Dollar Recovers as Markets Stabilize, Euro Pressured by PMI and Dovish ECB Accounts – Action Forex

Dollar staged a broad recovery today as financial markets found some footing following a volatile stretch dominated by US deficit concerns. US futures are trading flat, while 10-year Treasury yield has pared back modestly from recent highs, signaling a pause in the bond selloff. The calmer tone helped the greenback regain some traction.

Support for Dollar came even after a narrow passage of a sweeping tax and spending bill in the US House of Representatives. The legislation, central to President Donald Trump’s policy agenda, introduces a range of tax breaks, most notably on tips and car loans, while substantially boosting military and border enforcement budgets. The Congressional Budget Office estimates the bill would add approximately USD 3.8 Trillion to debt over the next decade.

In Europe, Euro came under some pressure following disappointing PMI data. The services sector unexpectedly slipped back into contraction territory in May, highlighting the fragility of the region’s recovery. The PMI Composite also dipped below 50, reinforcing the view that growth momentum is stalling again after a weak start to the year.

Adding to Euro’s woes, ECB’s latest meeting accounts revealed internal discussions over a more aggressive 50 basis point rate cut in April, although the final decision was a unanimous 25 basis point reduction. While the accounts reflect growing confidence in disinflation trends, they also underscore a heightened sense of caution about weakening growth and the evolving global trade environment.

Overall in the currency markets, Yen stands out as the strongest performer today so far, followed by Dollar, and then Sterling. Kiwi leads the losers, followed by Euro and Aussie. Loonie and Swiss Franc are positioning in the middle. Overall, today’s market tone isn’t clearly risk-on.

Technically, Bitcoin finally surged to new record high above 110000 this week. Upside momentum remains strong as seen in D MACD. Current up trend could now be targeting 100% projection of 49008 to 109571 from 73473 at 134936 next. For now, outlook will remain bullish as long as 100692 support holds, in case of retreat.

In Europe, at the time of writing, FTSE is down -0.77%. DAX is down -0.08%. CAC is down -1.05%. UK 10-year yield is up 0.008 at 4.769. Germany 10-year yield is down -0.002 at 2.652. Earlier in Asia, Nikkei fell -0.84%. Hong Kong HSI fell -1.19%. China SSE fell -0.22%. Singapore Strait Times fell -0.06%. Japan 10-year JGB yield rose 0.041 to 1.562.

US initial jobless claims fall to 227k vs exp 230k

US initial jobless claims fell -2k to 227k in the week ending May 17, below expectation of 230k. Four-week moving average of initial claims rose 1k to 232k.

Continuing claims rose 36k to 1903k in the week ending May 10. Four-week moving average of continuing claims rose 18k to 1888k, highest since November 2021.

UK PMI composite ticks up to 49.4, price pressures ease from April spike

UK PMI Services rose modestly from 49.0 to 50.2, while Manufacturing PMI edged lower from 45.4 to 45.1. As a result, the Composite PMI ticked up from 48.5 to 49.4, still below the 50-mark that separates expansion from contraction.

According to S&P Global’s Chris Williamson, business confidence has improved since April, helped in part by easing trade tensions. However, output across the private sector shrank for a second consecutive month, suggesting that the UK economy may be slipping into contraction for Q2.

On a more encouraging note, inflationary pressures appear to have cooled significantly from April’s spike. This moderation in price growth, combined with lackluster output and emerging job losses, strengthens the case for further monetary easing by BoE in the coming months.

ECB accounts: Some members see April rate cut as frontloading a June move

ECB’s April 16–17 meeting accounts revealed unanimous support for the 25 basis point rate cut, the inflation shock was “nearly over”. The cut was not only as a response to improving inflation outlook but also as insurance against mounting downside risks to growth, driven by escalating global trade tensions.

Several members specifically cited recent developments around tariffs as rationale for acting sooner rather than later. In their view, a cut at the April meeting could be seen as “frontloading a possible cut at the June meeting”, helping to anchor sentiment amid elevated market volatility.

Some members noted that the tariff-driven uncertainty did not appear to be translating into inflationary pressure, partly due to Euro’s appreciation role as a “safe-haven currency”. Instead, tariff-related headwinds were increasingly viewed as disinflationary, especially as growth prospects weakened and financial conditions tightened.

