Risk Mood Softens as Moody’s US Downgrade and Mixed China Data Dent Confidence – Action Forex

Global markets kicked off the week with a mild risk-off tone, driven by renewed concerns over US creditworthiness and mixed economic data out of China. Moody’s downgrade of the U.S. sovereign rating from Aaa to Aa1 late last Friday has cast a shadow over investor sentiment. Meanwhile, China’s latest data highlighted a fragile recovery with industrial output holding up but retail sales and investment disappointing. Still, losses in Asian equities have been relatively contained so far, suggesting caution more than panic.

The more notable market movement is in US futures, where the DOW is down over 200 points in early trade. However, since US cash markets are yet to reopen, the true extent of investor reaction remains to be seen. Currency markets are relatively quiet, with Dollar trading on the soft side, but there’s no sign of a broad-based selloff. Nearly all major currency pairs and crosses are hovering within Friday’s ranges.

Trade policy developments will continue dominate this week’s narrative. In a Sunday interview, US Treasury Secretary Scott Bessent reiterated the administration’s readiness to reinstate reciprocal tariffs at the April 2 rate on countries that fail to negotiate “in good faith.” However, he offered little clarity on what qualifies as “good faith” or when decisions might be announced.

Bessent noted that the US is currently focused on its 18 most important trading relationships, and letters will be sent out to those nations deemed to be stalling or resisting negotiations. The threat of reactivating the more extreme tariff brackets imposed in April looms large and could provoke renewed volatility.

On the economic calendar, RBA’s expected rate cut will headline central bank action. Meanwhile, inflation data from Canada, the UK, and Japan will offer fresh insight into price dynamics amid global tariff pressures. Retail sales from the UK, Canada, and New Zealand will help gauge consumer resilience. ECB’s meeting accounts may shed light on the internal debate ahead of its anticipated June rate cut.

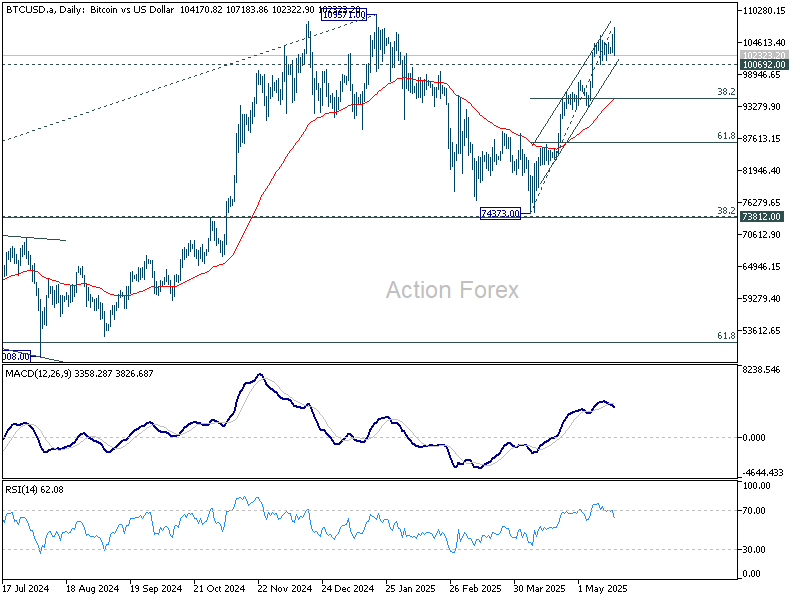

Technically, Bitcoin reversed quickly after initial surge earlier today. Upside momentum is also unconvincing as seen in D MACD. Break of 100692 support should confirm rejection by 109571 higher. Deeper pullback should at least be seen to 55 D EMA (now at 94361), with risk of near term bearish reversal.

In Asia, Nikkei fell -0.73%. Hong Kong HSI is down -0.02%. China Shanghai SSE is up 0.02%. Singapore Strait Times is down -0.25%. Japan 10-year JGB yield is up 0.03 at 1.485.

BoJ’s Uchida notes strain on consumers as food and import costs climb

BoJ Deputy Governor Shinichi Uchida noted in parliamentary remarks that recent inflation has been driven primarily by higher import and food costs, particularly staples like rice.

He acknowledged the burden on households, saying the price increases are “having a negative impact on people’s livelihood and consumption”. The bank remains prepared to continue raising rates if its current forecast holds.

However, Uchida stressed the “extremely high uncertainty” around global trade policies and their economic consequences. Given these risks, he emphasized that the BoJ would assess whether the economy and inflation align with projections before taking further steps.

