123; (P) 1.1171; (R1) 1.1212; More…

Immediate focus is now on 1.1292 resistance in EUR/USD as rebound from 1.1064 resumes. Decisive break there will indicate that correction from 1.1572 has already completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be turned back to the upside for retesting 1.1572 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0818) holds.