A minority on the Council even argued for a more aggressive 50 bps cut, citing a deterioration in the balance of risks since March. These members emphasized that “even in the event of a relatively mild trade conflict, uncertainty was already discouraging consumption and investment.

Eurozone PMI composite falls to 49.5, services falter, manufacturing holds tentatively

Eurozone’s private sector returned to contraction in May, with PMI Composite falling from 50.4 to 49.5, a six-month low. The drag came from the services sector, where the PMI dropped from 50.1 to 48.9, its weakest reading in 16 months. While the manufacturing index rose modestly from 49.0 to 49.4, marking a 33-month high, it remained in contractionary territory.

According to HCOB Chief Economist Cyrus de la Rubia, the region’s economy “cannot seem to find its footing,” as growth signals remain elusive and sentiment subdued.

The modest improvement in manufacturing may reflect front-loaded activity as firms seek to get ahead of US tariffs, rather than underlying demand strength. However, the downturn in services, typically more domestically oriented and less exposed to global trade, raises concern about internal demand softness.

For the ECB, the numbers are “likely to leave it with mixed feelings”. While service sector inflation appears to be moderating, input costs — likely driven by wages — are ticking higher again. Manufacturing purchase prices, by contrast, continue to fall.

German Ifo rises to 87.5, economy stabilizing with uncertainty eased

Germany’s Ifo Business Climate Index rose to 87.5 in May, up from 86.9 in April, offering cautious optimism that the economy may be stabilizing.

The improvement was driven by a notable rise in the Expectations Index, which climbed from 87.4 to 89.9, a sign that firms are growing more confident about future conditions. However, the Current Situation Index dipped slightly from 86.4 to 86.1.

The Ifo Institute noted that “sentiment among German companies has improved” and that the recent surge in uncertainty has begun to ease.

BoJ’s Noguchi: Must tread carefully with step-by-step policy normalization

BoJ board member Asahi Noguchi emphasized the importance of a “measured, step-by-step” pace in raising interest rates, stressing the need to carefully assess the economic impact of each hike before proceeding further.

Noguchi also addressed the upcoming interim review of BoJ’s bond tapering strategy, indicating that he sees no need for any major adjustments to the current plan, which runs through March 2026.

He noted that the central bank should approach its long-term reduction in the balance sheet with flexibility, taking the time needed to ensure stability while maintaining the capacity to respond to “sudden market swings”.

Any emergency increase in bond purchases, he noted, would be strictly conditional and “only be implemented during times of severe market disruption.”

Japan’s PMI composite falls to 49.8, private sector contracts again

Japan’s private sector activity fell back into contraction in May, with PMI Composite declining from 51.2 to 49.8. Manufacturing output edged higher from 48.7 to 49.0, but remained below the neutral 50 mark. The services sector, however, lost more momentum, with its PMI falling from 52.4 to 50.8.

The decline in composite output reflects weakening domestic and external demand, as new business volumes fell for the first time in nearly a year.

S&P Global’s Annabel Fiddes noted that elevated uncertainty around trade policy and foreign demand weighed heavily on business confidence, which sank to its second-lowest level since the pandemic’s onset.

RBA’s Hauser: Post-tariff China outlook positive but incomplete

In a speech focused on his recent visit to China following the sweeping tariff shifts of “Liberation Day”, RBA Deputy Governor Andrew Hauser noted there was a sense of “strong hand” in managing the economic fallout from US-imposed tariffs. Additionally, Australian firms operating in China perceived “opportunities amidst the risks”, as trade patterns began to shift.

However, Hauser was quick to stress that this view was inherently limited, anchored to a moment in time and shaped by a single national perspective.

Hauser laid out four key caveats. First, global tariff settings remain fluid, and data on their real-world economic effects is just beginning to emerge. Second, the assessments he heard may prove overly optimistic, domestic stimulus in China may underperform, and public tolerance for economic pain may be lower than expected.

Third, indirect “general equilibrium” effects could emerge, including the possibility of intensified competition from Chinese firms offloading excess supply originally intended for US markets. While sectoral overlap with Australia is limited, it is a concern shared across the Asia-Pacific region.