China’s retail sales growth slows to 5.1% in April, misses expectations

China’s economic data for April revealed a patchy recovery, with retail sales rising by 5.1% yoy, falling short of the 6.0% yoy forecast and slowing from March’s 5.9% yoy. Stripping out automobiles, consumer goods sales rose 5.6% yoy.

National Bureau of Statistics spokesperson Fu Linghui remained upbeat, saying that consumption momentum continues to build and will remain a key driver of economic growth.

On the production side, industrial output grew by 6.1% yoy, exceeding expectations of 5.7% yoy but decelerating from March’s robust 7.7% expansion. Meanwhile, fixed asset investment came in at 4.0% year-to-date, below the expected 4.4%.

NZ BNZ services slips to 48.5, sector remains under pressure

New Zealand’s services sector showed further signs of strain in April, with the BusinessNZ Performance of Services Index dipping from 48.9 to 48.5, well below the long-term average of 53.0.

Key components of the survey highlighted persistent weakness: activity/sales was stagnant at 47.3. Employment slipped back into contraction territory at 48.2. New orders showed only marginal improvement, rising from 50.8 to 50.9.

BNZ Senior Economist Doug Steel noted the PSI paints a more sobering picture than broader recovery narratives might suggest, highlighting that New Zealand’s services sector is underperforming relative to key global peers.

ECB’s Lagarde attributes Euro strength to waning confidence in US policy amid uncertainty

ECB President Christine Lagarde has described the Euro’s recent appreciation against Dollar as “counter-intuitive,” but ultimately a reflection of growing global unease over US political and economic direction.

In an interview with La Tribune Dimanche, Lagarde said that parts of the financial markets appear to be “losing confidence” in the US, due to economic and financial chaos during the first 100 days of President Donald Trump’s term.

By contrast, Lagarde highlighted Europe’s comparative stability, both economic and institutional, as a key driver behind the Euro’s unexpected strength.

“Uncertainty is a constant [in the US],” she noted, while Europe is being recognized as “a stable economic and political region with a solid currency and an independent central bank.”

That divergence in perceived reliability, she argues, has led markets to favor the Euro even in a climate where risk aversion would normally boost Dollar.

RBA rate cut, inflation data from Canada, UK and Japan to highlight the week

RBA is widely expected to deliver a 25 bps rate cut, bringing the cash rate down to 3.85%. While all of Australia’s big four banks agree on the need for further easing, there’s some divergence on the pace. NAB stands out with a bolder forecast, projecting a larger 50bps reduction.

Looking ahead, ANZ anticipates two more cuts in July and August to bring the cash rate to 3.35% by then. Commonwealth Bank shares a similar view but sees the final cut coming in November. NAB expects a more dovish sequence, projecting three further cuts by year-end, followed by one more in early 2026. Westpac also forecasts two cuts in H2 2025.

Yet, with global tariff negotiations still unresolved, particularly regarding China, Australia’s economic outlook remains highly fluid, leaving room for policy recalibration in the months ahead.

On the data front, inflation will dominate. Canada, the UK, and Japan are all set to release April CPI figures.

In Canada, headline inflation could be significantly distorted by the recent removal of the consumer carbon tax on energy products. As a result, attention will shift to the ex-energy components, which could offer clearer guidance for the BoC. Economists generally expect another rate cut in June, provided the CPI report shows subdued underlying pressures, especially as tariff effects begin to bite.

In the UK, inflation is projected to rebound above 3%, largely due to previously flagged increases in energy prices and regulated items like water bills. BoE has already accounted for this temporary surge, so a surprise in either direction is unlikely to alter its current pace of easing, generally one 25bps cut per quarter.

Japan’s CPI will also attract attention after Q1 GDP revealed a deeper-than-expected contraction, causing markets to dial back BoJ rate hike bets. Even if core inflation picks up again in April, BoJ is likely to remain on hold for now, especially given the dual headwinds of weak growth and global trade uncertainty. However, an upside surprise could test BoJ’s tolerance.

Beyond inflation, retail sales from the UK, Canada, and New Zealand will provide insight into consumer resilience in face of tariff threats. Germany’s Ifo Business Climate and a batch of Chinese data, including retail sales, industrial production, and fixed asset investment, will also be in focus. Additionally, ECB will publish the minutes of its latest policy meeting, offering more clues on the anticipated June rate cut.

