US Assets Remain Under Pressure; Sterling Gains Muted Despite Hot CPI – Action Forex

Dollar’s selloff moderated slightly during European session, but pressure on US assets remains firmly in place. DOW futures are down more than -300 points, while the 10-year Treasury yield has surged back above the 4.5% mark. Market sentiment continues to reflect unease over the US fiscal outlook and uncertainty surrounding the Trump administration’s trade stance. With the G7 finance ministers’ meeting underway, any hint that Washington may be aiming for a weaker currency will be closely scrutinized.

In the UK, despite a hotter-than-expected CPI report, Sterling failed to extend gains beyond Dollar and weakened against most other majors. A particularly striking detail in the report was the 5.4% surge in services inflation, which surpassed BoE’s own forecast of 5.0%. On a monthly basis, services prices jumped 2.2% the largest monthly rise in 34 years.

This supports recent remarks from BoE Chief Economist Huw Pill, who argued that the pace of policy easing may be too fast given the structural persistence in wage and price-setting behavior. The CPI report has clearly dampened market expectations for a summer rate cut, with odds of an August move now down to 40%, compared to 60% before the data release.

In the broader currency markets, Dollar remains the weakest performer so far today, trailed by Sterling and the Loonie. At the other end, Yen leads the pack amid safe-haven demand, followed by Swiss Franc and Euro. Aussie and Kiwi are trading in the middle.

In Europe, at the time of writing, FTSE is up 0.06%. DAX is down -0.28%. CAC is down -0.58%. UK 10-year yield is up 0.066 at 4.771. Germany 10-year yield is up 0.046 at 2.654. Earlier in Asia, Nikkei fell -0.61%. Hong Kong HSI rose 0.62%. China Shanghai SSE rose 0.21%. Singapore Strait Times closed flat. Japan 10-year JGB yield fell -0.002 to 1.521.

UK CPI surges to 3.5% in April, core jumps to 3.8%

UK inflation came in hotter than expected in April, with headline CPI rising 1.2% mom versus expectation f 1.1% mom. Annual CPI accelerated from 2.6% yoy to 3.5% yoy, above the 3% mark for the first time since March 2024.

Core CPI, which strips out energy, food, alcohol and tobacco, climbed sharply from 3.4% yoy to 3.8% yoy, its highest level since April 2024.

Breakdowns show a sharp jump in both goods and services inflation. Goods inflation accelerated from 0.6% yoy to 1.7% yoy, while services inflation climbed from 4.7% yoy to 5.4% yoy , highlighting the strength of domestic price pressures.

Japan’s US-bound exports fall -1.8% yoy as tariffs and strong Yen Bite

.Japan’s export growth slowed to just 2.0% yoy in April, marking the weakest pace since October 2024.

Notably, shipments to the US fell -1.8% yoy — the first decline in four months — as demand for automobiles, steel, and ships weakened. Exports of automobiles alone dropped -4.8% yoy by value, impacted by a stronger Yen and reduced demand for high-end models.

The decline coincides with the imposition of 25% US tariffs on Japanese auto, steel, and aluminum exports, alongside the 10% blanket levy applied to most trade partners under the current US trade regime.

Trade with Asia remained more resilient, with exports rising 6.0% yoy. However, shipments to China dipped -0.6% yoy.

On the import side, Japan saw a -2.2% yoy contraction, resulting in a trade deficit of JPY -115.8B.

Seasonally adjusted figures show a -2.7% mom drop in exports and a -1.4% mom drop in imports, with the adjusted trade deficit widening to JPY -409B.

Australia’s leading index falls to 0.2%, growth pulse fades

Australia’s Westpac Leading Index slowed from 0.5% to 0.2% in April, signaling a loss in growth momentum.

According to Westpac, the above-trend growth seen earlier this year has “all but disappeared,” primarily due to rising global trade uncertainty and weaker commodity prices.

While these external pressures dominate, domestic factors such as a slowing labor market and only modest support from interest rate cuts are also contributing to the loss of momentum.

The overall picture suggests a stalling in the already tepid recovery, with GDP growth expected to reach just 1.9% by the end of 2025, well below historical averages.