Finally, Hauser acknowledged the broader strategic uncertainties at play—factors beyond economics that could shape Australia’s position.

Australia’s PMI Composite slips to 50.6; firms cite election drag on demand

Australia’s private sector showed signs of slowing in May, with PMI Composite falling from 51.0 to a 3-month low of 50.6. Manufacturing index held steady at 51.7. But services weakened from 51.0 to 50.5, its lowest level in six months.

According to S&P Global’s Andrew Harker, the sluggishness may be tied in part to election-related uncertainty, which “contributed to slower growth of new orders”. Still, firms remained cautiously optimistic, continuing to hire at a “solid pace”. With the political noise expected to ease, attention will turn to whether demand picks up in the months ahead.

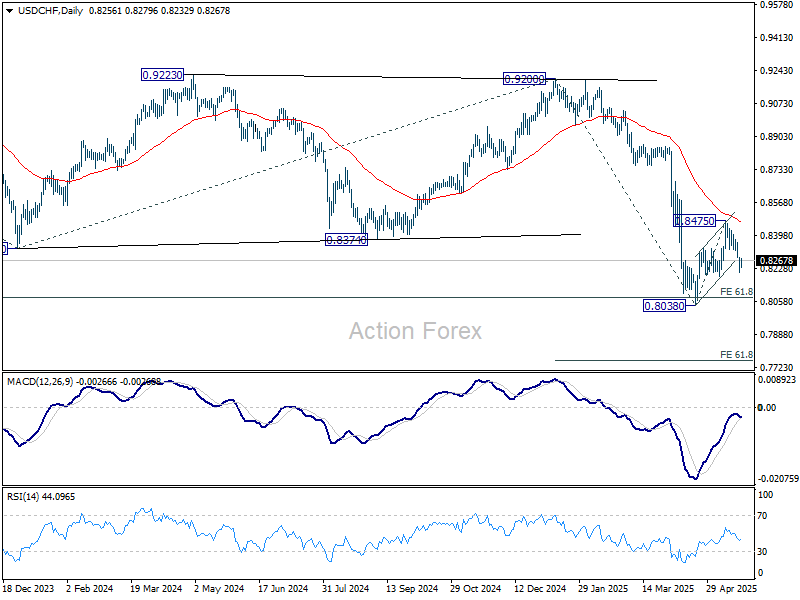

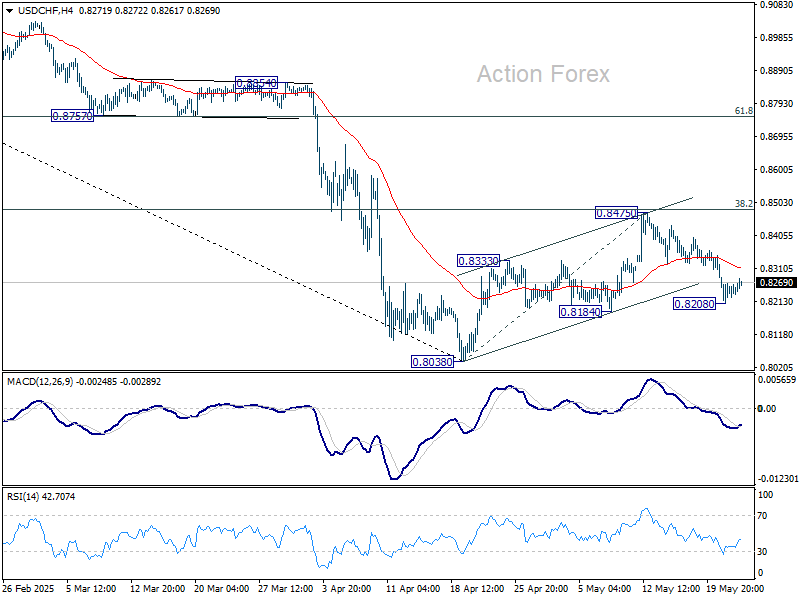

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8211; (P) 0.8251; (R1) 0.8251; More….

Intraday bias in USD/CHF is turned neutral first with current recovery. But risk will remain on the downside as long as 0.8475 resistance holds. Corrective rebound from 0.8038 should have completed already. Below 0.8208 will bring retest of 0.8038 first. Firm break there will resume larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8765) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.