Here are some highlights for the week:

- Monday: New Zealand BNZ services, PPI; China industrial production, retail sales, fixed asset investment; Japan tertiary industry index; Eurozone CPI final.

- Tuesday: China rate decision; RBA rate decision; Germany PPI; Eurozone current account; Canada CPI.

- Wednesday: New Zealand trade balance; Japan trade balance; UK CPI; Canada new housing price index.

- Thursday: Australia PMIs; Japan PMIs, machine orders; Eurozone PMIs, ECB accounts; Germany Ifo business climate; UK PMIs; Canada IPPI and RMPI; US jobless claims, PMIs, existing home sales.

- Friday: New Zealand retail sales; Japan CPI; UK retail sales; Germany GDP final; Canada retail sales; US new home sales.

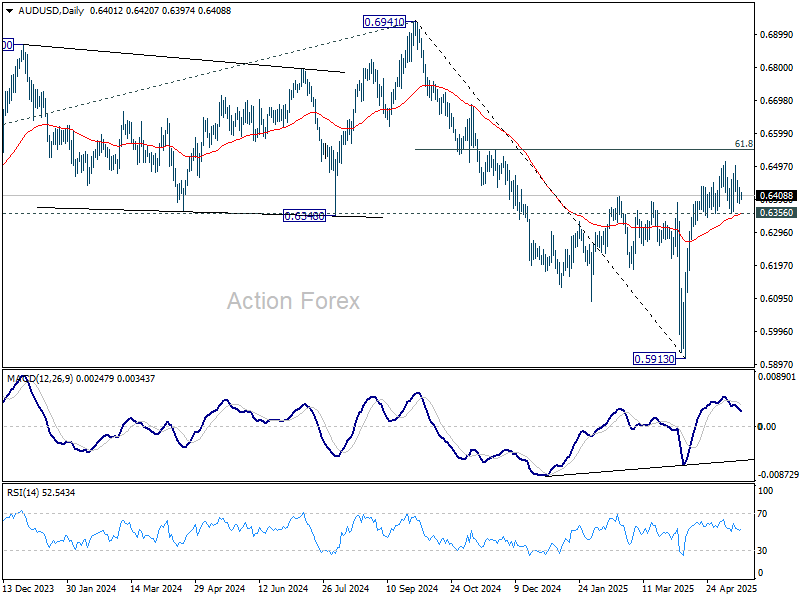

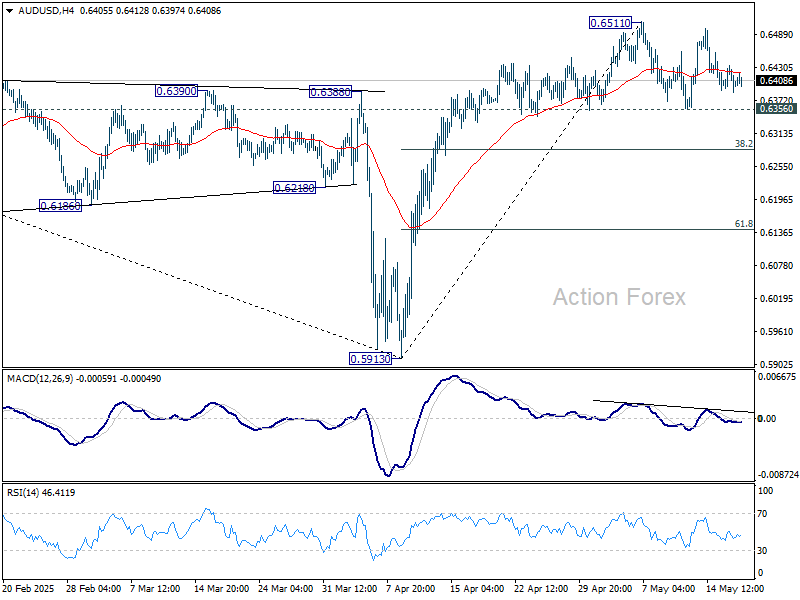

AUD/USD Daily Report

Daily Pivots: (S1) 0.6382; (P) 0.6409; (R1) 0.6430; More...

Intraday bias in AUD/USD remains neutral as range trading continues. Further rise is in favor as long as 0.6356 support holds. One the upside, break of 0.6511 will resume the rise from 0.5913 and target 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, firm break of 0.6356 will bring deeper pullback to 38.2% retracement of 0.5913 to 0.6511 at 0.6283 first.

In the bigger picture, as long as 55 W EMA (now at 0.6438) holds, down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.