Following RBA’s recent 25bps rate cut to 3.85%, Westpac expects a cautious pause at the next policy meeting on July 7–8. The central bank is likely to await further clarity from the Q2 inflation data due at the end of July before considering additional easing.

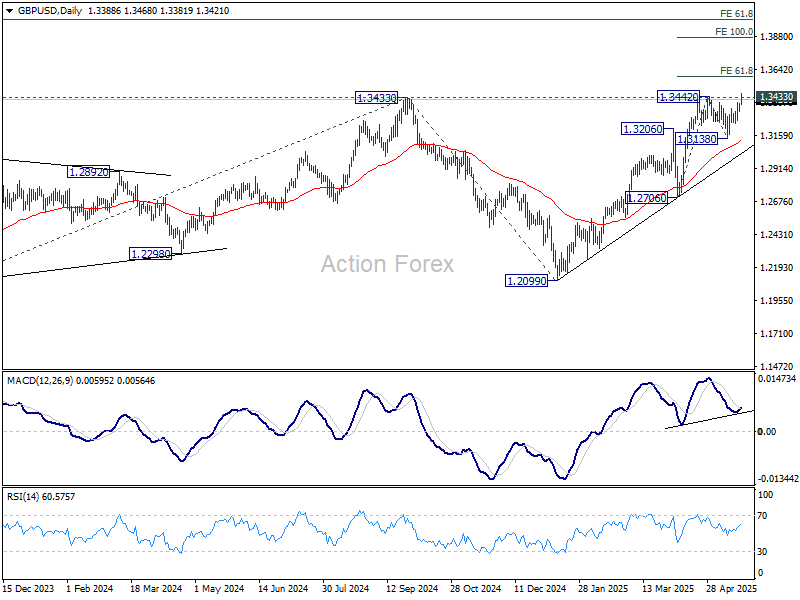

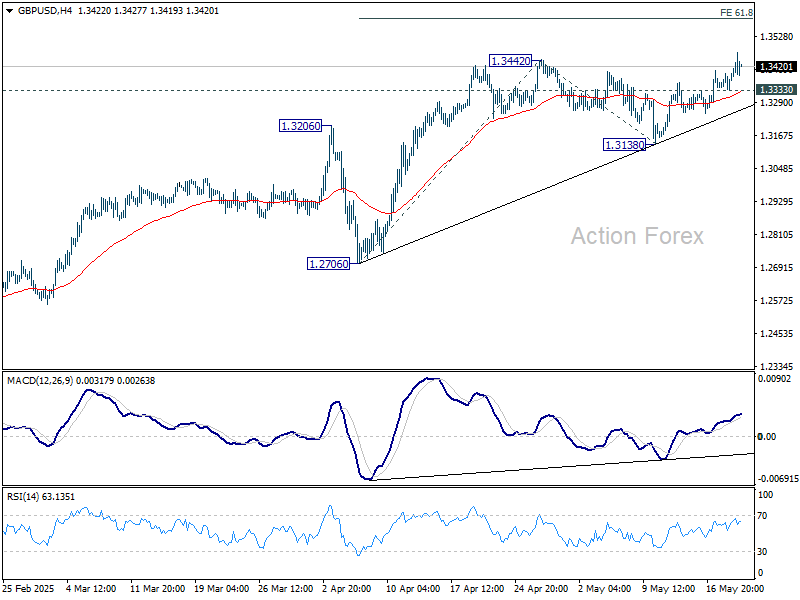

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3354; (P) 1.3375; (R1) 1.3414; More…

Intraday bias in GBP/USD stays on the upside for the moment, with focus on 1.3433/42 key resistance zone. Decisive break there will confirm larger up trend resumption. Next near term target will be 61.8% projection of 1.2706 to 1.3442 from 1.3138 at 1.3593, and then 100% projection at 1.1.3874. On the downside, below 1.3333 minor support will delay the bullish case and turn intraday bias neutral first.

In the bigger picture, up trend from 1.3051 (2022 low) is still in progress. Decisive break of 1.3433 (2024 high) will confirm resumption. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Nevertheless, sustained trading below 55 D EMA (now at 1.3124) will delay the bullish case and bring more consolidations first.